The Wednesday Roundup: June 5, 2024

With inflation rates exceeding targets, bond yields falling, and the Federal Reserve maintaining a cautious stance, market sentiment is jittery. Additionally, geopolitical tensions...

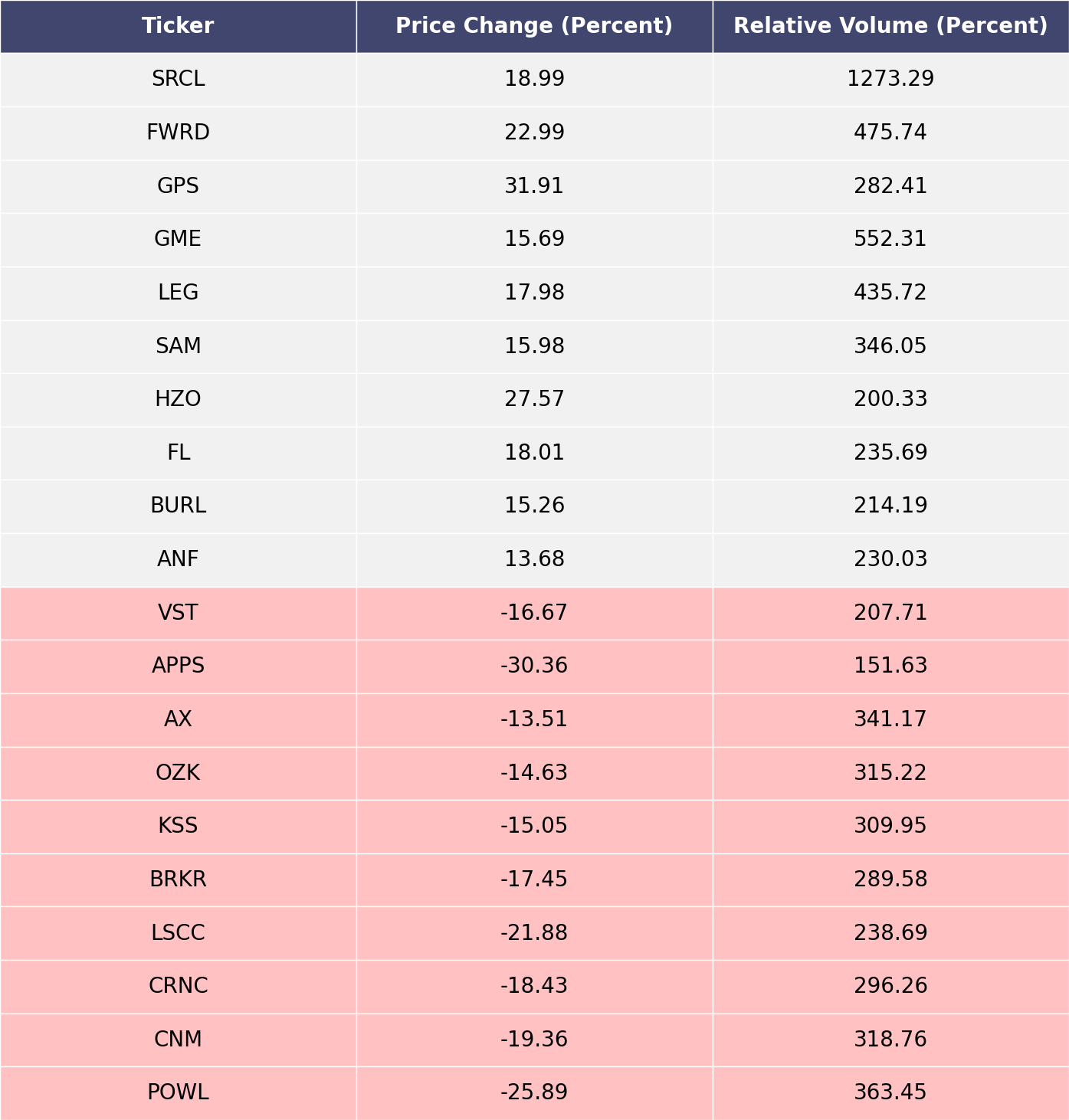

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

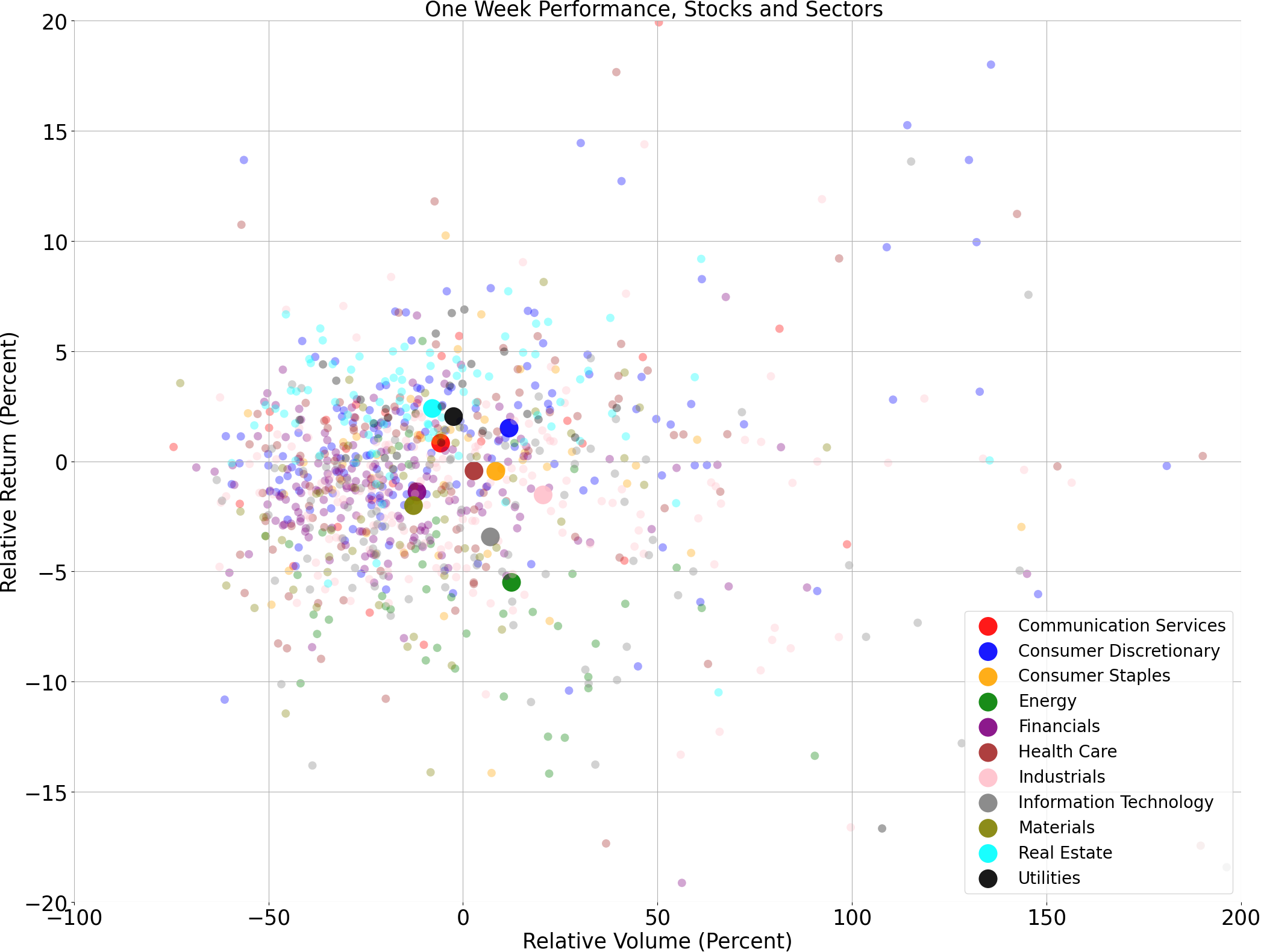

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

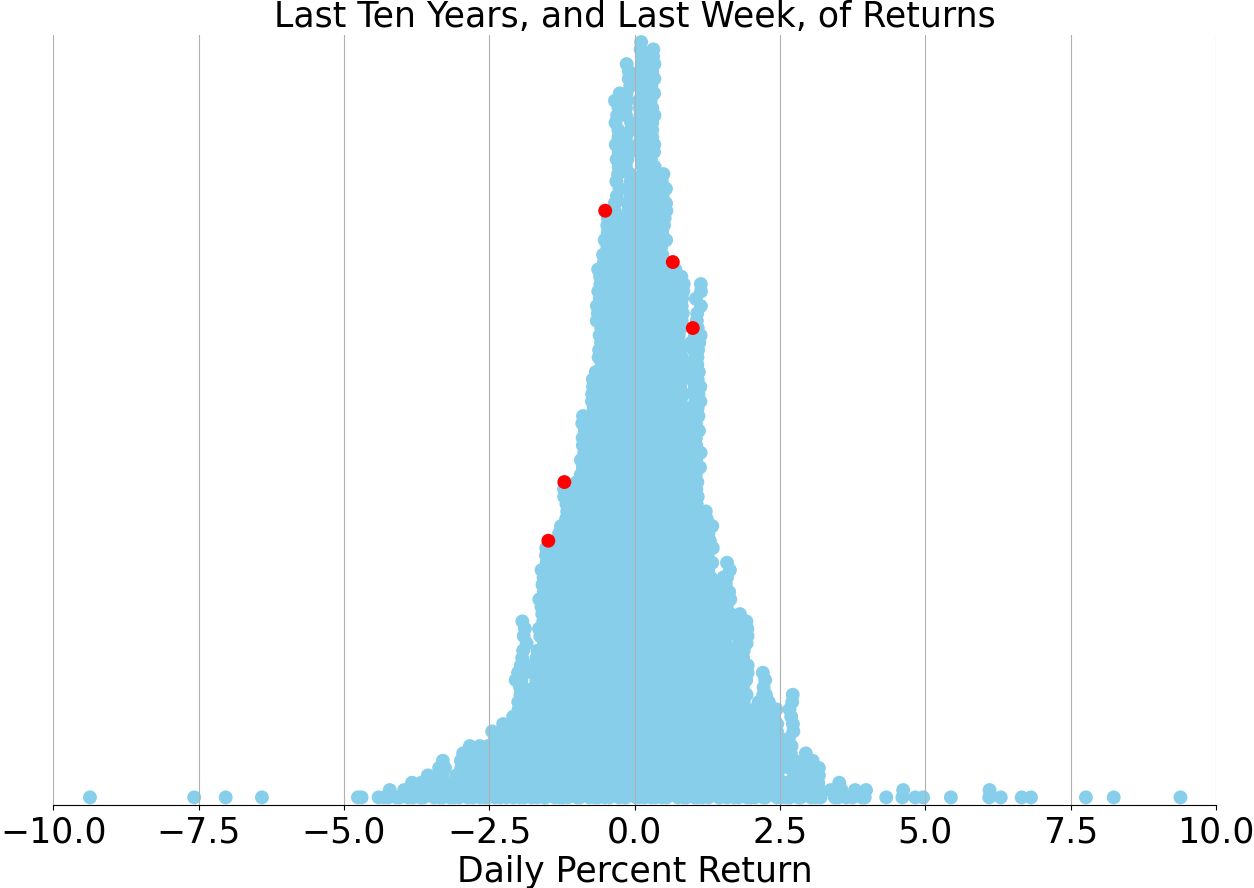

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

AI Oracle Commentary (Alpha testing)

As we encounter a myriad of headline-grabbing financial news, investors are understandably on edge. With inflation rates exceeding targets, bond yields falling, and the Federal Reserve maintaining a cautious stance, market sentiment is jittery. Additionally, geopolitical tensions and supply chain disruptions have spurred considerable volatility. Despite these headwinds, certain