Viasat Inc (VSAT), Mid/Small Cap AI Study of the Week

June 13, 2024

Weekly AI Pick from the S&P 400 or S&P 600

Company Overview

Viasat, Inc., founded in 1986, is a global communications technology and services provider catering to sectors such as aviation, maritime, enterprise, consumer, military, and government. The company operates through three segments: satellite services, commercial networks, and government systems. Notable recent acquisitions include Inmarsat, enhancing Viasat’s satellite services, and Euro Broadband Infrastructure and RigNet, which boost its capabilities in satellite broadband internet services across Europe, the Middle East, and Africa. Viasat also sold its Link-16 Tactical Data Links business to L3Harris Technologies for approximately $1.96 billion.

Viasat's business is divided into three main sectors: Energy Services, IoT and Other Narrowband Services, and Community Internet Services. Energy Services, strengthened by the acquisition of RigNet, offer secure connectivity and machine learning analytics. IoT and Narrowband Services provide real-time M2M tracking and industrial IoT solutions, while Community Internet Services offer affordable satellite-based internet in underserved regions like Mexico and Brazil. The company anticipates significant growth in its satellite services, driven by global mobility services and increasing numbers of connected aircraft and maritime vessels.

The Commercial Networks segment develops advanced satellite and wireless products, supporting both broadband and narrowband services, while the Government Systems segment focuses on communication and cybersecurity solutions for military and government clients. Viasat offers a range of satellite communication products, including SATCOM broadband modems, terminals, and systems for various applications. The company emphasizes secure networking and cybersecurity, with high-speed encryption solutions for military and government users.

Viasat's growth is expected to stem from the rising demand for high-speed, secure connectivity services to support global military and government operations. The company’s strengths include a comprehensive satellite fleet, a wide array of service offerings, ongoing innovation in satellite and space technologies, a vertically integrated platform, and a diversified business model. Their diversified portfolio ensures resilience against market fluctuations and economic disruptions, with significant offerings for military and government sectors.

Viasat is expanding its international presence, leveraging the Inmarsat acquisition to offer near-global broadband and narrowband services, including strong oceanic and future polar coverage. The company collaborates with content providers and U.S. government agencies to enhance user experiences with affordable broadband, especially in underserved areas, thereby generating socio-economic benefits. Viasat’s revenue is significantly driven by U.S. government contracts, awarded through competitive bidding and involving various contract types. The company emphasizes sustainable and responsible access to space through strategic alliances and acquisitions.

By the Numbers

- Inmarsat Holdings acquisition cost: $550.7 million in cash and 46.36 million shares of common stock.

- Financing for acquisition: $616.7 million in secured term loans and $733.4 million in unsecured bridge loans.

- Replacement of bridge loans: 7.500% Senior Notes due 2031.

- Sale of Link-16 Tactical Data Links business: $1.96 billion in cash.

- In-flight connectivity (IFC) systems: Installed on approximately 3,540 commercial aircraft, with plans for an additional 1,430 aircraft.

- Total revenue increase for the quarter ending December 31, 2023: $477.1 million compared to the same period in 2022.

- Service revenue increase: $423.3 million.

- Product revenue increase: $53.8 million.

- Satellite services segment revenue increase: $279.0 million.

- Government systems segment revenue increase: $142.5 million.

- No material impairments noted for periods ended December 31, 2023, and 2022.

