The Monday Charge: October 7, 2024

The September nonfarm payrolls report revealed a significant addition of 254,000 jobs, surpassing the anticipated 150,000.

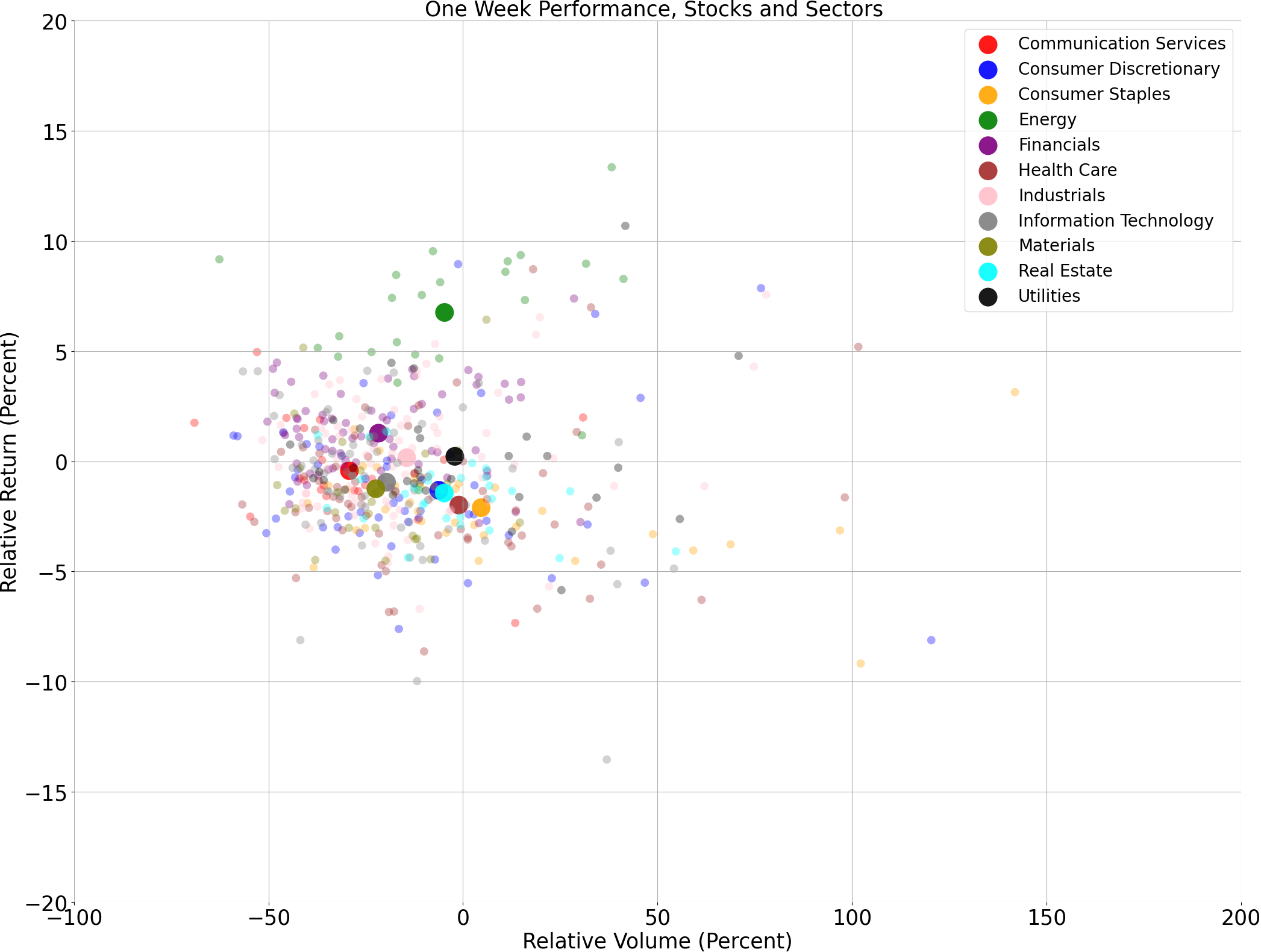

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

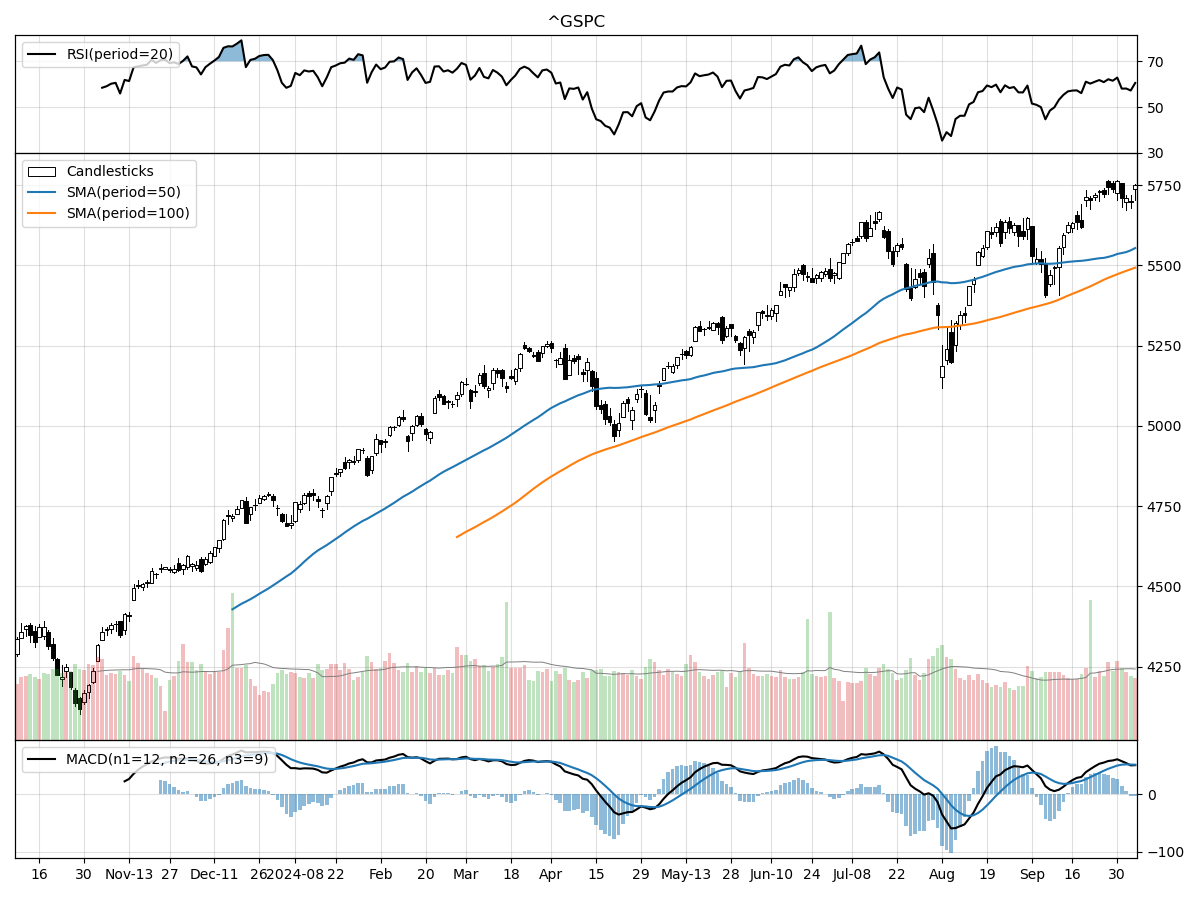

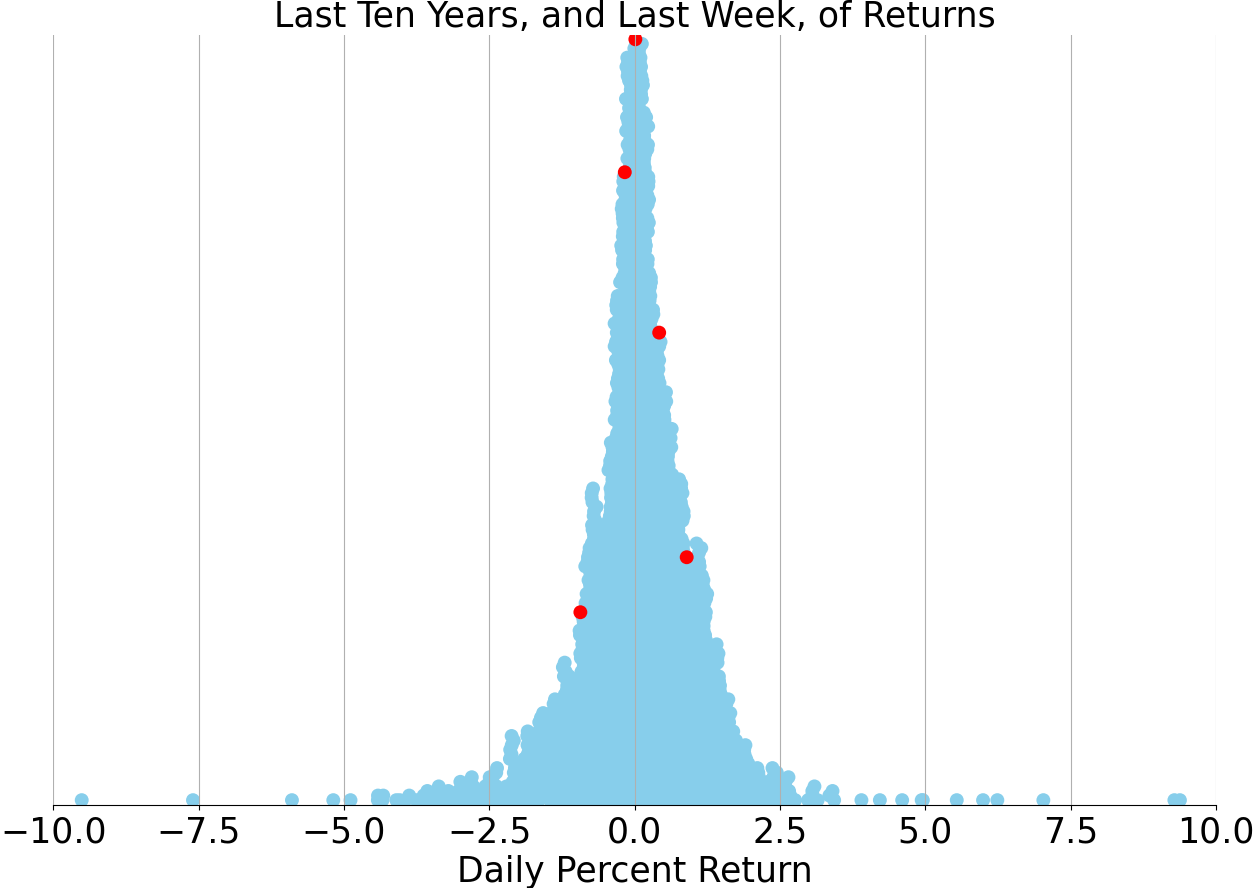

