The Wednesday Roundup: January 3, 2024

Our weekly Wednesday article, focusing on the mid/small cap S&P 400 and 600 indices. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

- Mailed to FREE newsletter subscribers (Covered on Thursday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

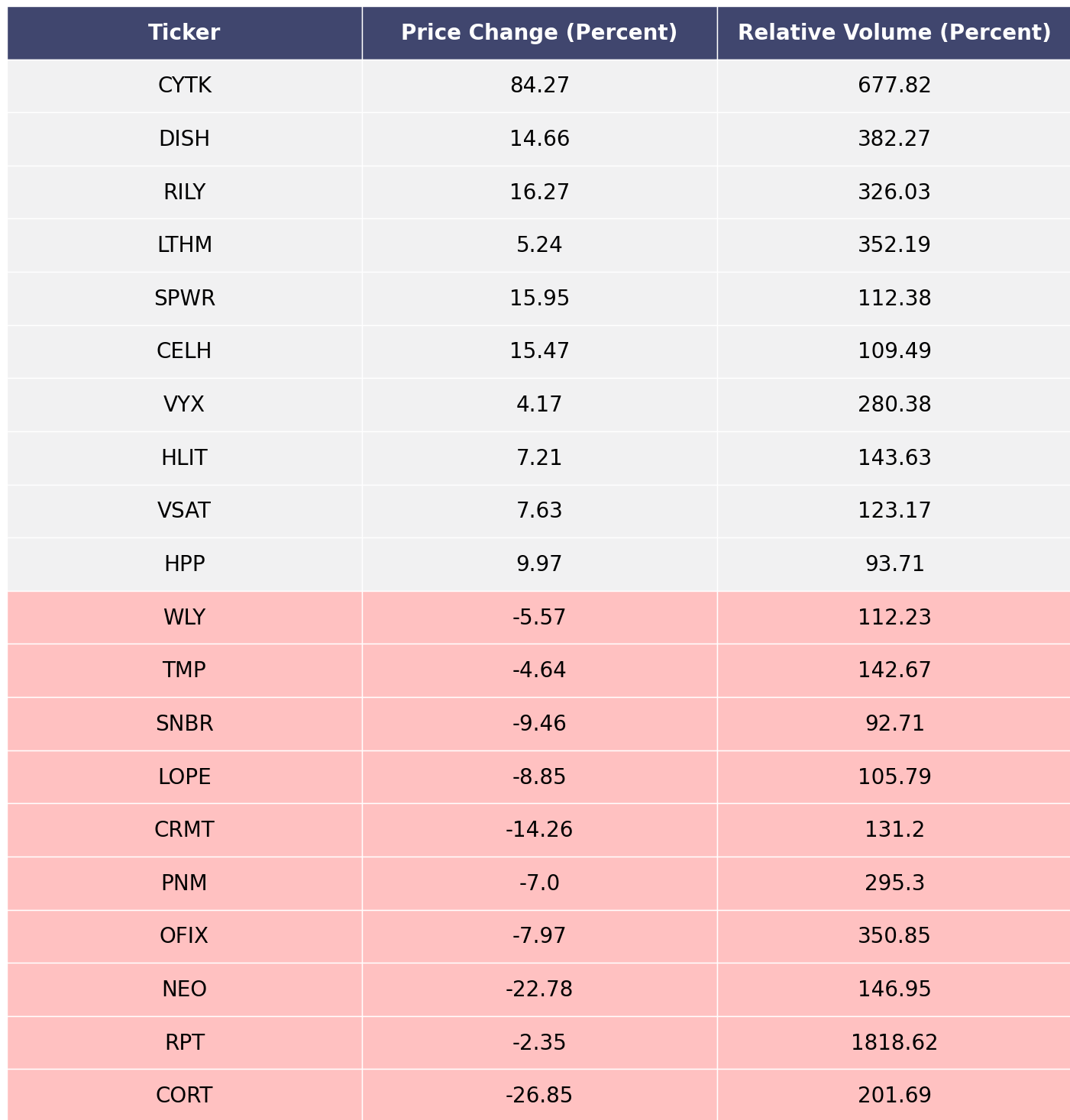

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

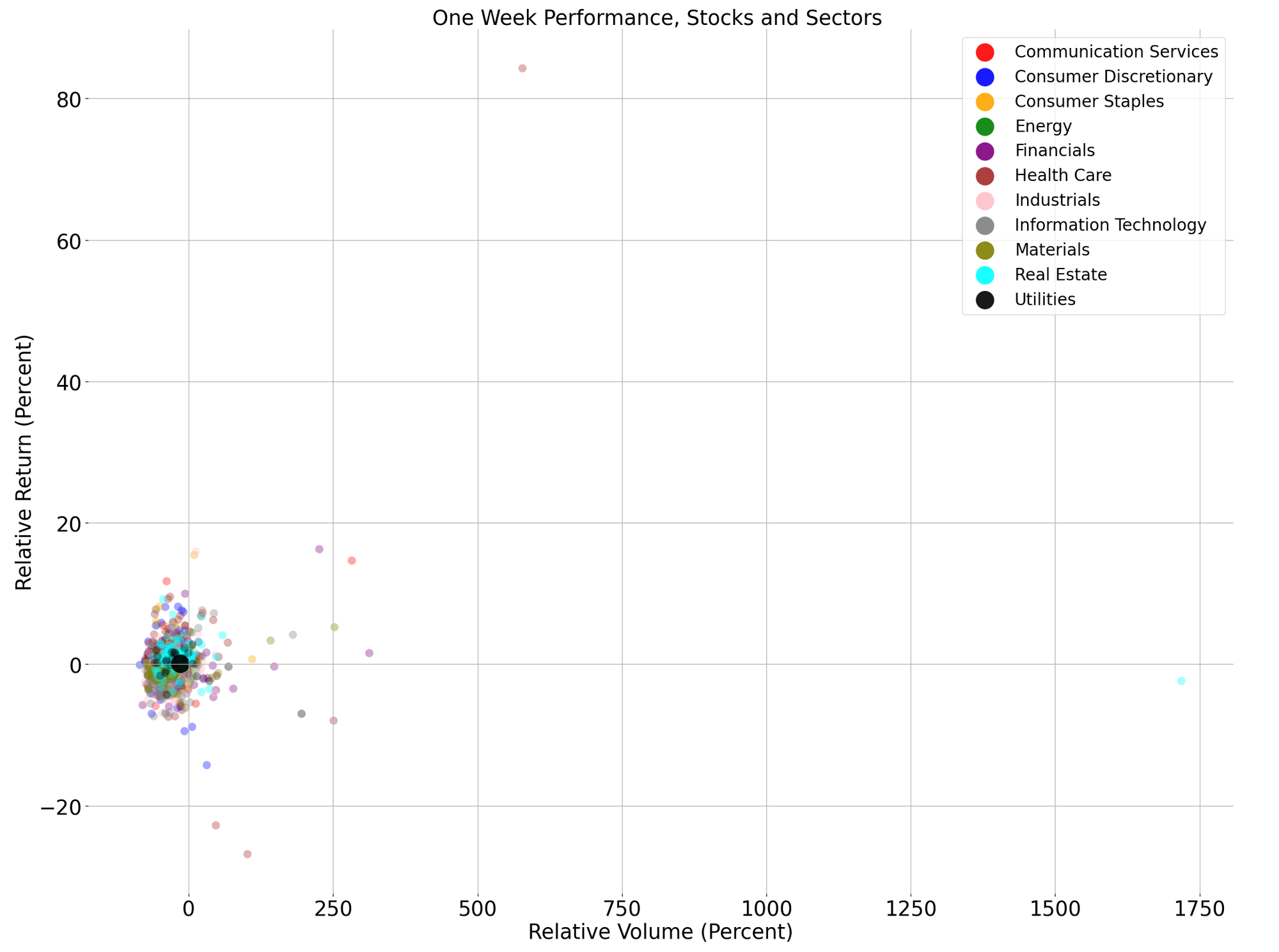

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

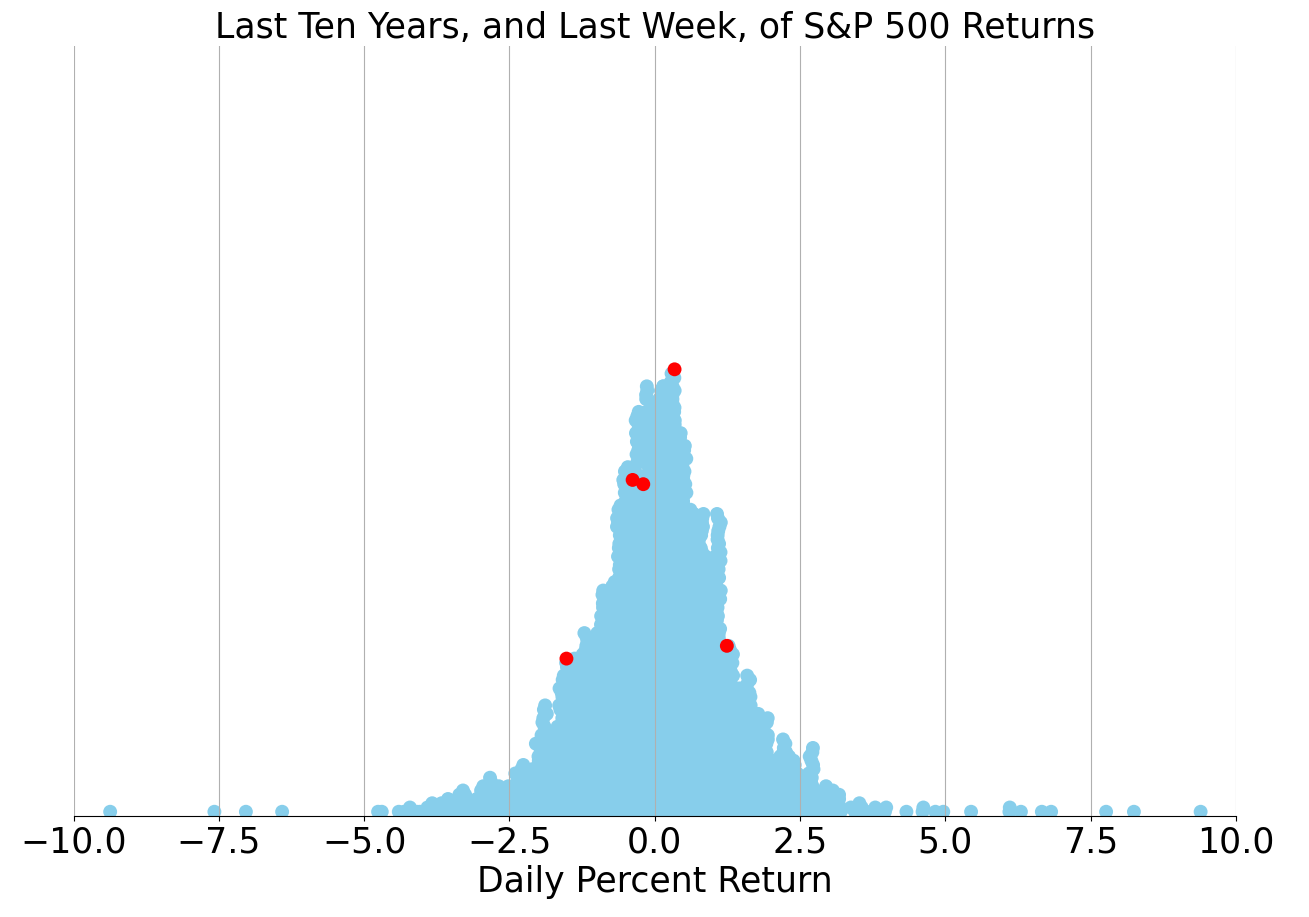

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

Markets Rally on Dovish Fed Outlook as Rate Cut Expectations Mount

Markets Rally as Inflation Eases and Fed Signals a Pivot

As the year 2023 drew to a close, the financial markets experienced a significant turnaround, defying the gloomy expectations set at the outset. Investors navigated a complex landscape marked by the highest borrowing costs seen in over two decades, a regional bank crisis, and persistent geopolitical tensions. Despite these challenges, the economy showed remarkable resilience, and the markets ended on a high note, buoyed by a trend toward disinflation, the cessation of the Federal Reserve's tightening cycle, and burgeoning excitement over advancements in artificial intelligence (AI).

