The Monday Charge: September 23, 2024

The Federal Reserve last week executed a larger-than-expected interest rate cut, slashing the policy rate by 0.5% to a range of 4.75%-5.0%

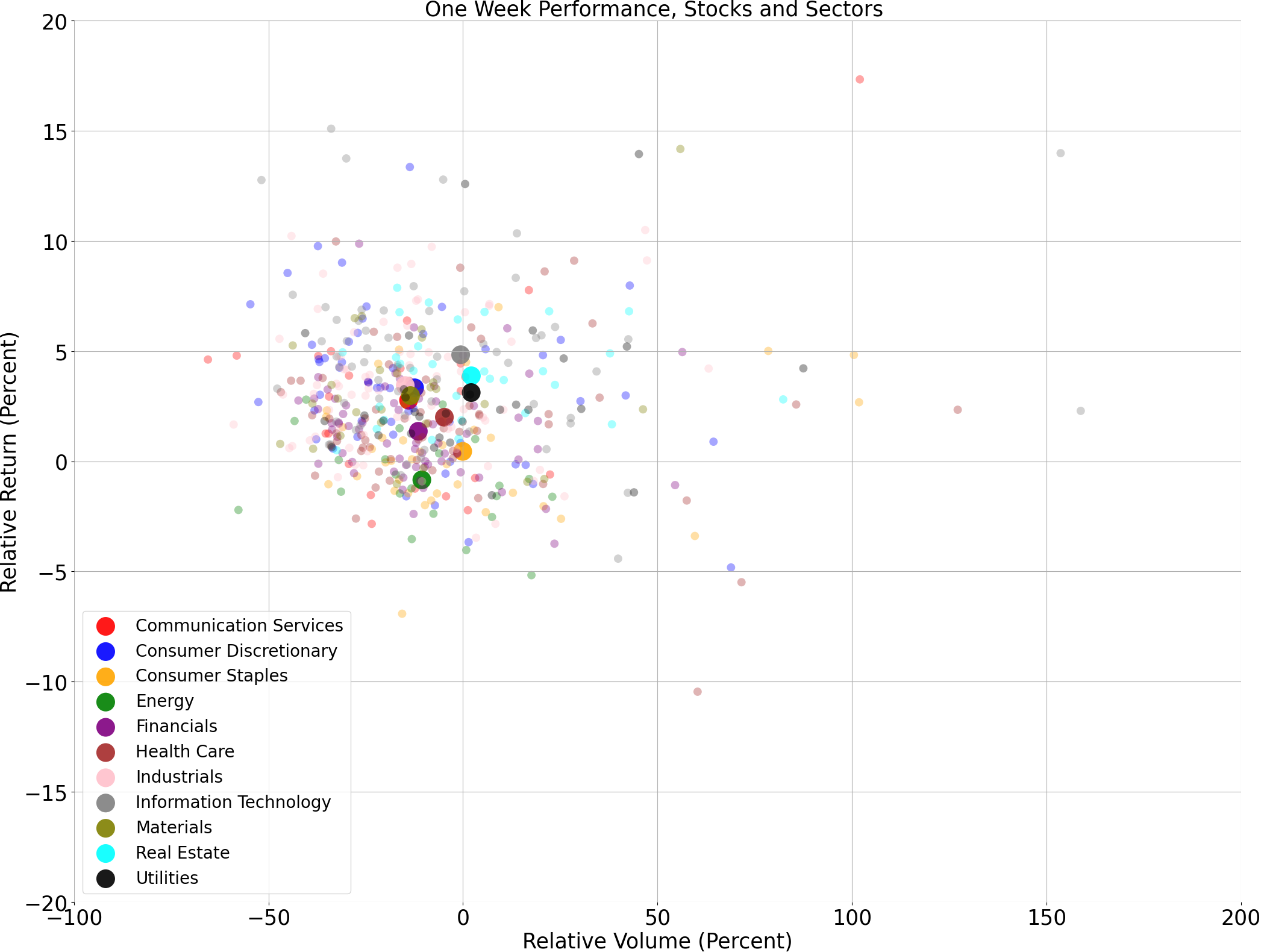

The biggest movers last week on price and volume (Large Cap S&P 500)