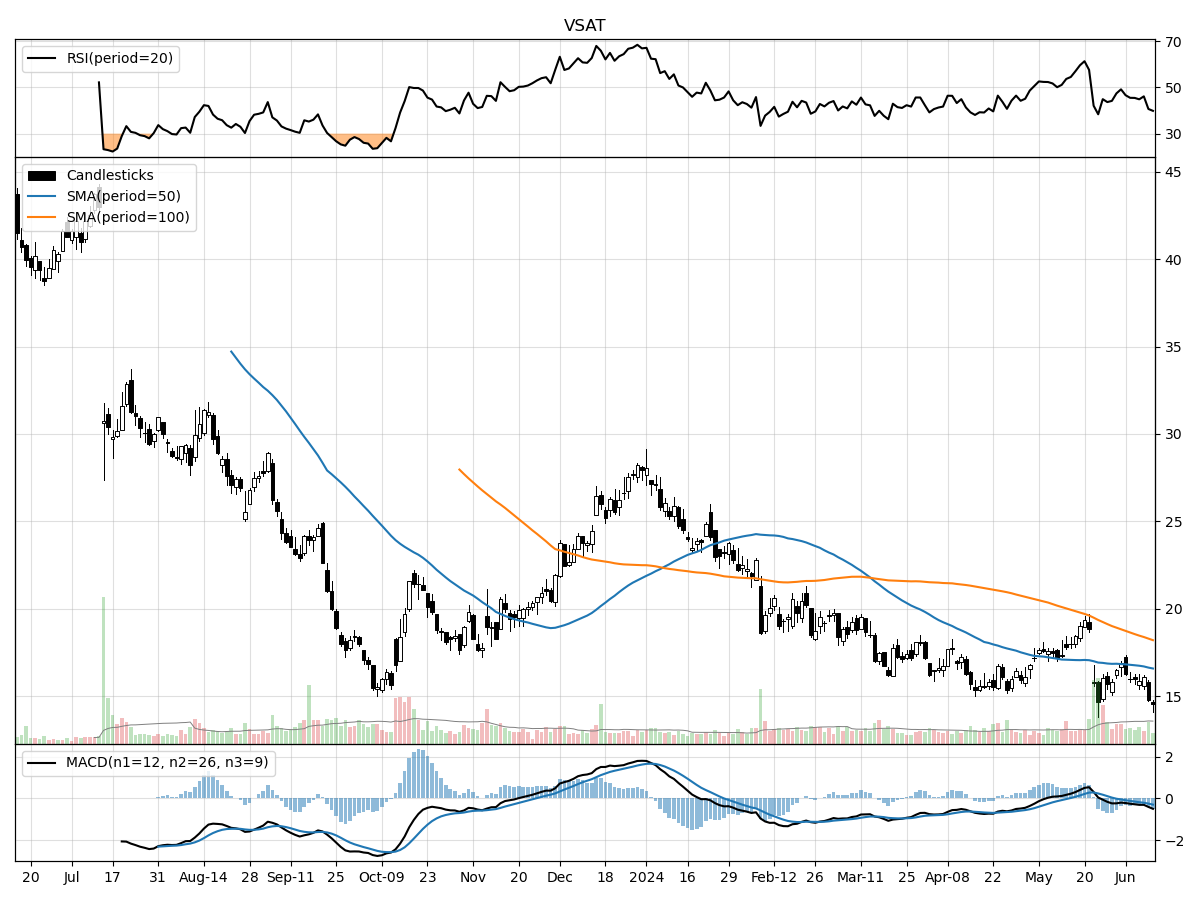

Stock Performance and Technical Analysis

The technical analysis of a stock involves the interpretation of statistical trends gathered from trading activity, such as price movement and volume. When considering an investment in the company with the current stock price of $14.57, which is precisely at its 52-week low and significantly below its 52-week high by 67%, it suggests that the stock has been undergoing a substantial downward trend. This could either indicate a potential undervaluation, assuming the company's fundamentals remain strong, or it might reflect a negative outlook on the company's future prospects or general market sentiment.

The recent trading volume is higher than the longer-term average, with approximately 1,796,159 shares traded daily compared to the longer-term average of 1,278,536 shares. This suggests increased investor interest or activity, which often accompanies significant price moves. However, given the price has fallen 18.36% in the last month and 12.99% in the last three months, this increased volume appears to coincide with selling pressure rather than buying interest.

