The Wednesday Roundup: January 17, 2024

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers (Covered on Thursday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

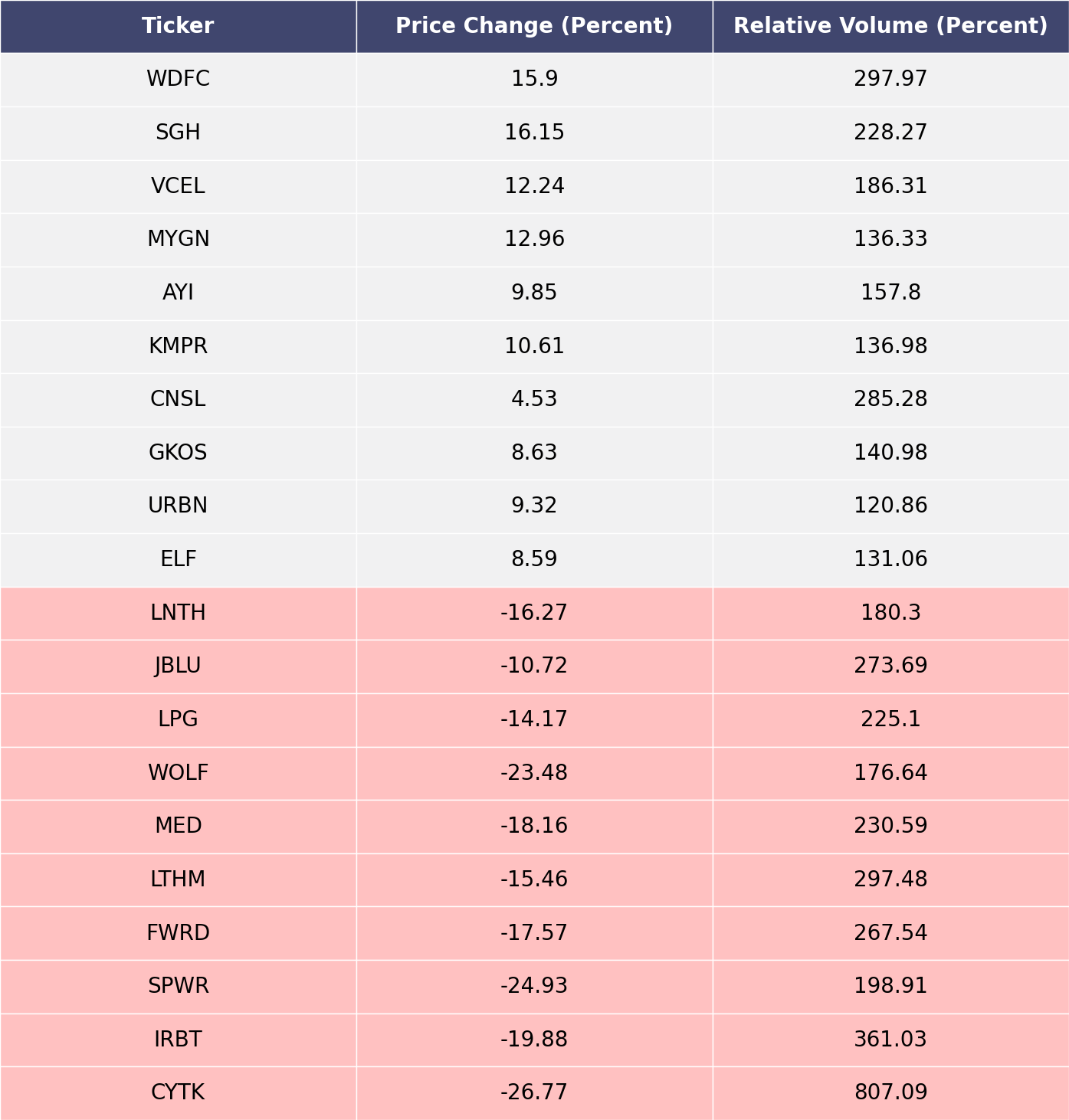

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

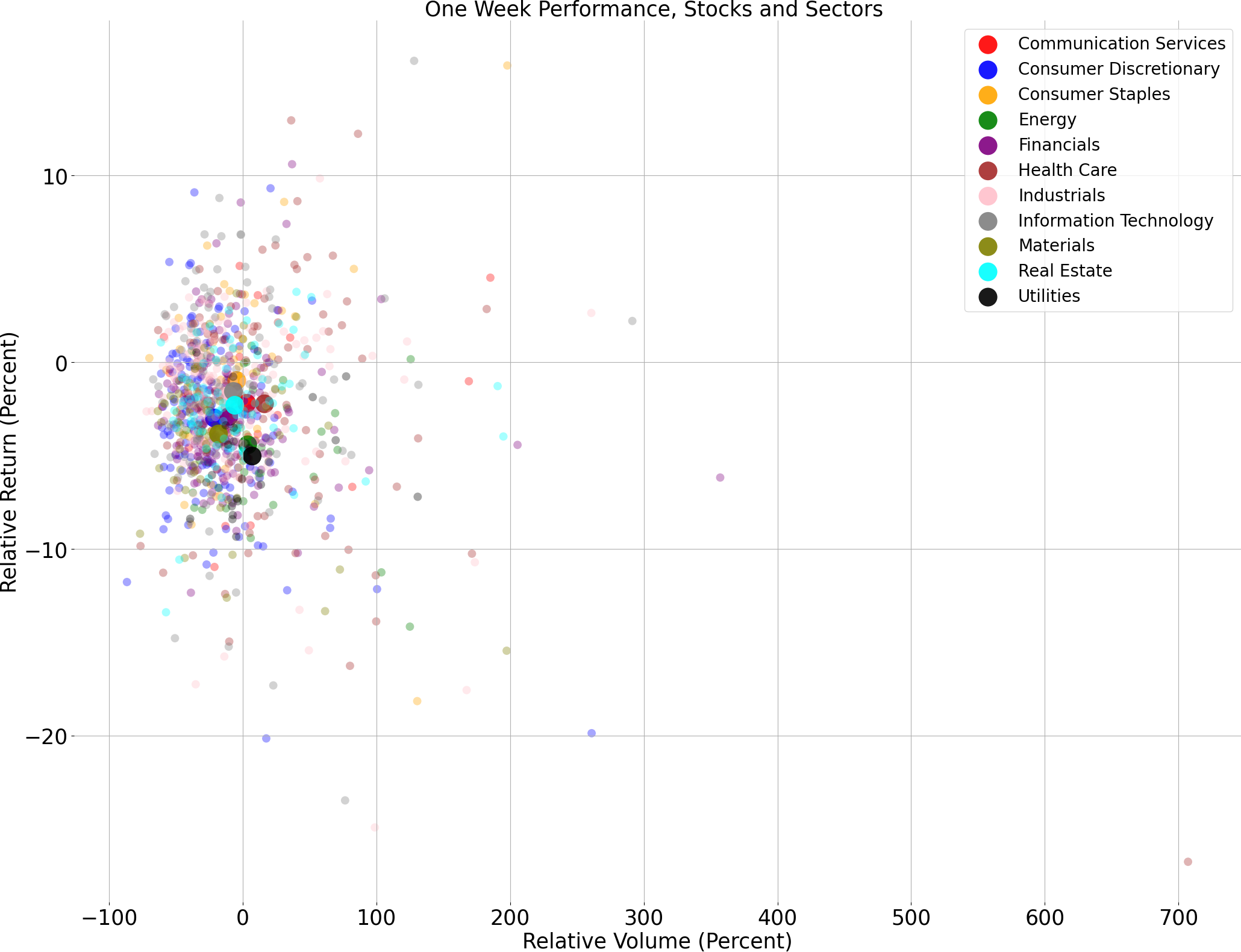

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

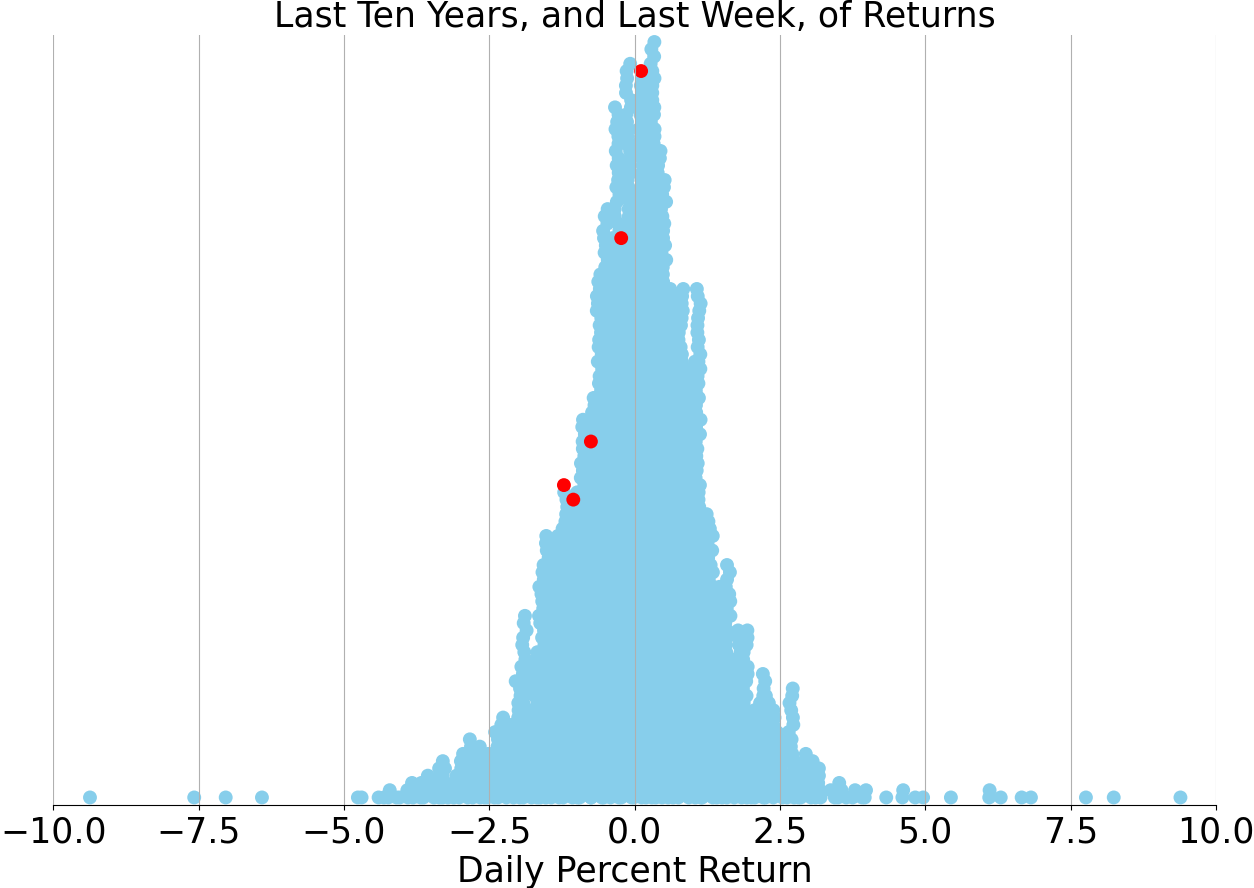

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

Navigating Choppy Waters: Market Insights Amidst Inflation and Interest Rate Tensions

As we delve into the first full trading week of 2024, the financial markets continue to wrestle with the prevailing themes of inflation and the Federal Reserve's monetary policy. With fresh data on consumer prices fueling the ongoing debate around the trajectory of interest rates, investors are left pondering the timing of potential rate cuts. This week's market movements suggest a cautious optimism, as the possibility of a choppier phase looms on the horizon.

