Unum Group (UNM), Mid/Small Cap AI Study of the Week

While rising interest rates can lead to improved investment yields, they have also contributed to a massive net unrealized loss for Unum Group, totaling $4.2 billion on fixed maturity securities...

December 7th, 2023

Weekly AI Pick from the S&P 400 or S&P 600

Unum Group (UNM)

Company Overview

Unum Group is a multinational financial protection and insurance provider operating mainly in the United States, the United Kingdom, and Poland. The company offers a diverse range of products including disability, life, accident, critical illness, dental, and vision insurance, which are primarily marketed through workplaces. Unum's business is structured into three main segments: Unum US, Unum International, and Colonial Life, with Unum US being the largest and focusing on group disability, life, and voluntary benefits. The company's revenue generation hinges on premium collections, which take into account factors like expected claims, administrative costs, and investment income.

The company is looking to grow by investing in technology and operations, and by expanding into new markets. Growth prospects include the expansion of Unum UK and Unum Poland, leveraging their distribution expertise, and the development of voluntary benefits products. However, Unum UK has ceased marketing supplemental products to individual customers starting in 2022, and the Closed Block segment discontinued offering individual long-term care insurance.

Unum Group also engages in reinsurance to manage risks, including a major transaction in 2020 with Global Atlantic Financial Group to reinsure part of its individual disability business. The company maintains catastrophic reinsurance coverage and has a captive reinsurance subsidiary in the US. Despite measures to minimize credit risk, the inability of a reinsurer to fulfill their obligations could adversely affect Unum's operations.

The company's financial performance is influenced by various factors including investment strategy, which aims to align cash flows from assets and liabilities, and maintaining high-quality investments for consistent returns. Unum's creditworthiness is assessed by major rating agencies, and the company's competitive edge in the insurance industry depends on factors such as customer service, product offerings, pricing, and financial strength. Success also relies on the ability to attract and retain independent agents and brokers who market Unum's products.

By the Numbers

- Net Income (2022): $1,314.2 million, up from $824.2 million in 2021.

- After-tax Adjusted Operating Income (2022): $1,254.3 million ($6.21 per share), up from $890.7 million ($4.35 per share) in 2021.

- Unum US Income Before Tax (2022): Increased by 65.6%.

- Colonial Life Adjusted Operating Income (2022): Grew by 13.8%.

- Closed Block Segment Income Before Tax and Net Investment Gains (2022): Rose by 29%.

- Closed Block Segment Adjusted Operating Income (2022): Declined by 37.2% after exclusions.

- Unum UK Profit (2022): Increased by 37.7%.

- International Segment Adjusted Operating Income (2022): Increased by 20.2% in U.S. dollars.

- Total Sales Across All Segments (2022): Improved significantly.

- Net Unrealized Loss on Fixed Maturity Securities (2022): $3.0 billion.

- Share Repurchase (2022): 5.7 million shares at a cost of around $200 million.

- Total Revenue (2022): $11.991 billion, down from $12.013 billion in 2021 and $13.162 billion in 2020.

- Adjusted Operating Revenue (2022): Stable at $12.007 billion.

- Income Before Income Tax (2022): $1.631 billion, showing a significant increase over three years.

- Policy and Contract Benefits Reserves (End of 2022): $44.7 billion, down from $45.3 billion at the end of 2021.

For the third quarter of 2023:

- Net Income (Q3 2023): $202.0 million, down from $510.3 million in Q3 2022.

- Net Income (First Nine Months of 2023): $953.2 million, down from $1,118.0 million in 2022.

- After-tax Adjusted Operating Income (Q3 2023): $381.7 million, up from $332.3 million in Q3 2022.

- U.S. Segment Income Before Tax and Net Investment Gains/Losses (Q3 2023): $486.6 million, up from $451.6 million.

- Colonial Life Income Before Tax (Q3 2023): $183.6 million; for nine-month period: $393.0 million.

- Closed Block Segment Loss (Q3 2023): $354.9 million.

- Unum UK Sales (Q3 2023): Decreased by 41.1%; for nine-month period: increased by 15.4%.

- Net Unrealized Loss on Fixed Maturity Securities (First Nine Months of 2023): $4.2 billion.

- Share Repurchase (2023): 3.9 million shares.

- Risk-Based Capital Ratio (As of September 30, 2023): 470%.

- Adjusted Operating Income (2023): $490.2 million, up from $416.2 million in 2022.

