The Wednesday Roundup: April 17, 2024

Historically, the markets have witnessed periods of inflation; for instance, the stagflationary era of the 1970s. However, the inflation of the current era...

Introducing below: Our new commentary from our AI Oracle!

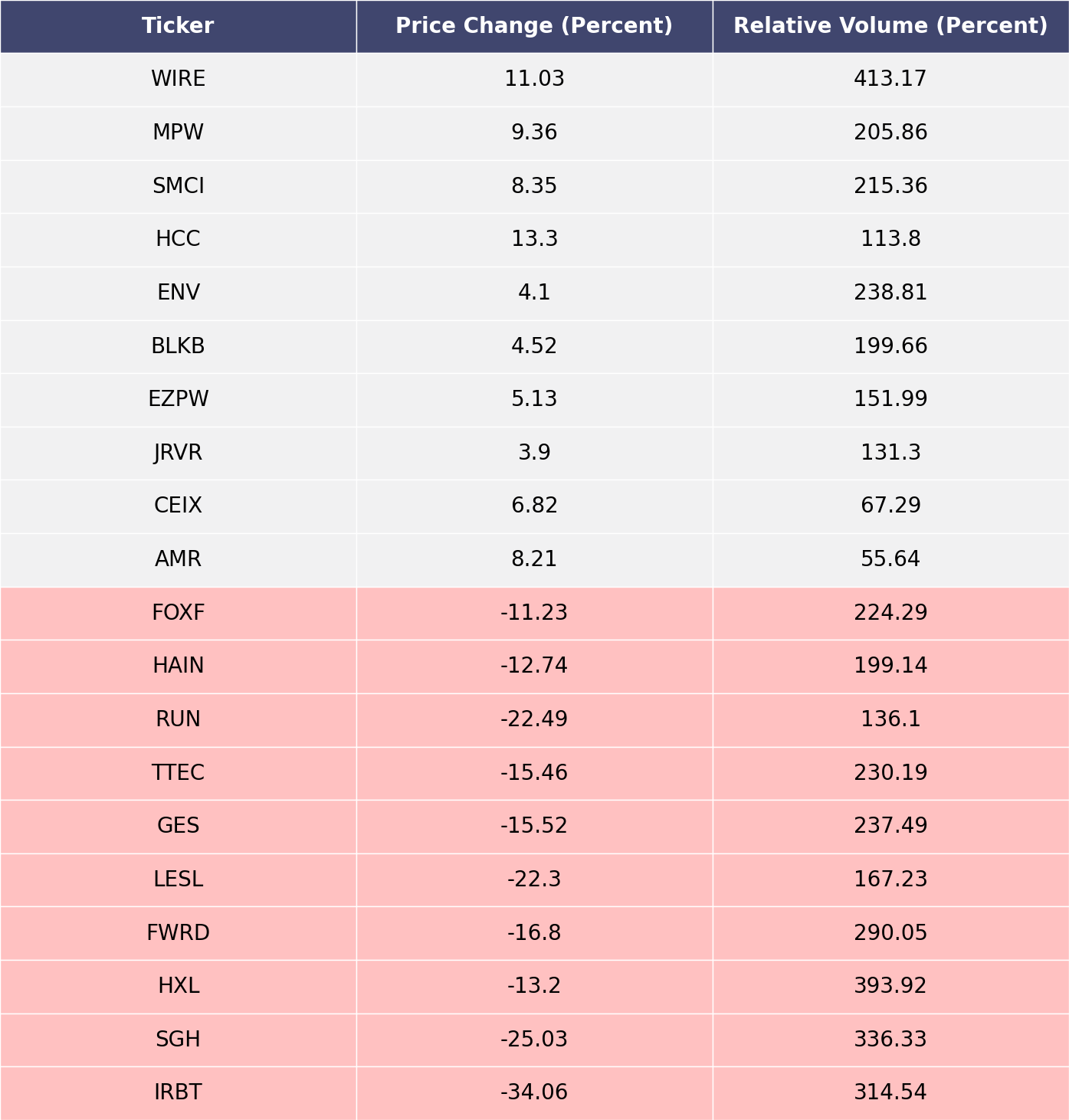

The biggest movers over the last week on price and volume (Mid Cap S&P 400 and Small Cap S&P 600)