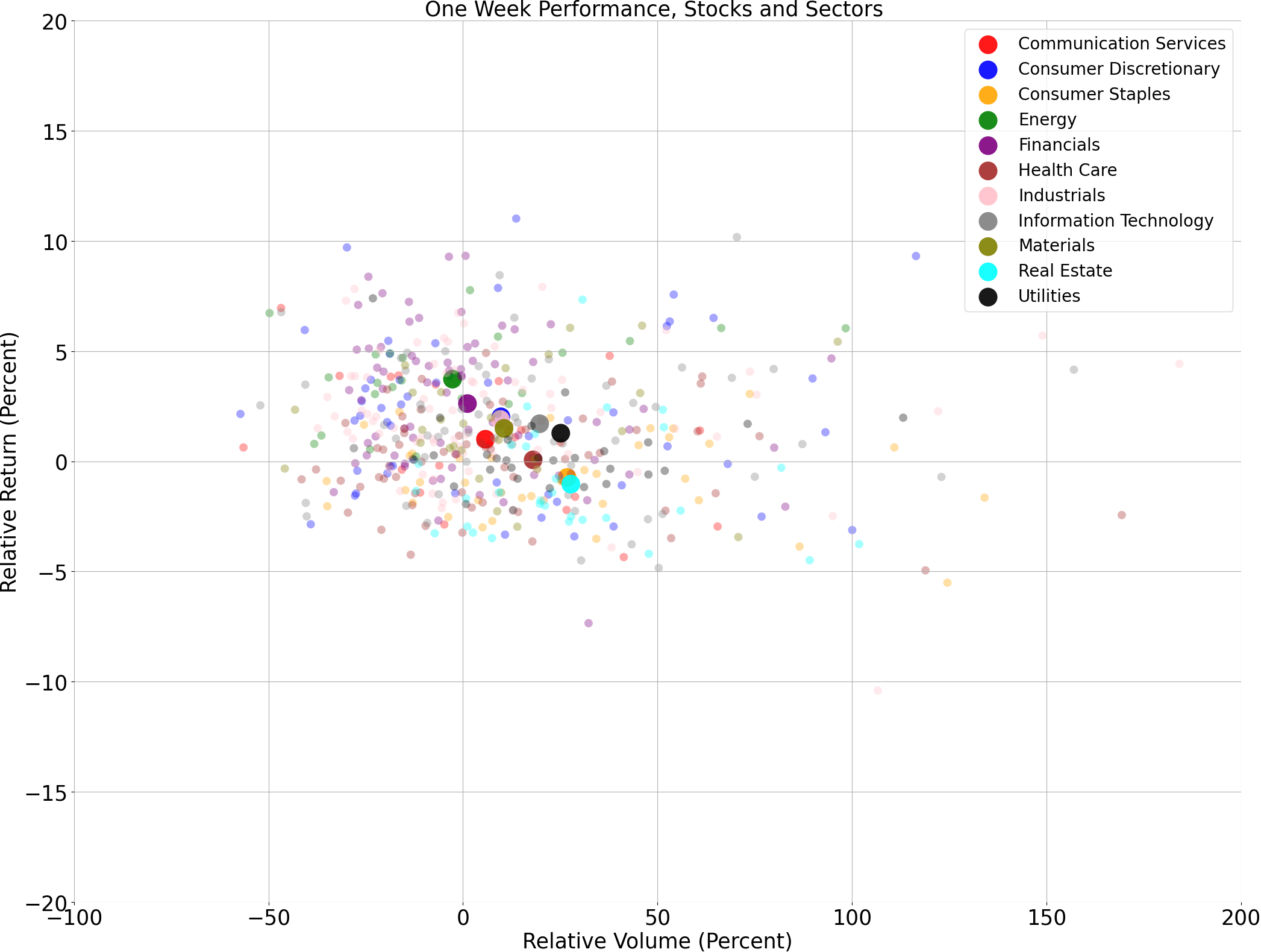

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

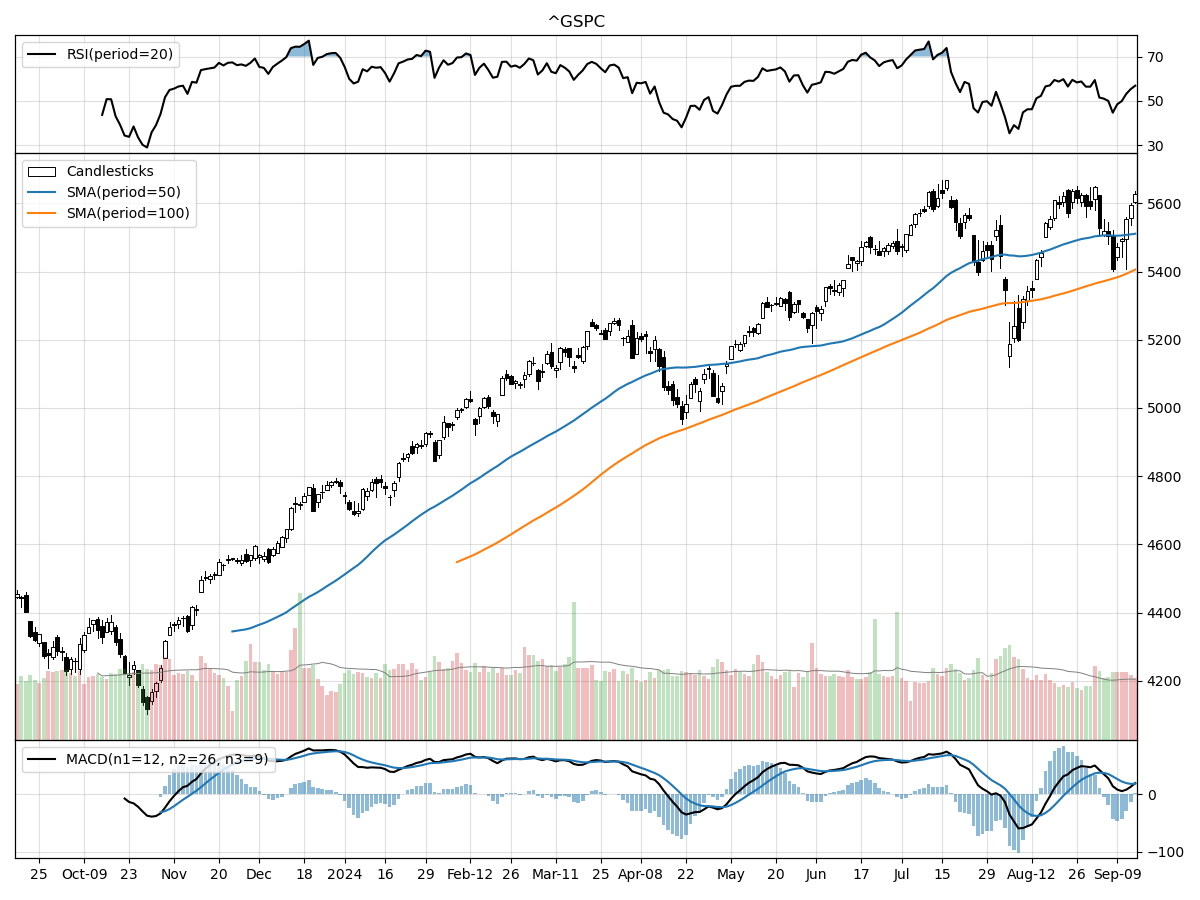

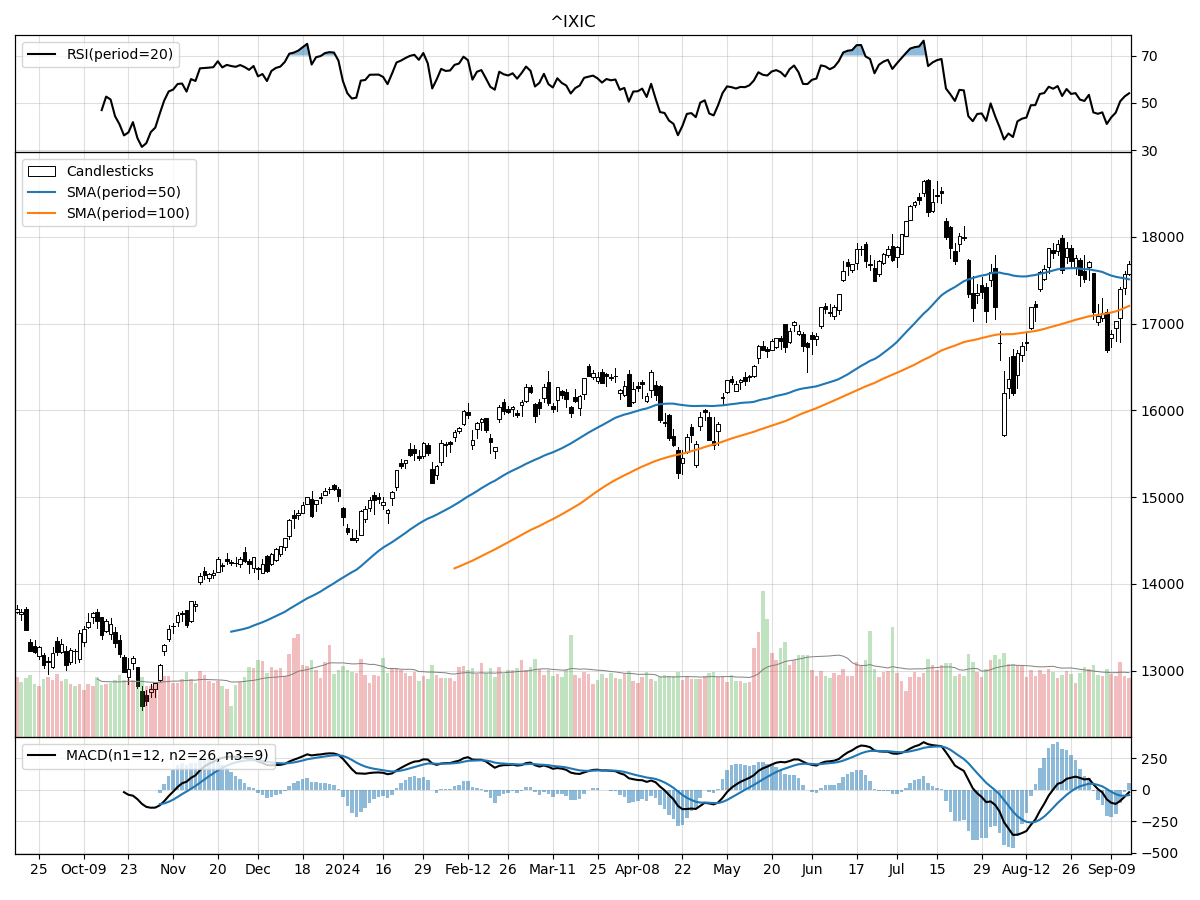

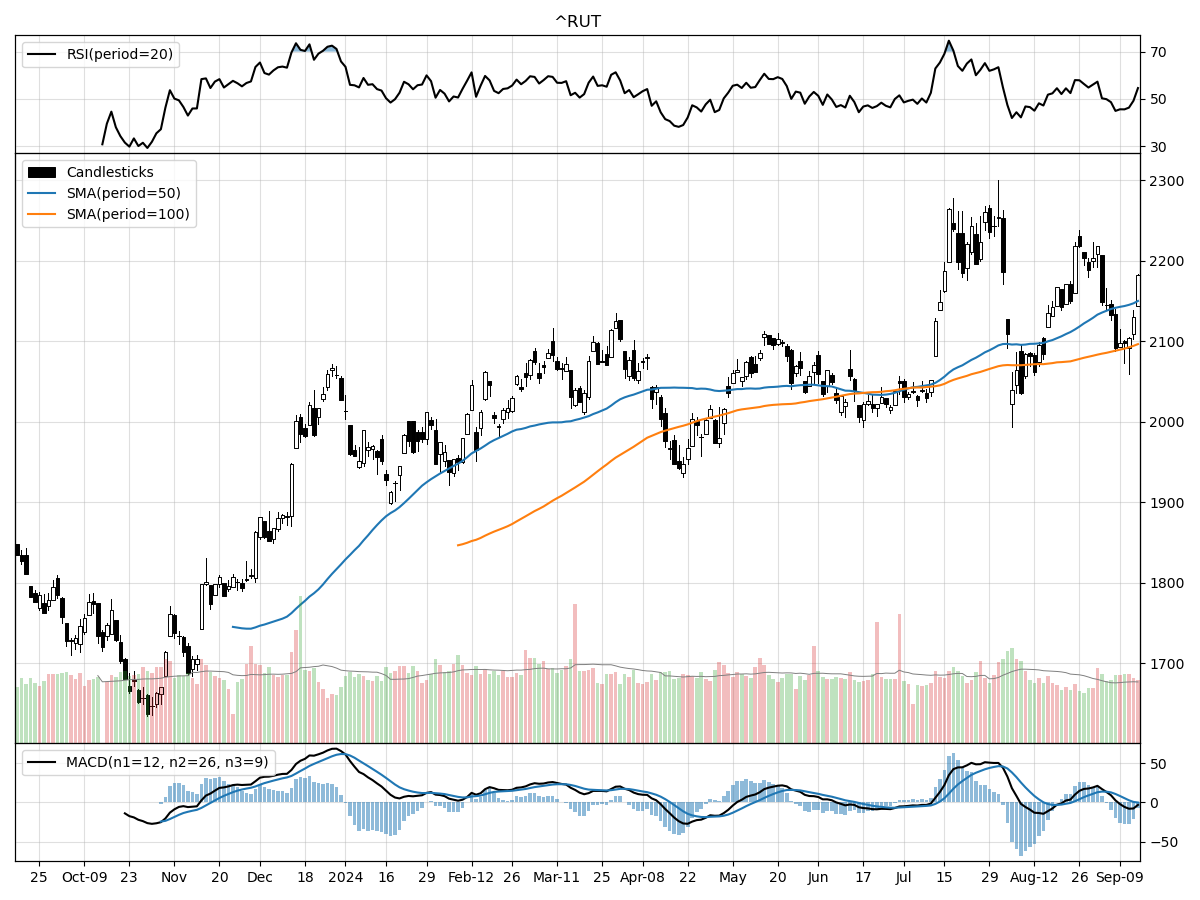