- Liabilities for Future Policy Benefits (End of Q3 2023): $36.5 billion, down from $38.6 billion at the end of 2022.

- Total Income Before Tax (First Nine Months of 2023): -$177.2 million due to cash flow assumption updates.

These figures provide a snapshot of Unum Group's financial health and performance over the reported periods.

Stock Performance and Technical Analysis

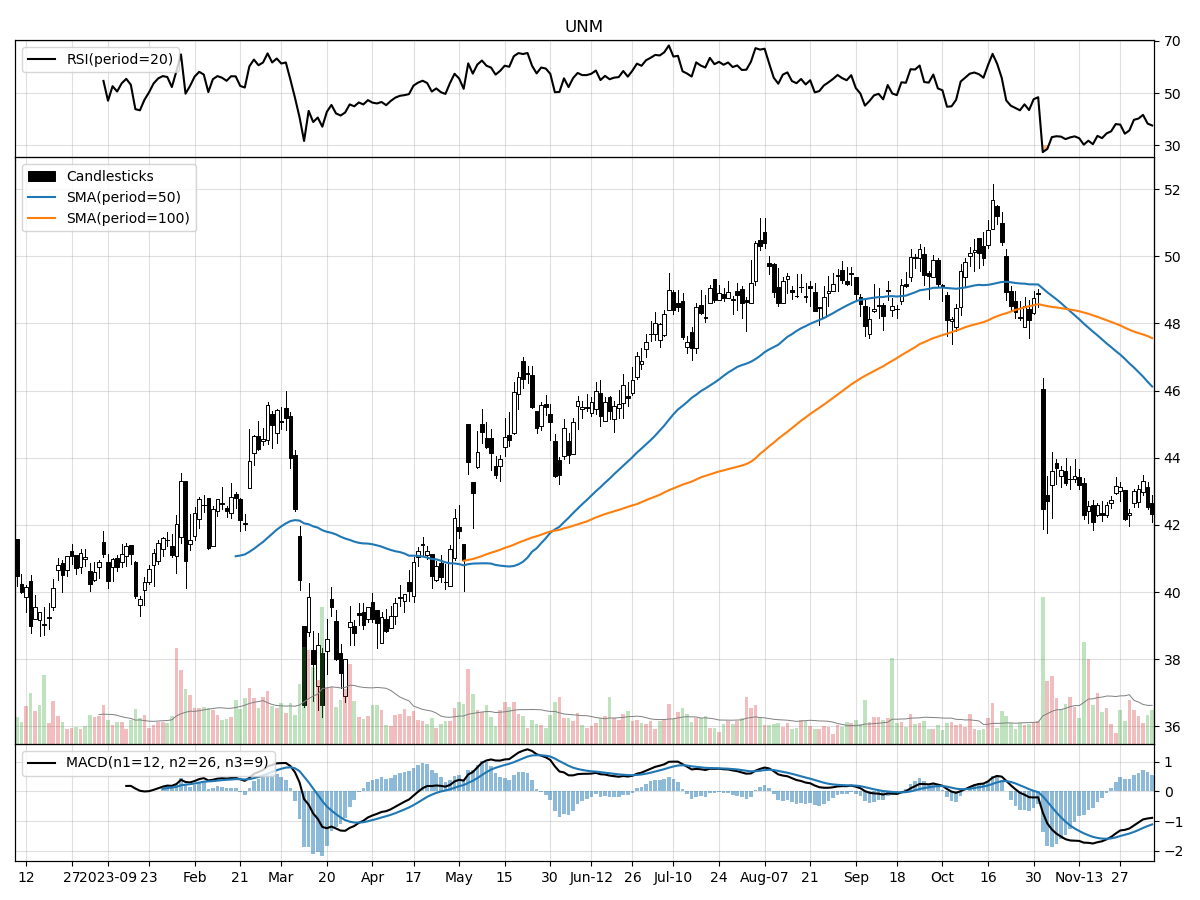

Starting with the price action, the current stock price of $42.34 is positioned between its 52-week high and low, which suggests moderate volatility over the past year. Sitting 15% above its 52-week low and 18% below its 52-week high implies that the stock has recently pulled back from its peak levels, potentially indicating a correction or a bearish trend. The recent price drop of approximately 2.13% over the last month, coupled with stability over the last three months, suggests that the stock is experiencing a period of consolidation or that it has found a temporary support level from which it could either break down or rebound, depending on upcoming market conditions and investor sentiment.

