The Wednesday Roundup: January 24, 2024

As we approach the tail end of January 2024, investors are navigating a market landscape that has been nothing short of bumpy. Following a robust rally in the final quarter of 2023, where the S&P 500 surged by over 15%, markets have entered a phase of consolidation.

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers (Covered on Thursday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

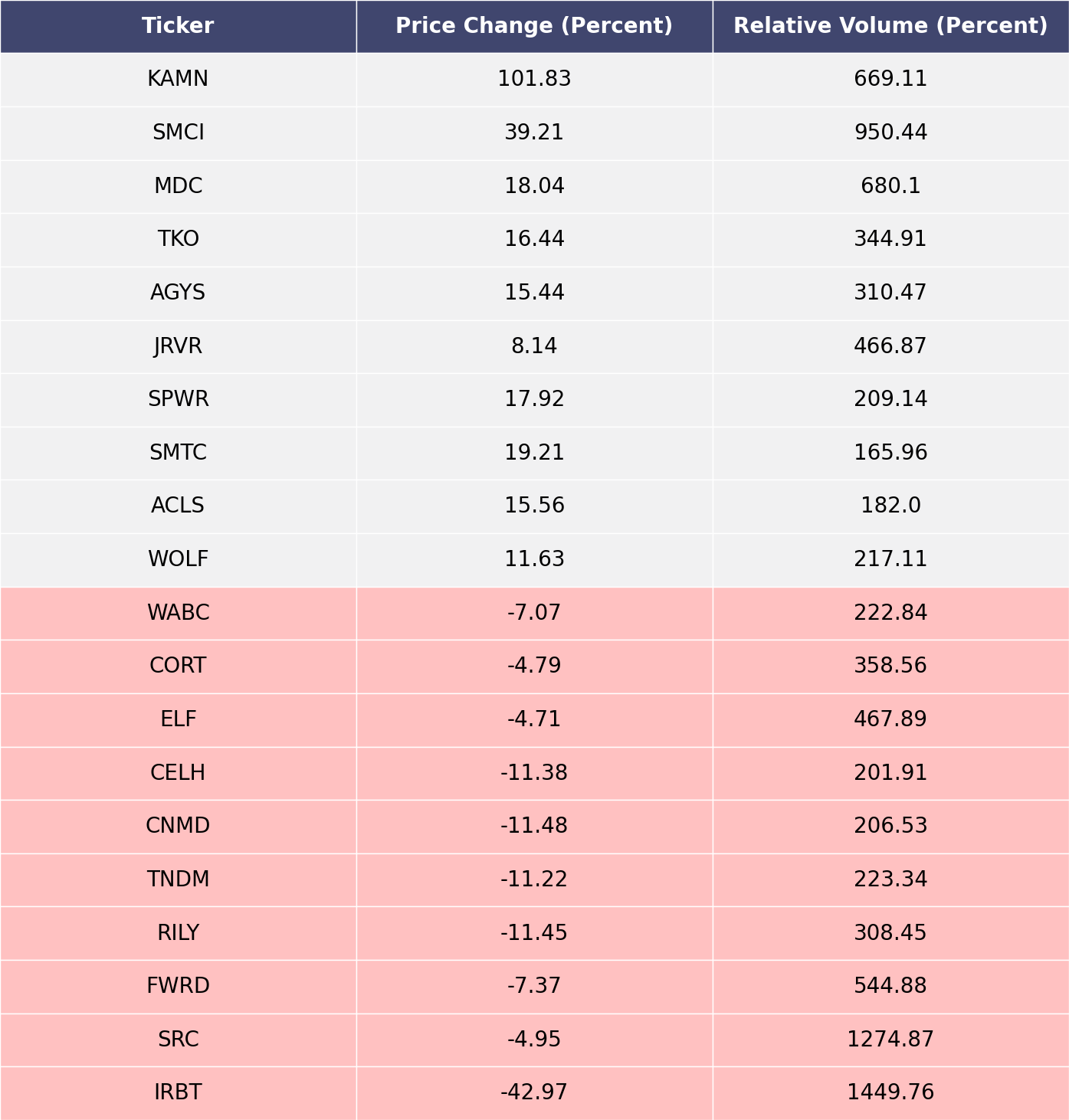

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

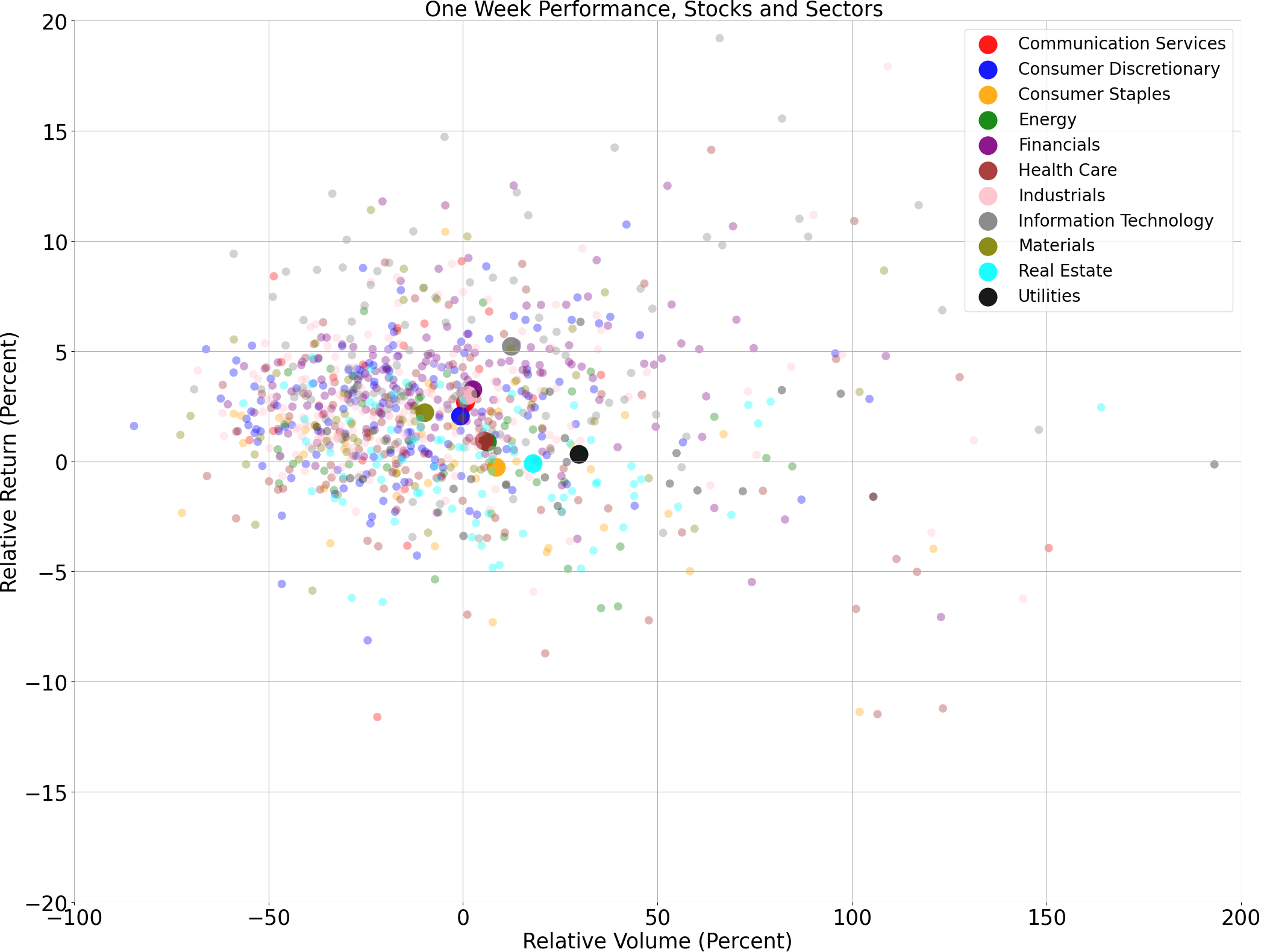

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

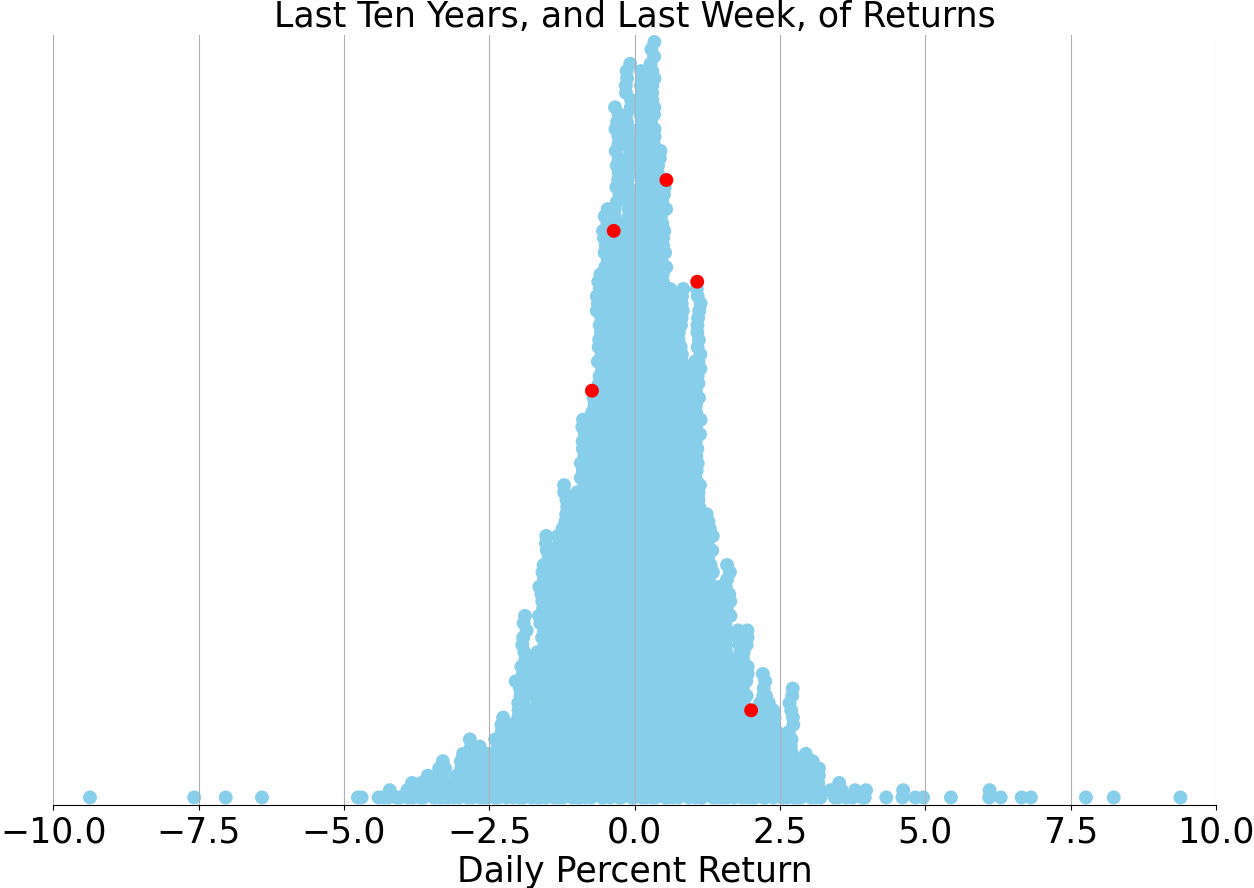

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

Markets Navigate a Tumultuous January Amidst Mixed Signals

As we approach the tail end of January 2024, investors are navigating a market landscape that has been nothing short of bumpy. Following a robust rally in the final quarter of 2023, where the S&P 500 surged by over 15%, markets have entered a phase of consolidation. Despite the S&P 500's modest year-to-date gain of 0.2%, beneath the surface, we're witnessing some shifts as small-cap stocks and investment-grade bonds, which previously showed vigor, now face downward pressures. The technology and communication services sectors continue to spearhead the market, while defensive segments like health care and consumer staples are also outperforming, hinting at an underlying cautious sentiment among investors.