Money Flow indicators, such as the Money Flow Index (MFI), help in determining the strength of money flowing in and out of a stock. Currently, they suggest moderate selling pressure and distribution, meaning that larger investors may be offloading their shares, possibly indicating a bearish outlook. Moreover, the Moving Average Convergence Divergence (MACD) is a trend-following momentum indicator that shows the relationship between two moving averages of a stock's price. A bearish MACD at -0.29 confirms that the short-term momentum is in a downward phase relative to the long-term momentum, reinforcing the current negative trend.

Based on these technical indicators, a conservative approach would be to watch the stock for stabilization or signs of a trend reversal before considering an investment. An aggressive investor might see the current low price as a buying opportunity, expecting a potential rebound, but should proceed with caution given the current bearish signals. It's essential to complement technical analysis with fundamental analysis and recent news that could affect the stock's future performance.

The ‘Bull’ Perspective

Summary:

- Robust Revenue Growth: Viasat’s recent financial performance showcases a significant increase in total revenues, with a $477.1 million rise compared to the same period in 2022, largely due to the strategic Inmarsat acquisition.

- Expanding Market Presence: Post-acquisition, Viasat now has approximately 3,540 commercial aircraft with in-flight connectivity systems, with plans to expand this to an additional 1,430 aircraft.

- Diverse Revenue Streams: The company’s diversified business model across satellite services, commercial networks, and government systems provides multiple avenues for revenue generation.

- Strategic Acquisitions and Divestitures: The acquisition of Inmarsat and the sale of the Link-16 Tactical Data Links business to L3Harris Technologies for about $1.96 billion in cash positions Viasat for strategic growth and capital allocation.

- Mitigating Risks: Viasat is navigating through industry-specific risks and broader economic headwinds with strategic measures, such as careful cost capitalization, insurance coverage, and a focus on technological innovation.

Elaboration:

- Robust Revenue Growth:

Viasat has demonstrated a formidable increase in its revenue streams, with a notable $477.1 million year-over-year growth in total revenues for the quarter ending December 31, 2023. This surge is primarily attributed to the Inmarsat acquisition, which contributed a $423.3 million boost in service revenues and a $53.8 million increase in product revenues. The satellite services segment alone saw a $279.0 million increment, underscoring the success of the acquisition in bolstering the company's financial stature. Such impressive figures indicate that Viasat is effectively leveraging its acquisitions to drive revenue and scale operations. - Expanding Market Presence:

Viasat's in-flight connectivity (IFC) systems are now installed on approximately 3,540 commercial aircraft, with commitments to equip an additional 1,430 aircraft. This expansion is significant, given the industry's recovery from COVID-19 impacts and the growing demand for in-flight broadband services. Despite satellite anomalies reported this year, Viasat's proactive approach and contractual agreements suggest a robust pipeline for future growth and a solidifying presence in the aviation sector. - Diverse Revenue Streams:

The diversity of Viasat's revenue streams, spanning satellite services, commercial networks, and government systems, provides a hedge against market volatility. The company's government systems segment, in particular, reported a $142.5 million increase in service revenue, reflecting the strength and stability of its defense-related income. Such diversification allows Viasat to tap into various high-priority technology markets and secure large contracts, mitigating the risks associated with reliance on a single revenue source. - Strategic Acquisitions and Divestitures:

Viasat's strategic decision to acquire Inmarsat and divest its Link-16 Tactical Data Links business to L3Harris Technologies for a substantial $1.96 billion cash infusion showcases the company's commitment to optimizing its portfolio and focusing on core growth areas. These moves not only provide immediate financial benefits but also realign the company's strategic direction towards emerging opportunities in global communications. - Mitigating Risks:

Despite facing risks such as satellite anomalies and competitive pressures, Viasat employs prudent risk mitigation strategies, including careful estimation and accounting practices. The company capitalizes costs related to satellite construction and launch, with periodic reviews to adjust depreciation based on useful life assessments. Additionally, Viasat's reliance on government contracts, which could be subject to policy changes and budget cuts, is balanced by its diversified business model and ongoing efforts to innovate and penetrate new markets.