The latest figures from the U.S. Consumer Price Index (CPI) indicate a nuanced picture of rent inflation, with the Zillow rent index's growth deceleration potentially hinting at a forthcoming dip in CPI rent inflation. However, investors are reminded that past performance is not a reliable indicator of future results. Concurrently, geopolitical tensions have led to a spike in shipping costs, as evidenced by the uptick in the World Container Index following recent incidents in the Red Sea.

Amidst these developments, the relationship between headline CPI and the Fed policy rate has come under scrutiny. With the year-over-year change in headline CPI still above the Fed's 2% target, the central bank's rate decisions remain a critical focal point for market participants. In the equity space, the forward 12-month earnings estimates for the S&P 500 continue to be a barometer for corporate America's financial health.

Historical patterns also offer some perspective, as data reveals the time taken for the S&P 500 to transition from peak levels to bear market territory. Such trends underscore the unpredictable nature of market cycles, emphasizing the importance of not relying solely on past performance to forecast future market behavior.

As we prepare for the release of key economic data, including retail sales and housing starts, investors are advised to stay abreast of market updates. The interplay of earnings reports, particularly from the financial sector, and macroeconomic indicators will likely shape market sentiment in the coming days.

In summary, while the market has shown resilience this week, particularly in the technology sector, the overall climate remains tinged with caution. As earnings season progresses, the focus will be on whether other sectors can sustain growth and support the narrative of a soft economic landing. With the Fed's communication at odds with market expectations for interest rate cuts, investors are encouraged to stay vigilant and consider the risk-reward dynamics that lie ahead.

Comments ()