A technical analysis across indices

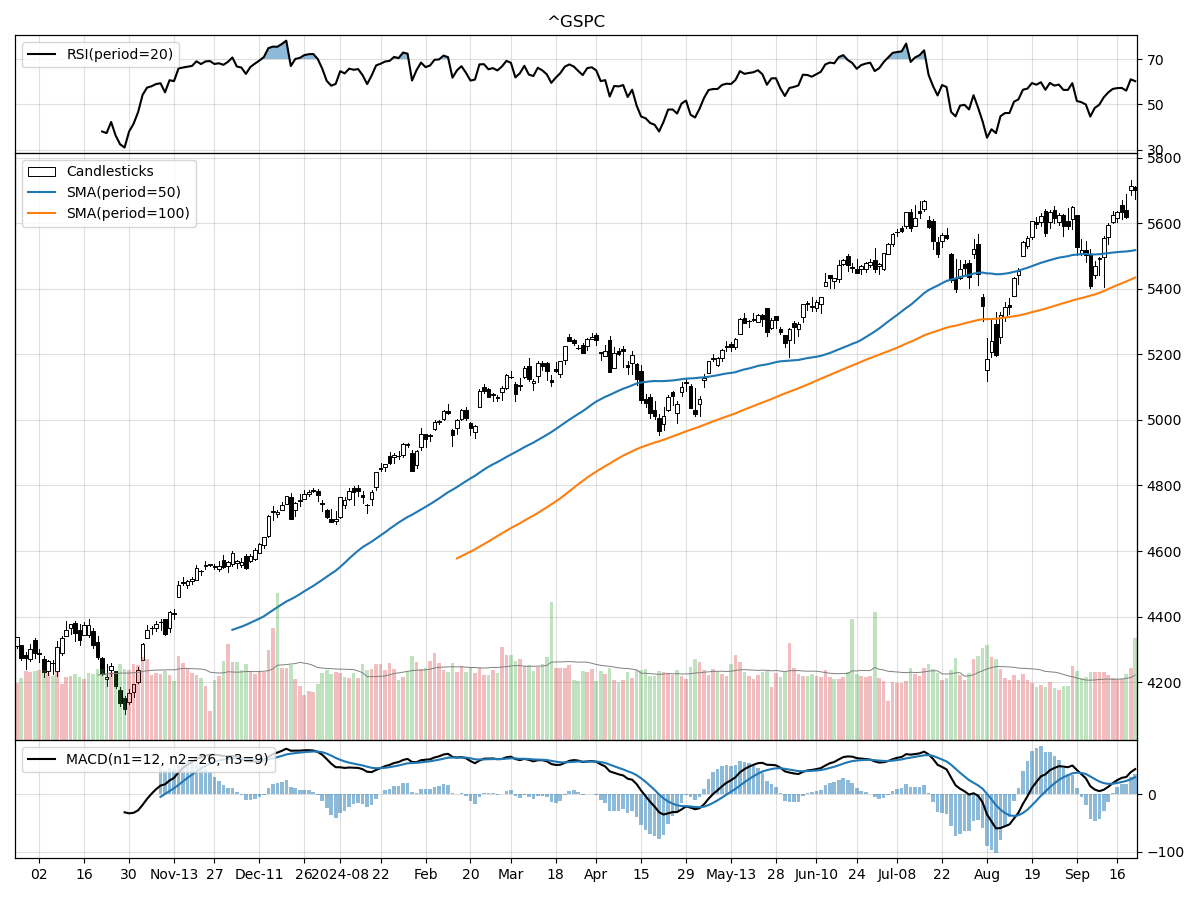

S&P500

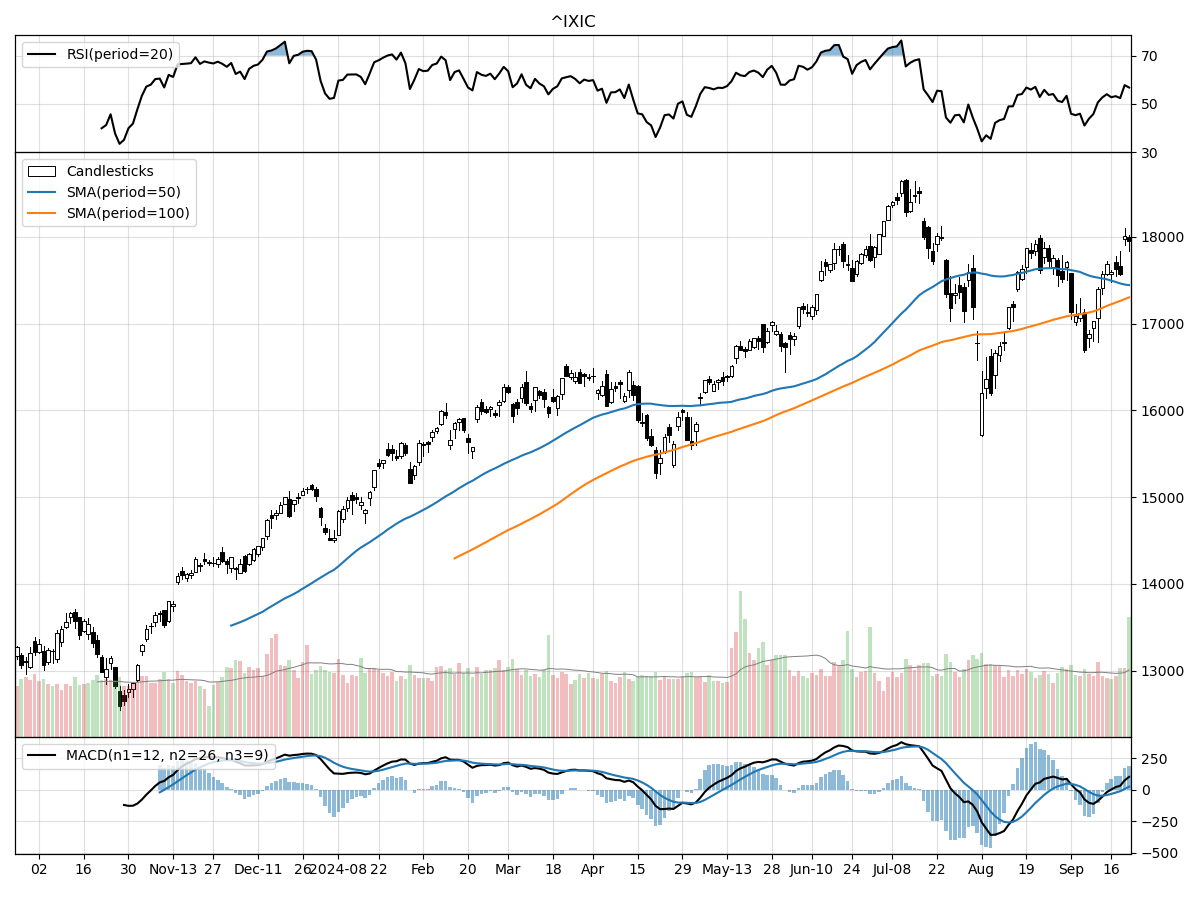

Nasdaq

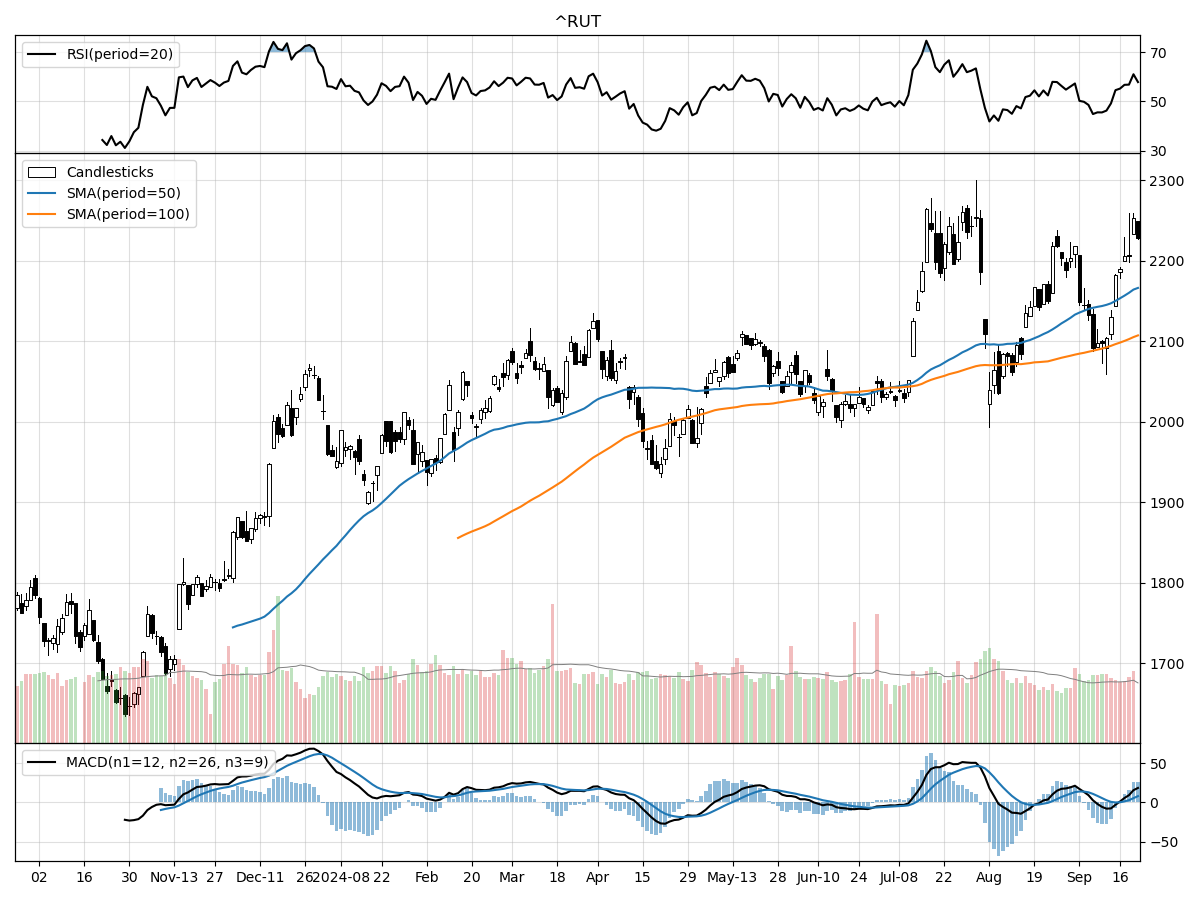

Russell 2000

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

S&P500

Nasdaq

Russell 2000

Upon examining the technical performances of the S&P 500, Nasdaq, and Russell 2000 indices, there are several key observations to note. The S&P 500 is currently trading at its 52-week high, marking a 36% increase from its 52-week low. This suggests a strong performance over the past year, although recent price movements have been relatively stable, indicating a potential consolidation phase. The S&P 500 is under moderate buying pressure, has a bullish MACD of 18.52, and is neither overbought nor oversold according to RSI metrics. This positions the index as a potentially stable investment with a bullish outlook.