Volume analysis can provide additional context to the price action. The recent daily volume is higher than the longer-term average, which could mean that more traders and investors are taking interest in the stock, often a sign of increased liquidity and potential volatility. Money Flow indicators suggesting moderate selling pressure and distribution imply that there might be a greater number of sellers in the market, leading to potential downward pressure on the stock price.

Finally, the Moving Average Convergence Divergence (MACD) is bearish at -1.11. The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a stock’s price. A bearish MACD indicates that the short-term momentum is moving downward more rapidly than the long-term momentum, which could suggest that the stock is losing strength and may continue to decline in the short term.

In summary, the technical indicators for this stock present a bearish outlook in the near term. The combination of the recent price decline, increased volume, selling pressure, distribution activity, and a negative MACD all suggest that the stock might face further downward movement. As a stock analyst, it would be prudent to consider these technical signals along with fundamental analysis before making an investment decision. It's also important to monitor any upcoming news or events that could affect the stock's performance and to consider setting stop-loss orders to manage risk in case the stock continues to decline.

The ‘Bull’ Perspective

Unum Group: A Robust Investment Opportunity Amidst Headwinds

Summary:

- Resilient Financial Performance: Despite a challenging quarter, Unum Group's after-tax adjusted operating income has shown growth, increasing to $381.7 million in Q3 2023 from $332.3 million in the same quarter of 2022.

- Strategic Share Repurchases: Unum Group's commitment to shareholder value is evident in its ongoing share repurchase program, with 3.9 million shares bought back, showcasing confidence in the company's intrinsic value.

- Strong Capital Position: The company maintains a robust capital position, with a Risk-Based Capital ratio of 470% as of September 30, 2023, indicating a strong buffer against potential financial distress.

- Diverse Geographic and Market Exposure: Unum Group benefits from a diverse geographic presence and exposure across different case sizes and industries, which helps mitigate risks and capitalize on growth opportunities.

- Proactive Liability Management: The company has managed its liabilities for future policy benefits effectively, reducing them to $36.5 billion at the end of Q3 2023 from $38.6 billion at the end of 2022.

Elaboration:

- Resilient Financial Performance

Unum Group's ability to increase its after-tax adjusted operating income amidst economic turbulence is a testament to its operational resilience. An increase from $332.3 million to $381.7 million year-over-year in Q3 2023, even as net income faced pressures, demonstrates the underlying strength of its core business operations. This growth in operational income is particularly noteworthy given the broader industry challenges, including increased claims and the impact of the Covid-19 pandemic. Moreover, this performance indicates that Unum's management is effective in navigating the company through cyclical downturns and positioning it for long-term success. - Strategic Share Repurchases

The company's share repurchase program signals management's belief in the undervaluation of its stock, providing an immediate return to shareholders and underscoring a commitment to capital allocation efficiency. By buying back 3.9 million shares, Unum Group not only returns value to its shareholders but also consolidates future earnings across fewer outstanding shares, potentially boosting earnings per share and investor confidence. This strategy is often viewed positively by the market as it can reflect the company's strong cash flow generation and a bullish outlook by insiders about the company's future prospects. - Strong Capital Position

With a Risk-Based Capital ratio of 470%, Unum Group stands on solid ground to withstand financial headwinds. This ratio far exceeds the regulatory requirements, providing a substantial cushion against market volatility and unexpected losses. A strong capital position is particularly vital in the insurance industry, where confidence in the company's ability to meet its obligations is paramount. It also affords Unum the flexibility to invest in growth opportunities and navigate the current rising interest rate environment, which could improve investment yields over time. - Diverse Geographic and Market Exposure

Unum Group's presence across multiple regions and sectors diversifies its risk and enables it to tap into various market dynamics. For instance, while Unum UK experienced a sales decrease in Q3 2023, the company saw a 24.1% increase in sales over the first nine months of the year. This diversification helps the company balance out the fluctuations in individual markets and maintain a steady revenue stream. Moreover, exposure to different case sizes and industries means that Unum is not overly reliant on any single segment, making it more resilient to sector-specific downturns. - Proactive Liability Management

Effective liability management is crucial for insurance companies, and Unum Group has demonstrated its capability in this area by reducing its liabilities for future policy benefits. This decrease from $38.6 billion to $36.5 billion reflects the company's proactive approach to managing its long-term obligations, which can lead to a more favorable balance sheet and potentially lower capital requirements. It also suggests that Unum is actively managing its product mix and reinsurance strategies to optimize its risk profile.