A key factor in the year's market success was the notable slowdown in inflation. After peaking at an alarming 9.1% in mid-2022, inflation rates have been substantially reduced, with the consumer price index (CPI) falling by two-thirds. This disinflationary trend was aided by lower oil and gas prices, which helped bring the headline CPI under 3%. Moreover, as supply chains recalibrated post-pandemic, goods prices fell, and although services inflation remains high, it too is on a downward trajectory.

Looking ahead to 2024, the disinflationary trend is expected to persist. Analysts predict that wage growth will moderate and sectors like used car sales and housing inflation will continue to cool. Housing, which constitutes a significant portion of the CPI, is expected to experience a more accelerated moderation later in the year, aligning with data on new leases and home prices.

March 2023 saw a shift in focus from inflation to financial stability as the banking sector came under scrutiny. The collapse of Silicon Valley Bank (SVB) and Signature Bank, followed by troubles at First Republic Bank and Credit Suisse, rattled confidence. Unlike the 2008 crisis, which was driven by excessive risk-taking and bad loans, this crisis was triggered by rapid rate hikes that devalued the bond securities held by banks. Policymakers responded swiftly, ensuring depositor confidence and stabilizing the situation.

Despite the banking sector's hiccup, the overall financial system remains robust. The latter part of the year saw stabilization in deposit outflows and a recovery in bank shares, particularly among larger banks. However, the sector still faces headwinds from potential increases in commercial real estate loan defaults and the prospect of stricter capital requirements regulation, which could affect profitability.

The labor market and consumer spending were the highlights of 2023, contributing to the avoidance of a full-blown recession. While manufacturing and housing investments waned, robust spending on services and a tight labor market, with an unemployment rate touching half-century lows, supported economic growth. Moving into 2024, economic growth is expected to slow initially but could rebound later in the year as consumption patterns shift and productivity increases.

Finally, the Fed's policy trajectory was a dominant influence on market dynamics throughout the year. After a series of rate hikes brought the policy rate to a 22-year peak, the Fed signaled a major pivot at year's end, suggesting that the tightening cycle had concluded and hinting at potential rate cuts in 2024. This pivot, alongside easing inflation, has led to optimism for a soft landing for the economy.

In summary, the year 2023 was a testament to the value of staying invested through uncertain times. With all asset classes showing positive returns, the year ahead holds promise, particularly as the Fed prepares to adjust rates in response to moderating inflation. Corporate earnings are on the rebound, and valuations in certain sectors remain attractive, offering a favorable outlook for investors in 2024.

Comments ()