The Monday Charge: September 30, 2024

Over the past seven weeks, the market has notched an impressive six weekly gains, culminating in an 11% surge since early August.

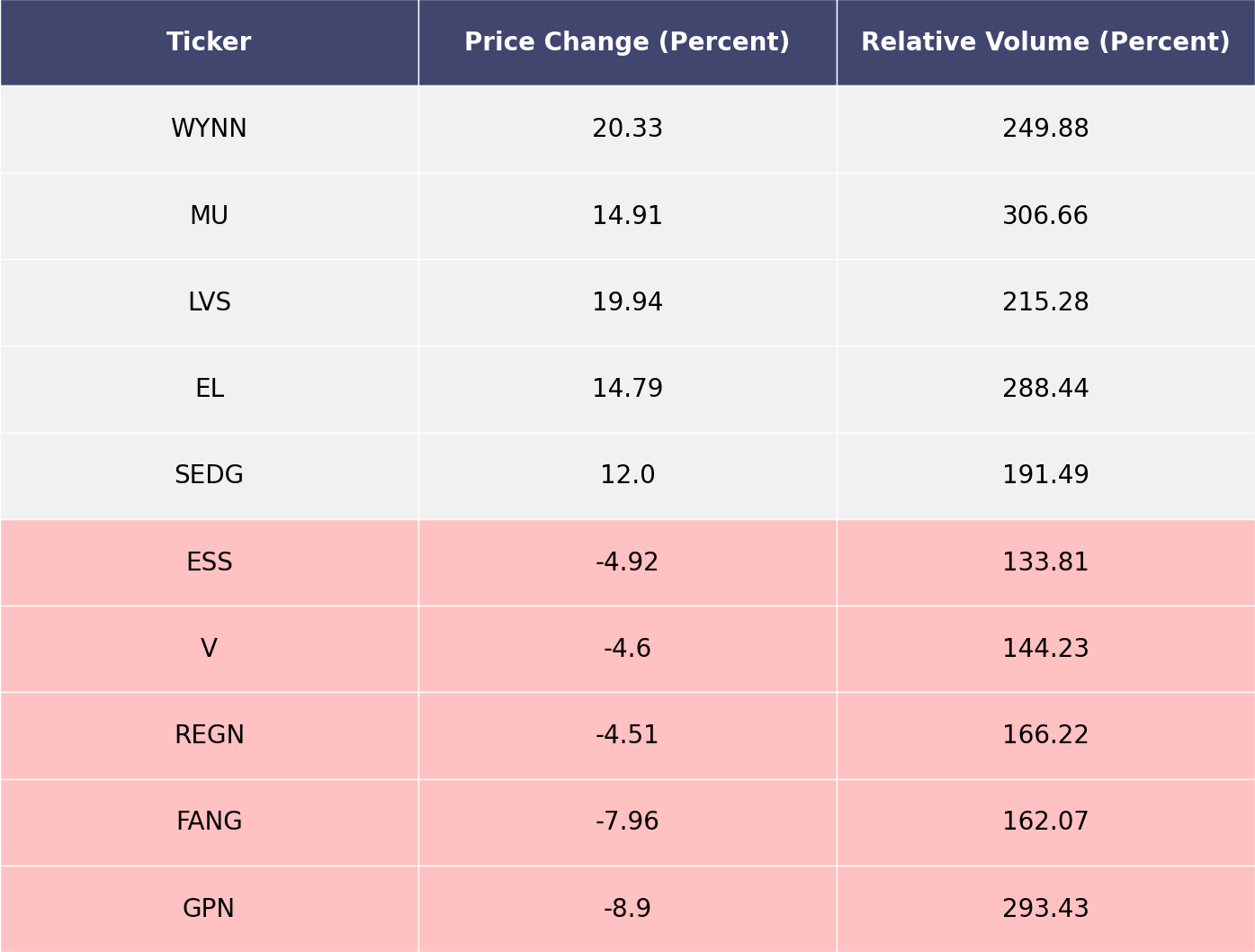

The biggest movers last week on price and volume (Large Cap S&P 500)

