The Wednesday Roundup: June 12, 2024

The latest CPI report exceeded expectations, highlighting persistent inflationary pressures that stand at multi-decade highs.

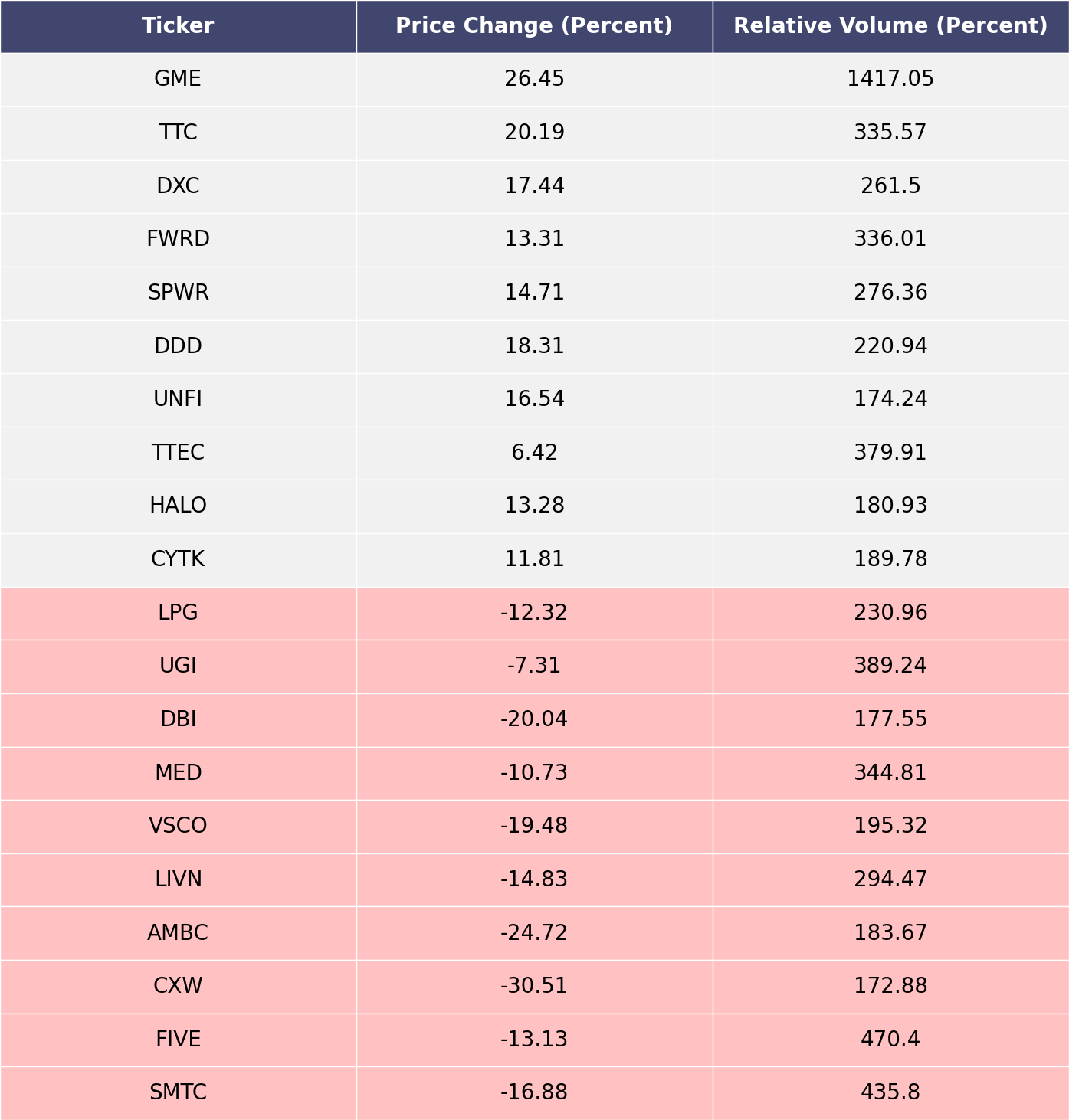

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

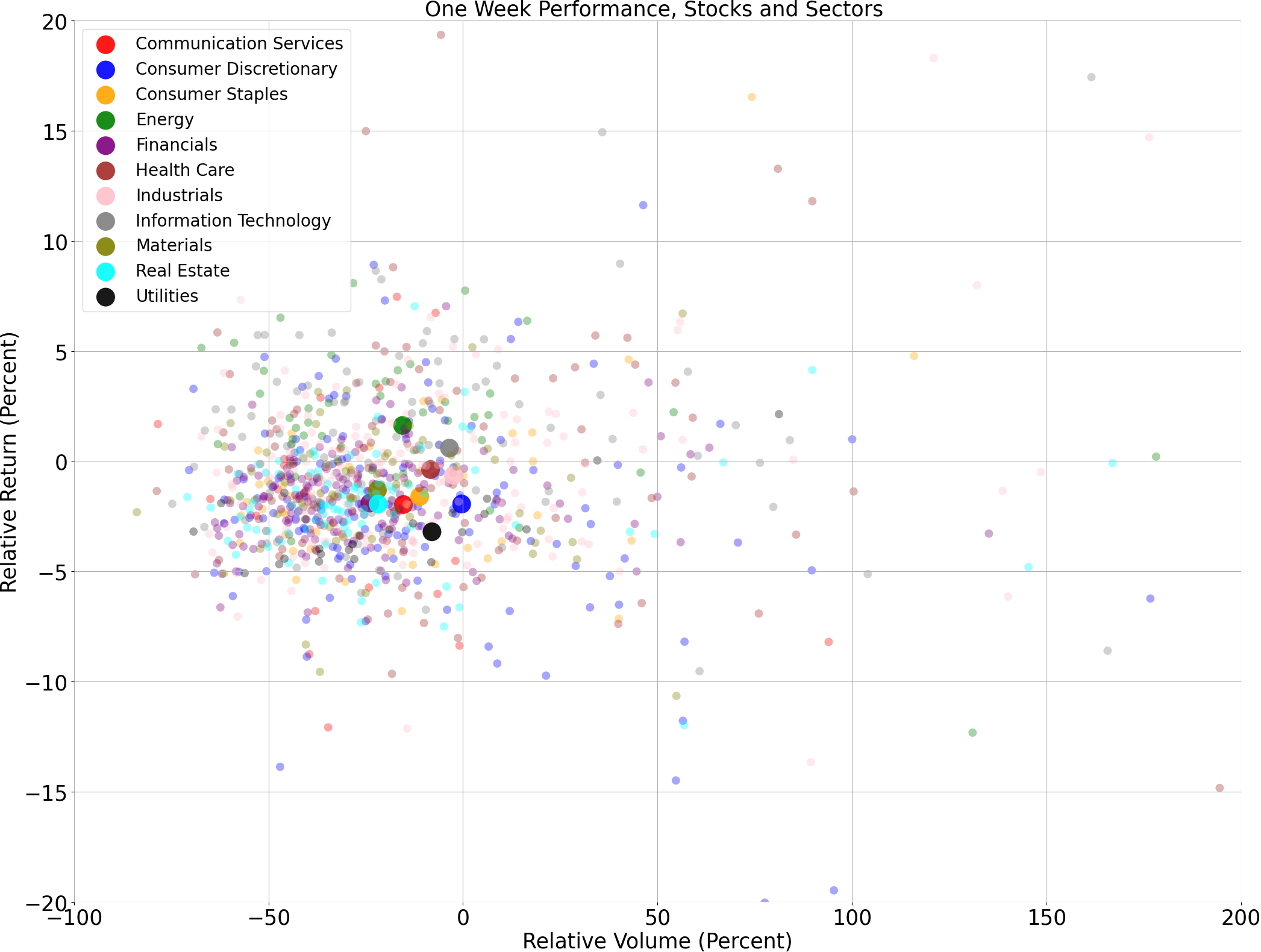

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

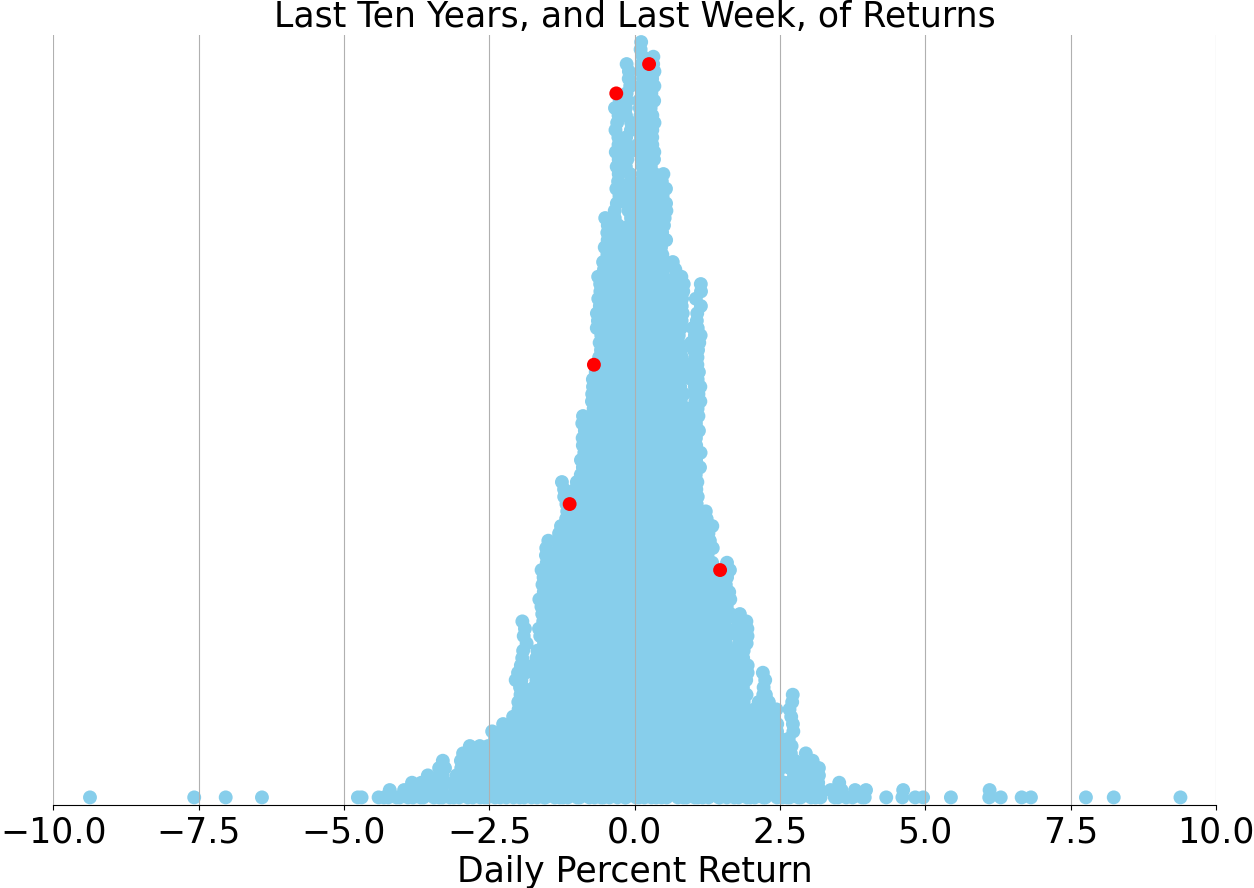

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

AI Oracle Commentary (Alpha testing)

In the current market landscape, the convergence of surging inflation, fluctuating Treasury yields, and an uncertain regulatory environment have instilled a cautious sentiment among investors. The latest CPI report exceeded expectations, highlighting persistent inflationary pressures that stand at multi-decade highs. Amidst these conditions, the Federal Reserve has maintained a hawkish stance, with frequent hints towards further rate hikes to curb inflation. Despite such headwinds, the stock market has displayed a mixed