The Wednesday Roundup: December 6, 2023

In a significant turn of events that could signal a shift in the U.S. economic landscape, recent data from the Department of Labor indicates that job openings across the country have plummeted to a more than two-and-a-half-year low...

Presenting the first edition of our new weekly Wednesday article, focusing on the mid/small cap S&P 400 and 600 indices. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers (Covered on Tuesday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

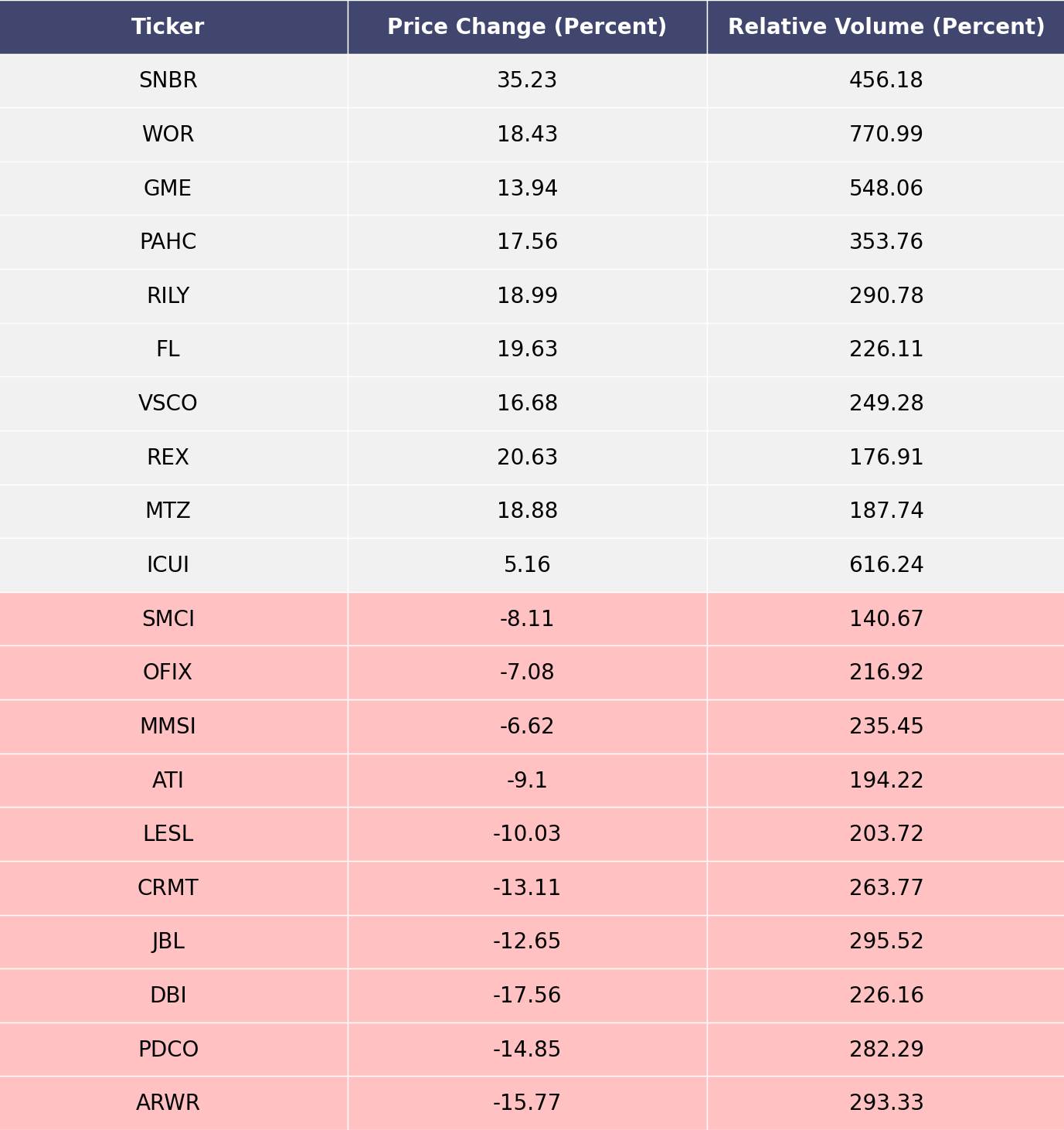

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

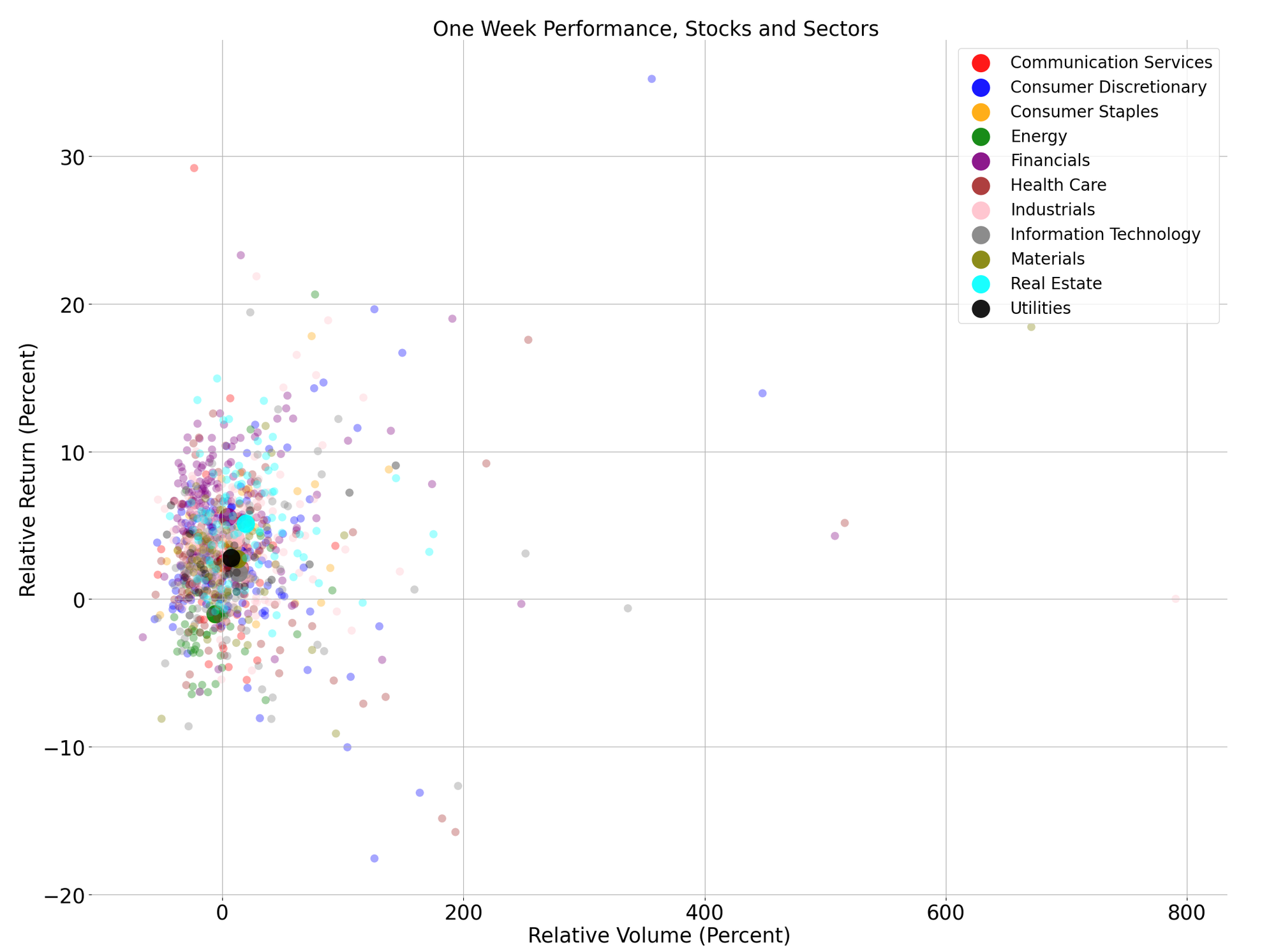

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

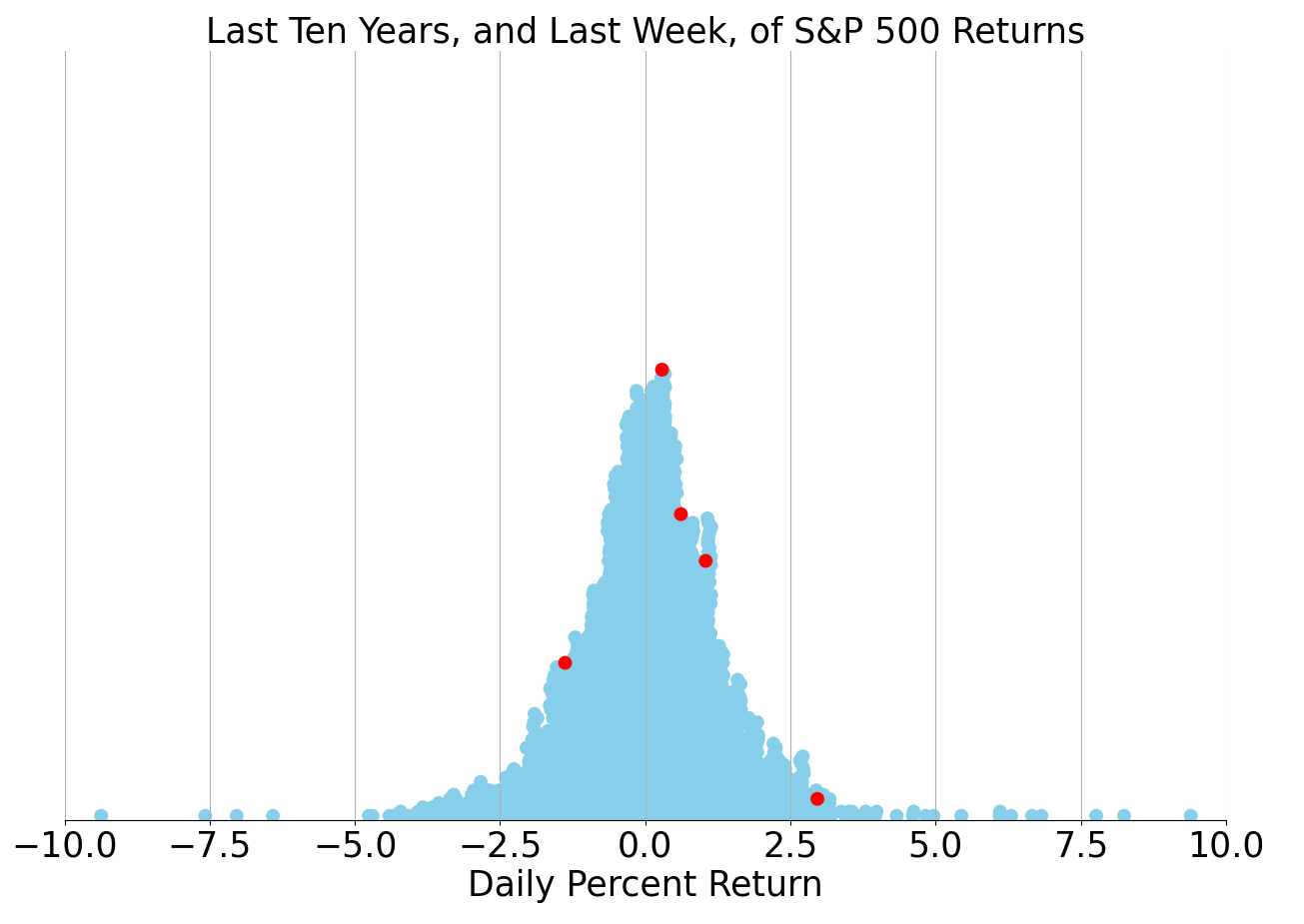

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

Market Commentary

U.S. Labor Market Shows Signs of Cooling as Job Openings Decline

In a significant turn of events that could signal a shift in the U.S. economic landscape, recent data from the Department of Labor indicates that job openings across the country have plummeted to a more than two-and-a-half-year low. This unexpected contraction in the labor market could have wide-ranging implications for investors and policymakers who have been closely monitoring the economy for signs of cooling amid aggressive monetary policy tightening by the Federal Reserve.