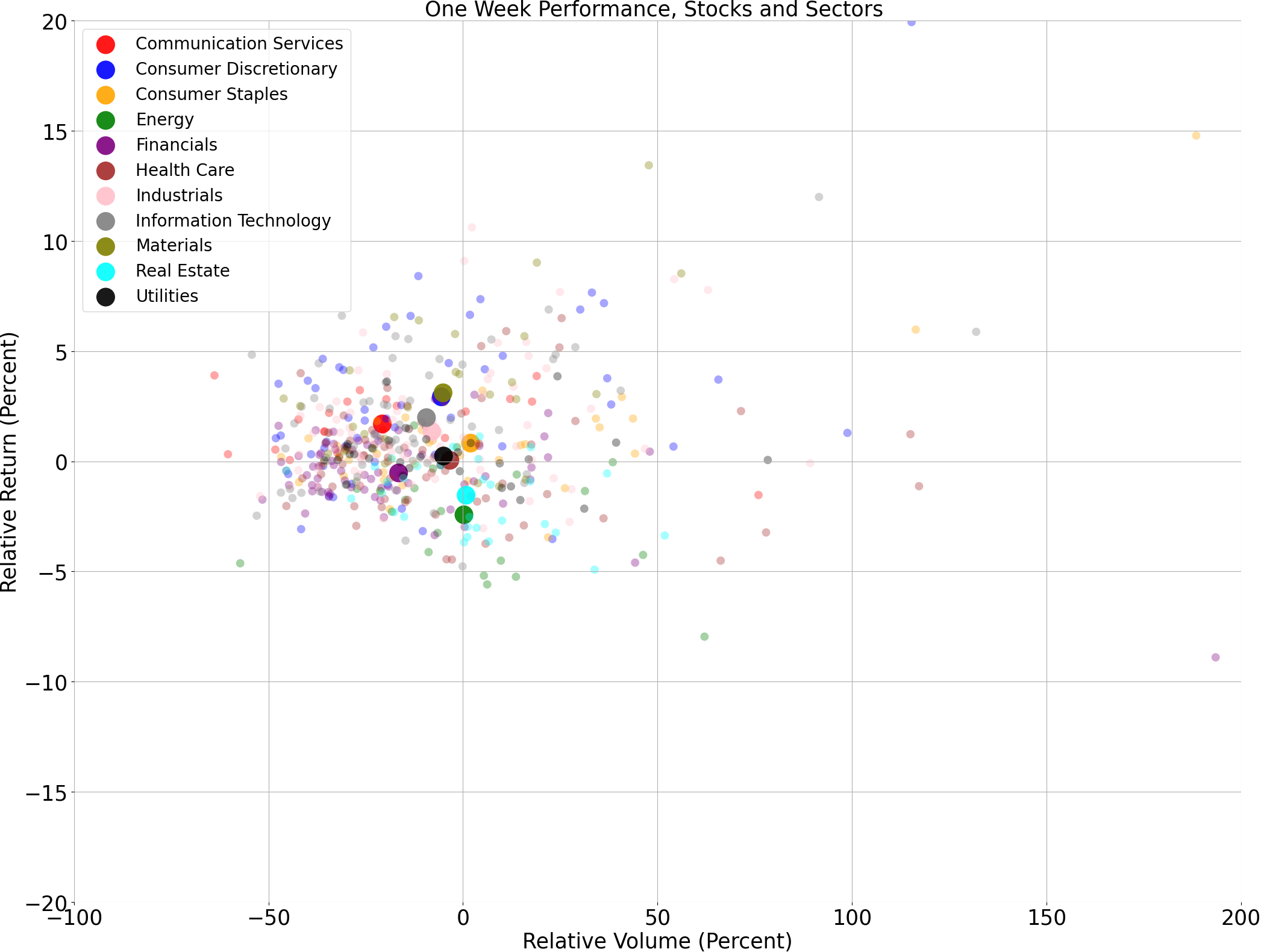

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

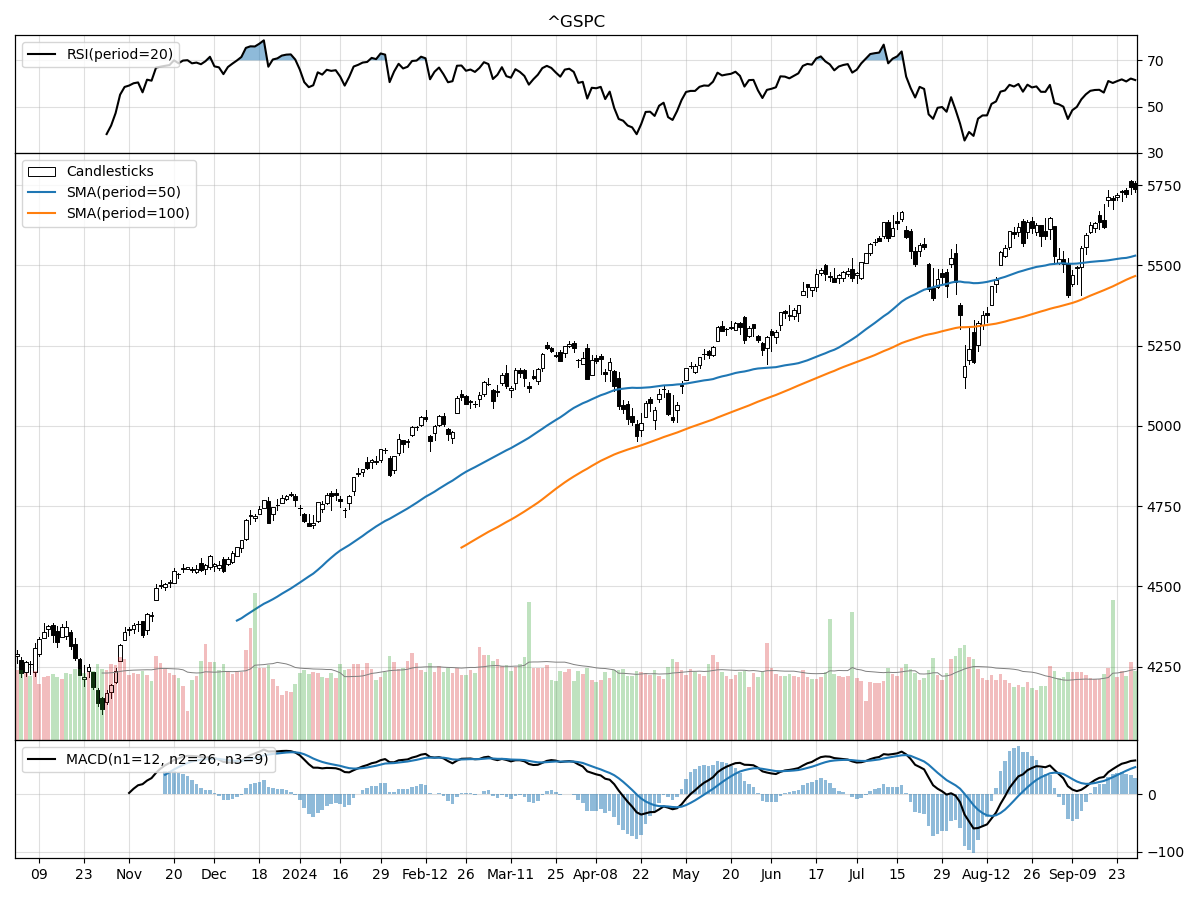

S&P500

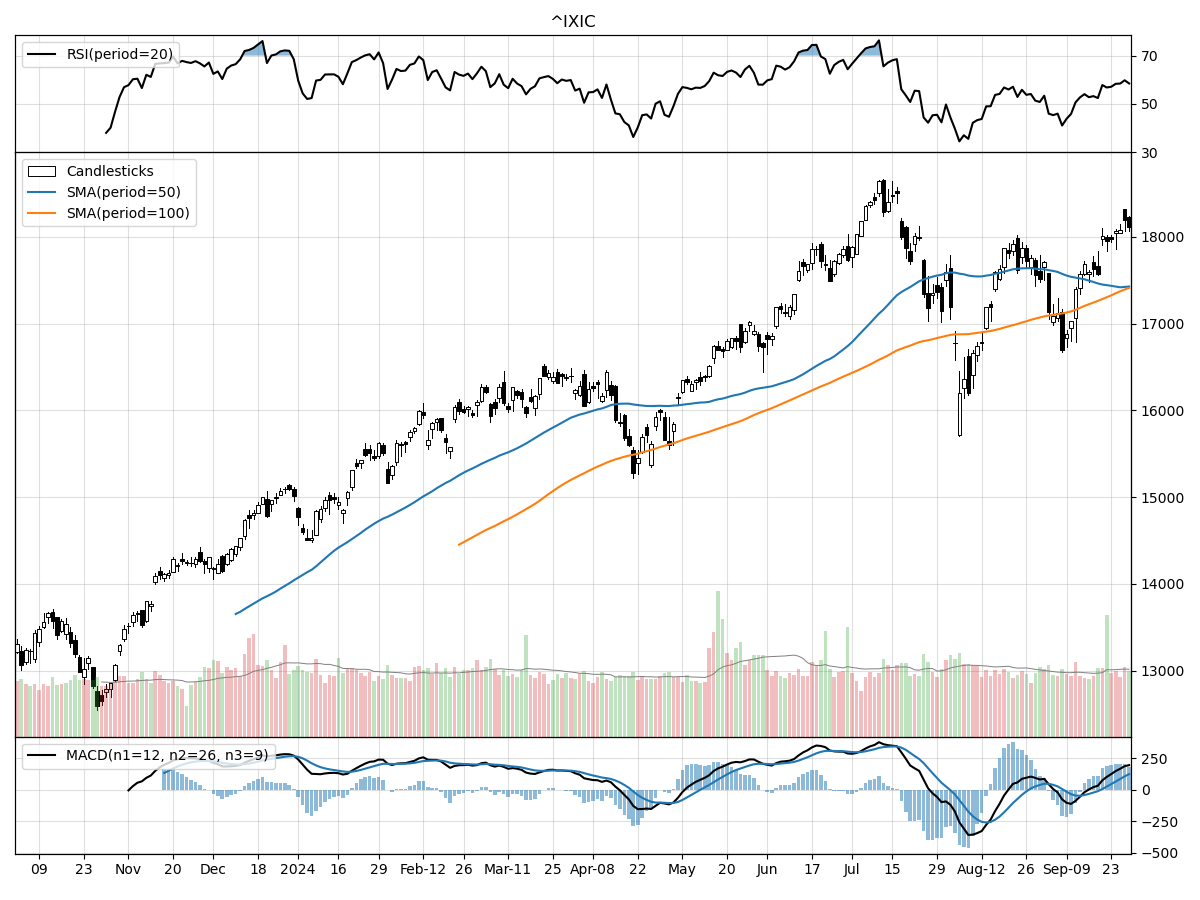

Nasdaq

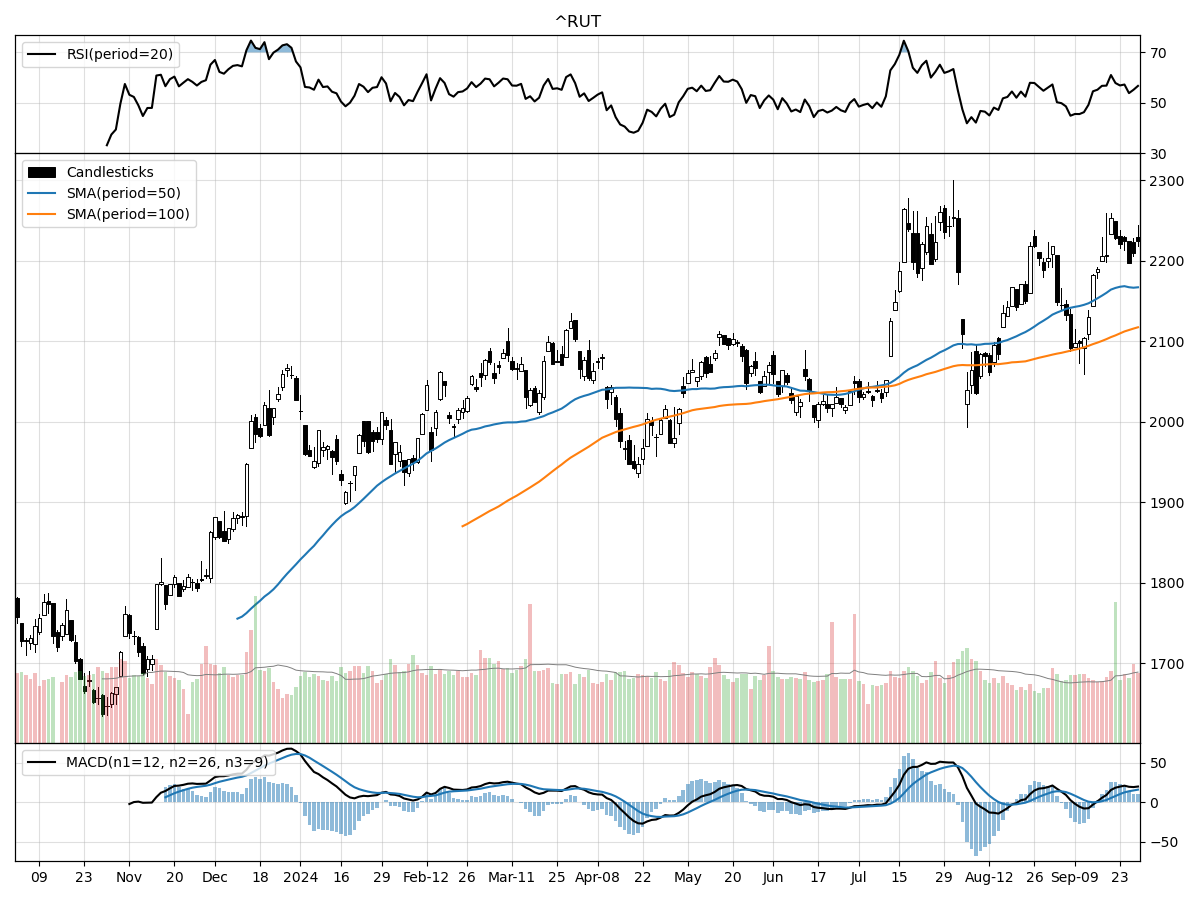

Russell 2000

When analyzing the technical performances of the S&P 500, Nasdaq, and Russell 2000 indices, a few key distinctions and similarities emerge. All three indices are trading near their 52-week highs, indicating a generally bullish market sentiment. The S&P 500 is currently at its 52-week high, while the Nasdaq is just 2% below its peak and the Russell 2000 is 1% below its high. This proximity to their annual highs suggests strong market momentum across the board. However, the Russell 2000 has shown a slightly higher volatility with a notable 9.8% rise over the last three months, compared to the more stable performances of the S&P 500 and Nasdaq.