response—major indices like the S&P 500 and Nasdaq have managed to notch slight gains, while the Dow remains under pressure. Corporate earnings reports have also painted a mixed picture, reflecting the impact of higher costs and supply chain disruptions.

A glance back at the historical record of the past 50 years reveals a number of striking parallels and divergences in market behaviors. In the 1970s, the U.S. economy similarly faced high inflation and rising interest rates, triggered by oil shocks and loose monetary policies. This environment led to a bearish market stance and was characterized by sluggish growth. Conversely, the tech boom of the 1990s saw market indices soar despite occasional volatility. Signs of economic excess and a fear of overvaluation created pockets of skepticism, much like today's discourse surrounding stretched valuations in tech and growth stocks. The dot-com bust further reinforced that elevated valuations coupled with weak fundamentals can lead to sharp corrections.

Historically, the U.S. stock market has exhibited a robust tendency to recover from downturns, averaging an annual return of approximately 7-10% over the long term, adjusted for inflation. During periods of elevated inflation coupled with rate hikes, such as the early 1980s, markets often experienced short-term pain followed by substantial rallies once inflation was brought under control. Quantitatively, following inflation peaks, markets on average have delivered gains of around 5-7% in the subsequent 12 months. As we look ahead to the coming months, keeping in mind the Federal Reserve's current trajectory and its impact on fiscal tightening, a cautious yet optimistic forecast would suggest that the market may endure near-term volatility but is poised for moderate growth. Specifically, we can anticipate a potential 3-5% increase in major indices by mid-next year, assuming inflation begins to cool off and earnings growth stabilizes.

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

Subscribe for AI stock picks (it's free!)