Historically, the performance of the markets in January has been viewed as a barometer for the rest of the year, but recent trends have bucked this notion. Since 1990, only 40% of the years that started off with a negative January ended with a negative annual return for the S&P 500. Despite the rocky start to 2024, it's not necessarily an omen for the remaining months. Investors are keeping a close eye on key economic indicators such as GDP growth and consumer spending, which are expected to slow down before potentially rebounding later in the year. This anticipation of a slowdown has been reflected in the reduced probability of a Federal Reserve rate cut in March, which has dropped from over 70% to just above 50%.

As we delve into the final weeks of January, several economic data points stand out. U.S. real GDP and consumption figures are projected to decelerate in the near term, setting the stage for a possible resurgence in the latter half of 2024. The Federal Reserve's actions remain a focal point, with the market still betting on eventual rate cuts, albeit with less certainty on the timing. This cautious stance is further underscored by the recent normalization of interest rates, with the 10-year Treasury yield now breaching the 4.0% mark.

The current market volatility is seen by some strategists as an opportune moment for investors to recalibrate their portfolios. The swift rally at the end of 2023 may have left some investors lagging, and the present fluctuations provide a chance to diversify and incorporate quality investments. Looking ahead, the themes of broader market leadership and improved performance from investment-grade bonds are expected to unfold throughout 2024.

In the coming week, crucial economic data releases such as the fourth-quarter GDP and PCE inflation will be closely scrutinized. These metrics will offer further clarity on the health of the economy and the potential direction of the Fed's monetary policy. While the current market conditions may be unsettling for some, they could pave the way for more favorable investment opportunities as the year progresses.

Mona Mahajan, an Investment Strategist with a distinguished background in equity and fixed income analysis, continues to be a prominent voice in shaping and communicating market perspectives. With regular appearances on financial news outlets and contributions to leading financial publications, Mahajan leverages her expertise from Harvard Business School and the Wharton School to provide investors with insightful analysis.

In conclusion, while a choppy January and the prospect of a less accommodative Federal Reserve may test the resilience of the markets, the potential for economic growth, coupled with easing inflation and strategic rate cuts, may yet foster a conducive environment for investors willing to weather the storm. As always, past performance is not indicative of future results, and investors are reminded to consider their unique objectives and financial situations before making investment decisions.

Comments ()