Examining the volume and money flow indicators, all three indices are experiencing higher-than-average trading volumes, indicative of increased market participation. Both the S&P 500 and Nasdaq are under accumulation according to money flow indicators, suggesting sustained buying interest. In contrast, the Russell 2000, despite being under moderate buying pressure, is under distribution, which might indicate some selling pressure or profit-taking activity. The Relative Strength Index (RSI) across all indices points to a modestly overbought condition, reinforcing the bullish sentiment but also hinting at potential short-term corrections. Additionally, the Moving Average Convergence Divergence (MACD) indicators are bullish for all three indices, with the Nasdaq showing the most robust MACD value at 125.3, compared to 47.42 for the S&P 500 and 15.93 for the Russell 2000.

In summary, while all three indices exhibit strong bullish characteristics, the Russell 2000 shows slightly higher volatility and mixed signals in money flow, suggesting a more cautious approach. The S&P 500 and Nasdaq appear more stable, with consistent buying pressure and accumulation, making them potentially safer bets for investors seeking steady growth.

Last week vs. history (Large Cap S&P 500)

Market Commentary

As we edge closer to the presidential election, markets have demonstrated remarkable resilience, with stocks continuing their upward trajectory. Over the past seven weeks, the market has notched an impressive six weekly gains, culminating in an 11% surge since early August. This bullish performance is not necessarily indicative of market indifference to the political uncertainties that loom large. Instead, it reflects a market more attuned to Federal Reserve policies, an area where recent clarity has provided a stabilizing influence.

Historically, election-driven volatility is a common phenomenon, but it tends to be short-lived. The VIX Index, a measure of market volatility, typically spikes in the weeks leading up to the election, only to subside shortly thereafter. This pattern has held true across multiple election cycles, offering a semblance of predictability in otherwise uncertain times. Investors should note, however, that past performance does not guarantee future results, but it does offer valuable insights into market behavior.

Post-election, the market's focus traditionally shifts from political headlines to fundamental economic conditions. This is a reassuring trend, as long-term market performance is more influenced by economic fundamentals than by the occupant of the Oval Office. Historical data supports this view, showing that stocks have delivered solid returns under administrations from both major parties. This underscores the importance of a long-term investment strategy that prioritizes economic indicators over political developments.

A look back at post-World War II presidential elections reveals a consistent pattern of market performance. One week after the election, markets have generally shown positive returns, a trend that extends to one month and even one year later. Over the course of a full presidential term, the S&P 500 has exhibited robust performance, further emphasizing the resilience of the market in the face of political changes. This historical perspective provides a compelling case for maintaining a steady investment course.

Craig Fehr, CFA, a principal and leader of investment strategy at Edward Jones, highlights that the market's recent gains are a testament to its focus on Federal Reserve policies rather than election uncertainties. Fehr's analysis suggests that as we move past election day, the market will likely return its focus to economic fundamentals. This shift is crucial for investors seeking to navigate the post-election landscape, as it reinforces the importance of a strategy grounded in economic realities.

Important economic releases this week, including the ISM manufacturing PMI and the September nonfarm payrolls report, will provide further insights into the health of the economy. These indicators are critical for assessing the underlying economic conditions that drive market performance. Investors should pay close attention to these reports, as they offer valuable data points for making informed investment decisions.

Fehr's expertise, featured in prominent financial publications such as The Wall Street Journal and Bloomberg News, lends credence to his analysis. His educational background, including a master's degree in finance from Harvard University, further underscores his authority in the field. Fehr's insights are particularly valuable in the current climate, offering a nuanced understanding of the interplay between market performance and economic fundamentals.

In conclusion, while election-driven volatility is inevitable, it is typically short-lived and followed by a return to focus on economic fundamentals. Historical data supports the view that markets perform well after elections, regardless of the political party in power. Investors are advised to maintain a long-term perspective and base their decisions on economic indicators rather than political developments. As we advance toward and beyond election day, staying informed and grounded in economic realities will be key to navigating the market landscape effectively.

This article is for informational purposes only and should not be interpreted as specific investment advice. Investors should consider their unique investment objectives and financial situation when making decisions. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice. Past performance does not guarantee future results, and diversification does not ensure a profit or protect against loss in declining markets.

Comments ()