Conclusion:

In light of the recent news headlines and identified risks, Unum Group's strong performance and strategic initiatives position it well to navigate the current landscape. While the tragic Las Vegas campus shooting underscores the unpredictable nature of risk in society, Unum's role in providing financial protection benefits remains critical. The company's risk management practices and diversified exposure help mitigate the impact of such events and broader market uncertainties. Moreover, the proactive management of liabilities and capital strength provides a buffer against the identified risks, including regulatory changes and economic fluctuations. With these factors in mind, Unum Group presents a compelling investment opportunity for those looking to add a resilient and strategically positioned company to their portfolio.

The ‘Bear’ Perspective

Title: A Prudent Stance on Unum Group: Why Investors Should Exercise Caution

Summary:

- Declining Net Income: Unum Group reported a significant drop in net income, from $510.3 million in Q3 2022 to $202.0 million in Q3 2023, raising concerns about the company's profitability.

- Interest Rate Environment: The rising interest rate environment presents both opportunities and risks, but the net unrealized loss of $4.2 billion on fixed maturity securities is alarming.

- Operational Challenges: Despite some areas of operational strength, the Closed Block segment reported a substantial loss, and Unum UK experienced a notable decrease in sales in Q3.

- Regulatory and Market Risks: Regulatory changes and market volatility pose significant risks to Unum Group's financial stability and future performance.

- Reputation and Competition: Unum Group's ability to maintain its market position is threatened by increased competition and reputational risks.

Elaboration:

- Declining Net Income

Unum Group's net income has seen a troubling decline, plummeting by over 60% from the same quarter in the previous year. This stark decrease from $510.3 million to $202.0 million in Q3 2023 is a red flag for investors, signaling potential underlying issues with profitability and sustainability. The nine-month performance also mirrors this downtrend, with net income falling to $953.2 million from $1,118.0 million. When a company's bottom line is shrinking at such a rate, it's a clear indicator that investors should proceed with caution, as this trend can reflect deeper financial or operational problems that may not be immediately apparent. - Interest Rate Environment

While rising interest rates can lead to improved investment yields, they have also contributed to a massive net unrealized loss for Unum Group, totaling $4.2 billion on fixed maturity securities. This figure cannot be ignored, as it represents a substantial portion of the company's investment portfolio that has lost value. Although these are unrealized losses and could potentially reverse, the current financial statements reflect a weakened position that could affect the company's ability to leverage its investments for growth or to buffer against future liabilities. - Operational Challenges

Unum Group's operational performance presents a mixed picture. On one hand, the U.S. segment and Colonial Life showed income growth before tax year-over-year. However, the Closed Block segment's loss of $354.9 million in Q3 2023 is concerning. Additionally, the international arm's performance, particularly the 41.1% decrease in Unum UK sales for Q3, suggests that the company is facing significant challenges in key markets. These operational inconsistencies could lead to unpredictability in future earnings, making it difficult for investors to assess the company's true health. - Regulatory and Market Risks

Regulatory changes are a constant threat to insurance companies like Unum Group. An increase in regulatory costs or a shift in policy that affects customer demand can have immediate and detrimental impacts on profitability. Moreover, the company's exposure to market risks, such as sustained low interest rates or issuer defaults, adds another layer of uncertainty. With the ongoing economic fluctuations and the potential for heightened regulatory scrutiny, investors could find themselves facing diminishing returns and increased volatility. - Reputation and Competition

Reputational risks, including litigation and non-compliance issues, can have far-reaching consequences for companies like Unum Group. In an industry where trust is paramount, any damage to the company's reputation can lead to a loss of customers and a decline in market share. Additionally, the insurance market is highly competitive, with customer service quality, pricing, financial strength, and regulatory compliance all playing critical roles in maintaining a competitive edge. Unum's ability to respond to these competitive pressures while managing reputational risks is crucial, and any missteps could result in a significant setback for the company.

In conclusion, while Unum Group has demonstrated some areas of operational resilience, the combination of declining net income, substantial unrealized investment losses, operational challenges, regulatory and market risks, and the ever-present threat of competition and reputational damage paint a picture of a company that is currently facing more headwinds than tailwinds. Investors should carefully consider these factors and exercise due diligence before making investment decisions regarding Unum Group's stock.

Comments ()