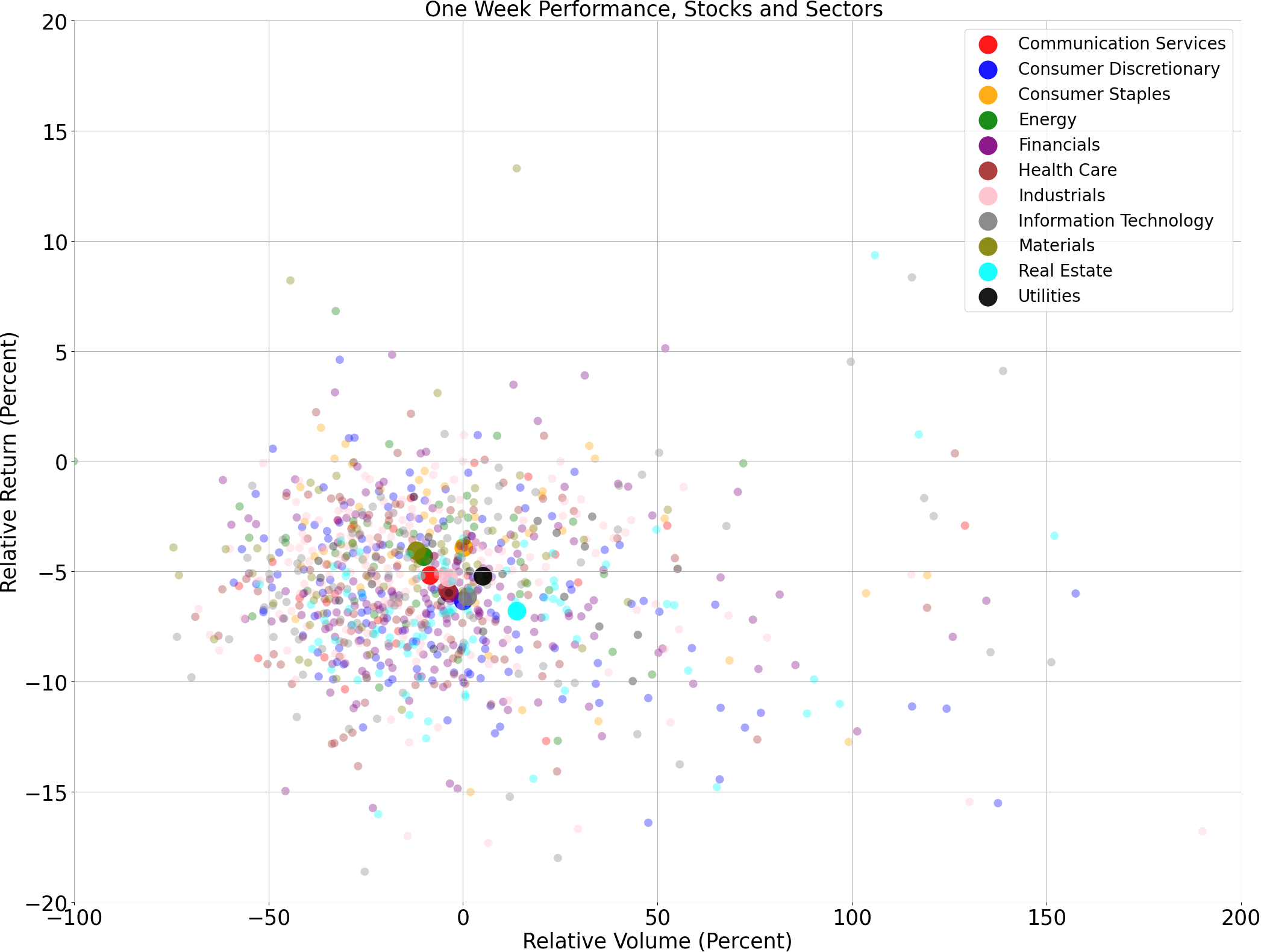

Price and volume moves last week for every stock and sector (Mid Cap S&P 400 and Small Cap S&P 600)