In contrast, the Nasdaq index, while also performing robustly with a 40% increase from its 52-week low, is 5% below its 52-week high. This indicates some recent pullback or resistance at higher levels. The MACD for the Nasdaq is bearish at -41.1, suggesting potential downside momentum. However, like the S&P 500, the Nasdaq is under moderate buying pressure and is not in an overbought or oversold condition. This mixed technical picture suggests that the Nasdaq might be facing some headwinds, but the accumulation signals indicate underlying investor confidence.

The Russell 2000 index, representing small-cap stocks, has shown a notable 8.18% rise over the last three months, outpacing the more stable performances of the S&P 500 and Nasdaq in the same period. Despite this recent uptrend, the Russell 2000 is 3% below its 52-week high and has shown moderate selling pressure, which could be indicative of profit-taking or less investor conviction at current levels. The MACD is slightly bearish at -0.08, but the index is also in an accumulation phase and is neither overbought nor oversold. This suggests that while the Russell 2000 has potential for growth, investors should be cautious of near-term volatility.

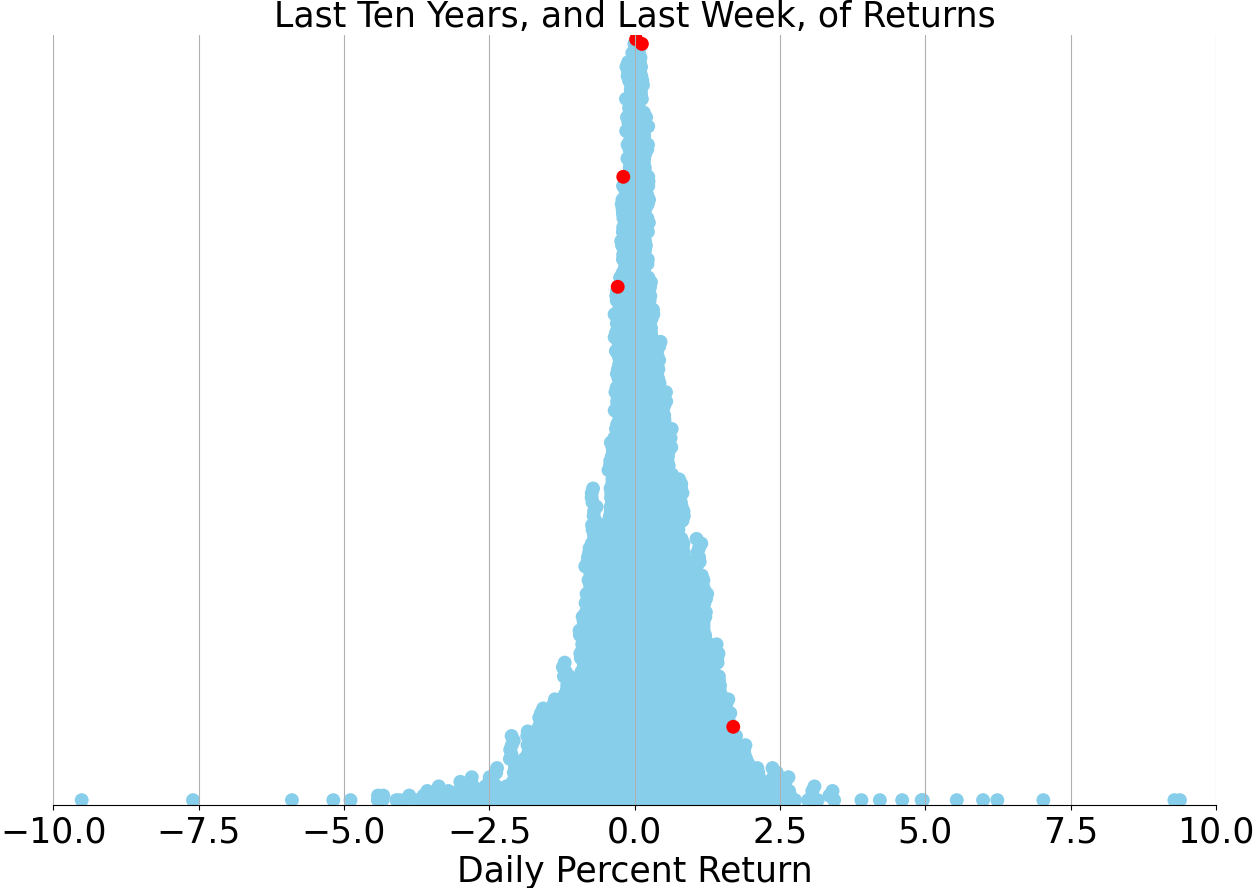

Last week vs. history (Large Cap S&P 500)