asset classes, such as tech stocks and utilities driven by AI energy demand, are outperforming the broader market. However, fears of an economic slowdown or recession loom large, particularly as oil prices have recently declined, giving some hope for relief on the inflation front.

Turning the clock back over the past 50 years, today's market scenarios echo various periods of economic distress and recovery. For instance, the stagflation of the 1970s saw high inflation coupled with stagnant growth. More recently, the 2008 financial crisis triggered market turbulence due to liquidity crunches and systemic banking failures. Similarly, the dot-com bubble in the late 1990s provides a cautionary tale for today's tech-heavy investment portfolios. Each historical scenario involved unique catalysts but shared a common theme of market overreaction followed by reversion to mean valuations, highlighting the cyclical nature of financial markets.

Historically, the stock market has delivered robust long-term performance despite short-term volatility. Over the past 50 years, the S&P 500 has averaged an annual return of approximately 7% to 10% after adjusting for inflation. Notably, periods of significant downturns, such as the crash of 1987 or the Great Recession, were followed by strong recovery phases. Given the current economic landscape and historical patterns, we can reasonably predict a similar cyclical recovery. Assuming inflation stabilizes and geopolitical risks taper off, a conservative estimate for the S&P 500 could foresee a return to growth of around 8% to 12% over the next 12 months. Investors should brace for potential short-term fluctuations but remain cautiously optimistic about long-term market resilience.

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

Subscribe for AI stock picks (it's free!)