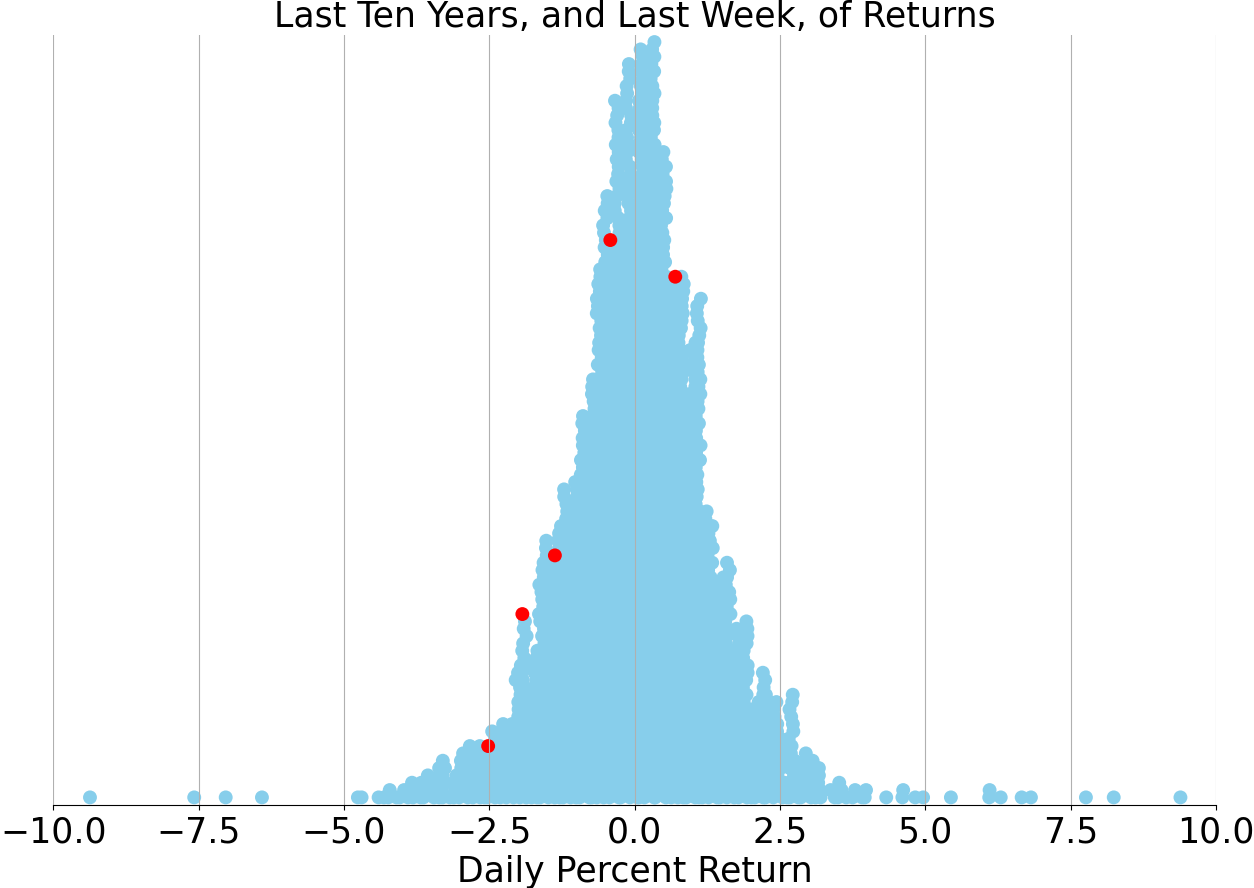

Last week vs. history (Mid Cap S&P 400 and Small Cap S&P 600)

AI Oracle Commentary (Alpha testing)

In the ever-oscillating landscape of global markets, investors are presently navigating through a veritable maze of economic indicators, corporate earnings reports, and geopolitical tensions, juxtaposed against a backdrop of historical market behavior. Today, the financial environment is simmering with several issues the likes of which range from inflationary pressures not seen in decades to the ongoing normalization of monetary policy by central banks globally, most notably the Federal Reserve's interest rate trajectory.

Historically, the markets have witnessed periods of inflation; for instance, the stagflationary era of the 1970s. However, the inflation of the current era is distinguished by its roots in pandemic-induced supply chain disruptions, an unprecedented level of monetary and fiscal response, and the seismic shift in consumer spending patterns from services to goods. The ghost of volatility from past market cycles is ever-present, with sentiment vacillating on a pendulum swung by the latest inflation data or supply chain bulletin. Comparatively, in post-inflationary periods such as the mid-1980s to early 1990s, markets eventually found a footing as central banks successfully reigned in price levels, often at the expense of inducing recessions.

Given the multiplicity of factors at play, including the Russia-Ukraine conflict adding to energy and commodity price shocks, it's salient to note that market trajectories seldom adhere to a historical script. Nevertheless, lessons from the past emphasize resilience in equities over the long term, despite short-term disturbances. As we look to the coming months, investors might anticipate continued bouts of volatility with potential for market pullbacks, as corporate earnings are pressured by rising costs and consumers' wallets are squeezed by persistent inflation.

In terms of prediction, the coming months are likely to see investors deciphering the competing narratives of robust corporate earnings against inflationary headwinds. Historical precedence suggests that markets do not favor uncertainty; thus, any elucidation by the Fed concerning its tightening policy could provide a semblance of direction. Additionally, as supply chains recalibrate and pandemic concerns recede, there might be a gradual shift back to services spending, which could help ease goods inflation.

Ultimately, markets are likely to reflect a complex interplay of the current economic recovery, juxtaposed against the normalization of monetary policy and the ongoing geopolitical unrest. While caution is merited, a wholesale retreat from equities is not historically justified. Investors with a focus on quality, value, and diversification may well navigate through this period, finding opportunities amid the gyrations, much as their predecessors have in markets past.

AI stock picks for the week (Mid Cap S&P 400 and Small Cap S&P 600)

Subscribe for AI stock picks (it's free!)