Market Commentary

In a move that has reverberated through the financial markets, the Federal Reserve last week executed a larger-than-expected interest rate cut, slashing the policy rate by 0.5% to a range of 4.75%-5.0%. This decision marks the first rate cut in four years and signals a significant shift in the Fed's monetary policy stance. Chair Jerome Powell had previously hinted at this change during his speech at Jackson Hole, but the magnitude of the cut took many by surprise. The rate reduction aims to address rising unemployment and ensure that inflation continues to move towards the Fed's 2% target, having already dropped from a peak of 9.1% in June 2022 to 2.5% in August.

The Fed's bold move is intended to preempt potential slowdowns in the labor market, reflecting a proactive approach rather than a reactionary one. Historically, such significant rate cuts have been reserved for crises like the 2020 pandemic, the 2008 financial meltdown, and the 2001 tech bubble burst. This time, however, the Fed is cutting rates as a precautionary measure to sustain economic expansion. Powell expressed optimism about the U.S. economy's fundamentals, and the updated Summary of Economic Projections supports this view, forecasting resilient growth and a slight uptick in unemployment to 4.4%.

The rate cut is not a one-off event but the start of what is expected to be a multi-year easing cycle. According to the Fed's updated "dot plot," additional cuts are anticipated, likely lowering the policy rate to around 2.9% by 2026. This gradual easing aims to bring the rate to a neutral point, balancing economic growth without stoking inflation. While the exact path will depend on incoming economic data, the general direction is clear: borrowing costs for consumers and businesses are set to decline, potentially spurring economic activity.

For investors, the Fed's rate cut is generally positive news, especially if the economy avoids a recession. Historical data shows that equities tend to perform well following the start of a rate-cutting cycle in non-recessionary periods. The S&P 500, which has already seen substantial gains this year, could continue its upward trajectory, although the extent of the rise may be tempered by already high valuations. The last comparable scenario occurred in 1995, when stocks surged 23% in the year following the initial rate cut.

The shift in Fed policy is also prompting a rotation in market leadership. Defensive and cyclical sectors like real estate, utilities, financials, and industrials have started to outperform, while tech and consumer discretionary stocks lag. This rotation suggests that investors are positioning themselves for a more balanced market environment. As long as a recession is avoided, cyclical and lower-valuation stocks could close the performance gap with mega-cap tech, offering new opportunities for portfolio diversification.

In the fixed-income market, the implications of the Fed's rate cut are equally significant. Although Treasury yields rose modestly following the announcement, they remain near year-to-date lows, with the likelihood of further declines ahead. Historically, investment-grade bonds have delivered positive returns in the 12 months following the start of a Fed rate-cutting cycle. Investors should consider extending the maturity profile of their fixed-income portfolios to mitigate reinvestment risk, as future rates are expected to be lower.

Overall, the Fed's decisive action has set the stage for a potentially soft landing for the U.S. economy. With consumer spending robust, jobless claims low, and household net worth at record highs, the economic backdrop appears favorable. Wage growth outpacing inflation further supports consumer purchasing power, while easing financial conditions and lending standards provide additional tailwinds. All these factors suggest that the economy is well-positioned to navigate the transition to a lower interest rate environment.

As the Fed continues its easing cycle, investors will need to stay vigilant, monitoring economic data and market trends closely. The opportunities for leadership rotations and the risks of holding too much cash are now more pronounced. With borrowing costs set to decline, areas of the market that have been under pressure from the Fed's previous tightening campaign could see renewed interest. High-quality dividend-paying stocks and mid-cap equities, in particular, offer compelling investment opportunities in this evolving landscape.

In conclusion, the Fed's supersized rate cut marks a pivotal moment in the current economic cycle. By taking proactive measures to support the labor market and ensure inflation remains on target, the Fed has increased the likelihood of a soft landing. For investors, this new phase of monetary policy presents both opportunities and challenges, necessitating a strategic approach to portfolio management. As always, diversification and a keen eye on market developments will be crucial in navigating the road ahead.

Stock study for Tuesday

Hess Corporation is a global exploration and production (E&P) company engaged in the exploration, development, production, transportation, purchase, and sale of crude oil, natural gas liquids, and natural gas. It operates in key regions including the United States, Guyana, the Malaysia/Thailand Joint Development Area (JDA), and Malaysia. One of its major projects is the Stabroek Block offshore Guyana, where it plans to deploy six FPSOs by 2027, targeting a production capacity of over 1.2 million gross barrels of oil per day. Hess is also pursuing the Whiptail project in Guyana, aiming for an initial production of 250,000 barrels of oil per day by 2027, and a Gas to Energy Project involving the construction of a 130-mile pipeline to an onshore power plant, expected to be completed by the end of 2024.

Comments ()