S&P500

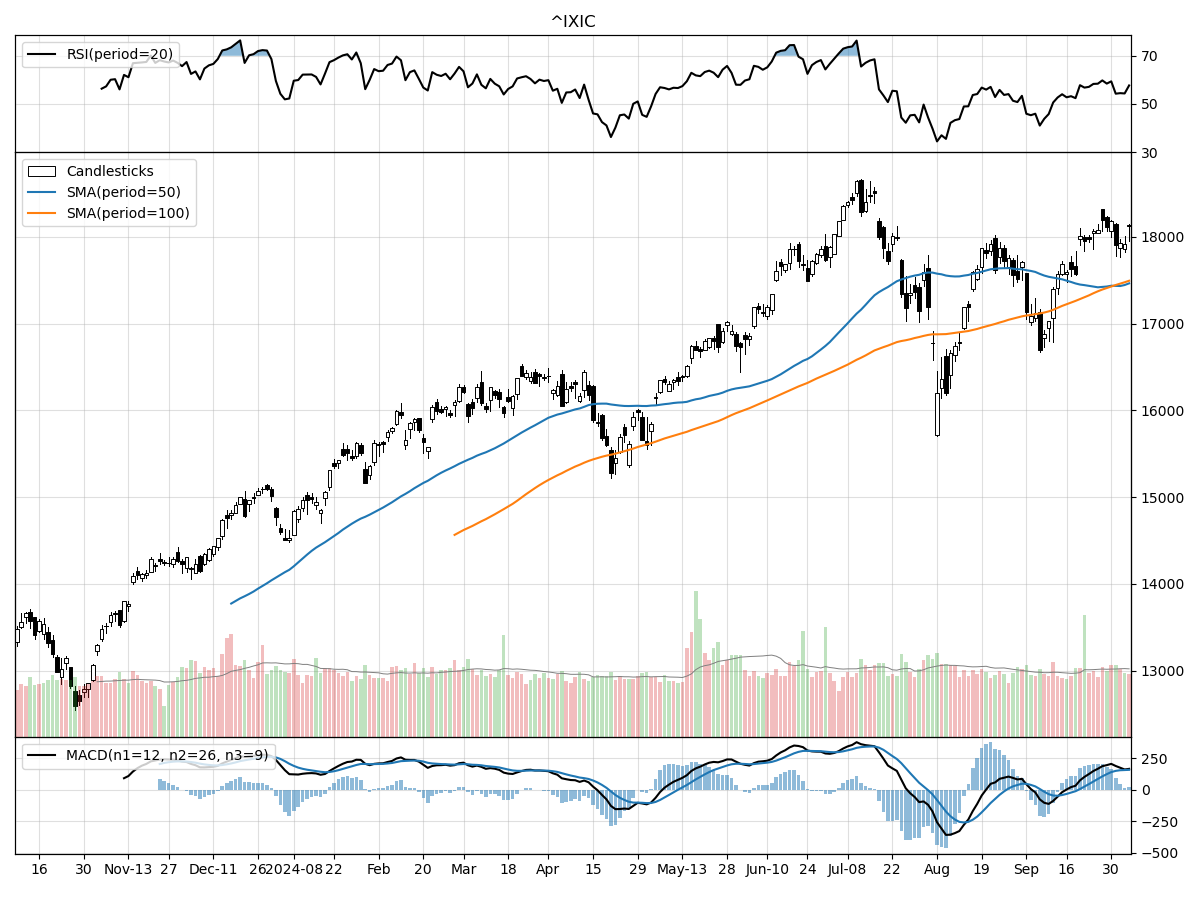

Nasdaq

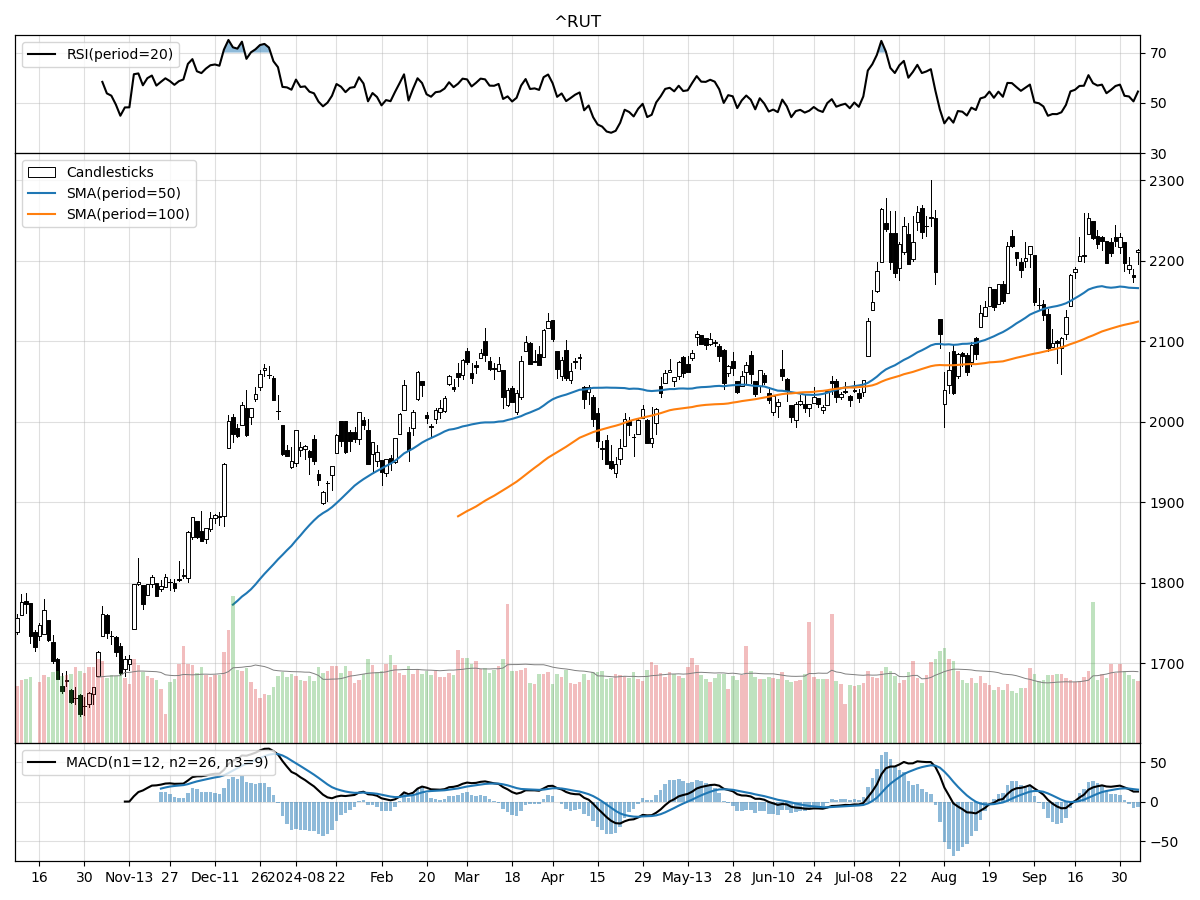

Russell 2000

When examining the technical performances of the S&P 500, Nasdaq, and Russell 2000 indices, several key differences and similarities emerge. The S&P 500 is currently trading at its 52-week high, indicating a robust upward trajectory over the past year. The recent increase of 5.12% over the past month reflects a resurgence in investor confidence, although the RSI suggests that the index is modestly overbought, hinting at a potential risk of a pullback. Volume levels slightly above the long-term average signal healthy market participation, and the bullish MACD, coupled with the stock being under moderate buying pressure, suggests continued positive momentum in the short term.

In contrast, the Nasdaq, although not at its 52-week high, is still only 2% below its peak, demonstrating a strong performance with a 7.42% monthly gain. This index seems to be in a more balanced state, as indicated by its RSI not flagging it as overbought or oversold. The higher-than-average trading volumes and the bullish MACD further underscore the positive sentiment, with the Nasdaq under moderate buying pressure and accumulation, signaling a potential for further gains as investors continue to inject capital.