The Job Openings and Labor Turnover Survey (JOLTS) reported that job vacancies dropped by 353,000 to 10.3 million on the last business day of November. This marks the lowest level since April 2021 and suggests that employers are becoming more cautious about hiring as the economy navigates through inflationary pressures and interest rate hikes. Economists had anticipated a more modest decrease, and the sharper drop has fueled speculation about a potential softening in the labor market.

The reduction in job openings was widespread, affecting a range of industries. The decline could be interpreted as a lagged response to the Federal Reserve's strategy to combat inflation through higher interest rates, which has increased borrowing costs and cooled demand across sectors. The central bank has been clear about its intentions to restore price stability, even at the risk of triggering a recession.

Investors reacted to the news with caution, as the stock market reflected a mixed sentiment. On one hand, the potential easing of wage inflation could mean that the Fed may be closer to achieving its goals, which might lead to a moderation in the pace of future rate hikes. On the other hand, a weakening job market could presage a broader economic downturn, which would negatively impact corporate earnings and consumer spending.

The tech sector, which has been a barometer for growth expectations, showed signs of vulnerability as companies brace for a potential economic slowdown. High-growth stocks, which are particularly sensitive to interest rate changes, may face additional headwinds if the labor market continues to deteriorate and consumer demand wanes.

Financial stocks, meanwhile, could see a more nuanced impact. While a slower pace of rate hikes might relieve some pressure on loan growth, the prospect of a softening labor market and the potential for increased loan defaults present a complex picture for banks and lending institutions.

The latest labor market data also has implications for the bond market, with yields on Treasuries fluctuating as investors recalibrate their expectations for the Fed's policy path. The bond market's reaction underscores the delicate balance policymakers must strike between curbing inflation and sustaining economic growth.

In the commodities space, the labor market report could influence expectations for energy demand, with oil prices reacting to the evolving economic outlook. A cooler labor market might suggest lower consumption, but geopolitical factors and supply-side constraints continue to contribute to volatility in energy markets.

Looking ahead, market participants will be closely watching for further signs of a shift in the labor market dynamics. The upcoming non-farm payrolls report and other key economic indicators will provide critical insights into the health of the U.S. economy. As the Fed continues to navigate the tightrope of monetary policy, the trajectory of the labor market will be a crucial factor in determining the pace and extent of future interest rate movements.

In conclusion, the latest JOLTS data serves as a reminder of the interconnectedness of employment trends, monetary policy, and market performance. As the U.S. labor market shows signs of cooling, investors and analysts will be vigilant in assessing the potential ripple effects across financial markets, keeping a watchful eye on the delicate interplay between economic indicators and stock market behavior.

Comments ()