In conclusion, Viasat's financial performance, strategic acquisitions, and market expansion, coupled with its diversified business model and risk mitigation strategies, suggest a company well-positioned for sustained growth. While the broader economic slowdown and labor market normalization present challenges, Viasat's robust revenue growth and proactive management of risks demonstrate its potential to thrive in the current market environment. Investors should consider Viasat's strong fundamentals and strategic initiatives when evaluating its potential for long-term investment.

The ‘Bear’ Perspective

- High Debt Post-Acquisition: The acquisition of Inmarsat Holdings has significantly increased VSAT's debt load, with secured term loans of $616.7 million and unsecured bridge loans replaced by 7.500% Senior Notes due 2031.

- Satellite Anomalies and Operational Risks: VSAT has reported satellite anomalies, which could affect the reliability and lifespan of its services, leading to potential revenue loss and increased maintenance costs.

- Market and Competitive Pressures: Intense competition in the communications technology sector and the risk of rapid technological obsolescence could hinder VSAT's ability to maintain and grow its market share.

- Regulatory and Contractual Vulnerabilities: A significant portion of VSAT's revenue is tied to U.S. Government contracts, making it susceptible to policy shifts and budget constraints.

- Economic and Geopolitical Uncertainties: Global economic headwinds and geopolitical tensions, such as sanctions from China, could disrupt supply chains and reduce customer spending, impacting VSAT's bottom line.

Elaboration on Key Points

- Debt Concerns Post-Inmarsat Acquisition

The recent acquisition of Inmarsat Holdings has left Viasat with a hefty debt burden. The financing structure, comprising $616.7 million in secured term loans and $733.4 million in unsecured bridge loans, now replaced by high-interest Senior Notes, significantly increases the company's financial liabilities. The 7.500% interest on the Senior Notes due 2031 will add considerable interest expenses to the balance sheet. This debt load could restrict Viasat's operational flexibility and eat into future earnings, making the stock a less attractive investment. - Satellite Anomalies and Operational Risks

Viasat has acknowledged satellite anomalies, which raise concerns over the reliability of its communications infrastructure. Satellites are capital-intensive assets with high risks of malfunction, potentially leading to unexpected operational costs and revenue losses. The finite lifespan of these satellites and the possibility of premature failure could necessitate costly replacements or repairs, impacting Viasat's profitability and long-term financial stability. - Market and Competitive Pressures

Viasat operates in a highly competitive industry, where rapid technological advancements can quickly render existing products and services obsolete. Larger competitors with more resources could outpace Viasat in innovation and market penetration. Additionally, Viasat's market share could be compromised by emerging technologies and shifting consumer preferences, making it challenging for the company to sustain its growth trajectory. - Regulatory and Contractual Vulnerabilities

With a substantial portion of its revenue hinging on U.S. Government contracts, Viasat's financial performance is vulnerable to changes in federal spending and policy. Any reductions in defense budgets or shifts in government priorities could lead to contract cancellations or non-renewals, which would have a direct and potentially severe impact on Viasat's revenue streams. - Economic and Geopolitical Uncertainties

The current economic climate, marked by inflationary pressures and potential interest rate hikes, could dampen consumer and corporate spending. Geopolitical tensions, such as trade disputes and international sanctions, pose additional risks. For instance, sanctions from China could hinder Viasat's ability to conduct business in one of the world's largest markets, potentially leading to significant revenue losses and operational disruptions.

In conclusion, while Viasat Inc. has made strategic moves to expand its global footprint, the accumulation of debt, operational risks, competitive pressures, reliance on government contracts, and exposure to economic and geopolitical uncertainties make it a precarious investment at this time. Investors should carefully consider these factors, which could significantly affect the company's future performance and stock valuation.

Comments ()