The Russell 2000, on the other hand, presents a slightly different picture. While it has also enjoyed a respectable 5.48% increase over the past month, it is under moderate selling pressure and distribution according to money flow indicators. This suggests that despite the bullish MACD, there is a degree of investor uncertainty or profit-taking occurring within the small-cap space. The index is also 2% below its 52-week high, similar to the Nasdaq, reflecting a stable, yet cautiously optimistic outlook. The differing pressures observed in the Russell 2000 highlight the nuanced behavior of small-cap stocks, which may be more sensitive to broader economic conditions and investor sentiment shifts.

Last week vs. history (Large Cap S&P 500)

Market Commentary

In a week marked by unexpected economic developments, the U.S. labor market delivered a robust performance that exceeded analysts' expectations, providing a welcome shift in tone for financial markets. The September nonfarm payrolls report revealed a significant addition of 254,000 jobs, surpassing the anticipated 150,000. This strong showing was accompanied by a slight decline in the unemployment rate, which edged down from 4.2% to 4.1%. Moreover, revisions to the previous month's data indicated an upward adjustment, further bolstering confidence in the labor market's resilience. This data suggests a normalization in labor dynamics, as more individuals enter the workforce and job openings gradually decline.

The implications of this labor market strength extend to the Federal Reserve's monetary policy, particularly concerning interest rate cuts. Following the release of the jobs report, markets reacted swiftly, with Treasury bond yields rising and futures markets adjusting their expectations for rate cuts. The consensus now leans towards two additional 0.25% rate cuts before year-end, rather than the more aggressive 0.5% reductions previously anticipated. This measured approach appears prudent, especially given the persistent wage growth of 4.0% year-over-year, which keeps inflationary pressures in focus.

In parallel, the resolution of a significant labor dispute on the East Coast further contributed to market optimism. The International Longshoremen's Association, representing workers at major ports, reached a tentative agreement after a brief strike. The deal includes a substantial wage increase of 62% over six years, averting prolonged disruptions that could have exacerbated inflationary pressures. While the wage hikes may contribute to marginal inflation, the swift resolution mitigates the risk of broader economic impacts.

Geopolitical tensions added another layer of complexity to the week's market dynamics, as hostilities flared in the Middle East. An Iranian missile strike on Israel prompted concerns over potential retaliatory measures, leading to a spike in oil and commodity prices. Safe-haven assets, such as gold and Treasury bonds, initially rallied, reflecting heightened market anxiety. However, as the week progressed, these moves largely reversed, with oil prices remaining the notable exception, underscoring the persistent risk of supply disruptions.

The looming U.S. presidential election also remains a focal point for investors, with the potential to inject volatility into markets. Historical patterns suggest that stock markets often experience heightened uncertainty in the weeks leading up to Election Day, only to recover once the electoral dust has settled. Despite the absence of significant election-related news this week, the tight races and potential for narrow margins of victory in key states keep political risks at the forefront of market considerations.

As the fourth quarter unfolds, equity markets face a series of challenges, including labor market uncertainties, geopolitical tensions, and the upcoming election. Nonetheless, the strong jobs report and resolution of the port strike have provided a degree of reassurance. Investors are advised to remain vigilant, leveraging any market pullbacks as opportunities to diversify and rebalance portfolios with quality investments.

Looking ahead, the fundamentals of the current bull market appear intact. The Federal Reserve's path towards easing interest rates, coupled with moderating inflation, supports a favorable economic backdrop. Earnings growth remains robust, with double-digit gains projected for this year and potentially next, further underpinning both equity and bond markets.

In conclusion, while uncertainties persist, the U.S. economy seems poised for a "soft landing," avoiding recessionary pressures. Investors should remain attuned to evolving market conditions, particularly as key economic indicators and geopolitical developments continue to unfold. With careful navigation, the opportunities for growth and stability in financial markets remain promising.

Comments ()