The Monday Charge: March 4, 2024

As we bid farewell to February, the financial markets have provided investors with a reason to smile. The S&P 500 surged by 5% last month, marking one of its best February performances since 1980. The upswing wasn't isolated to the United States; global equities also soared...

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

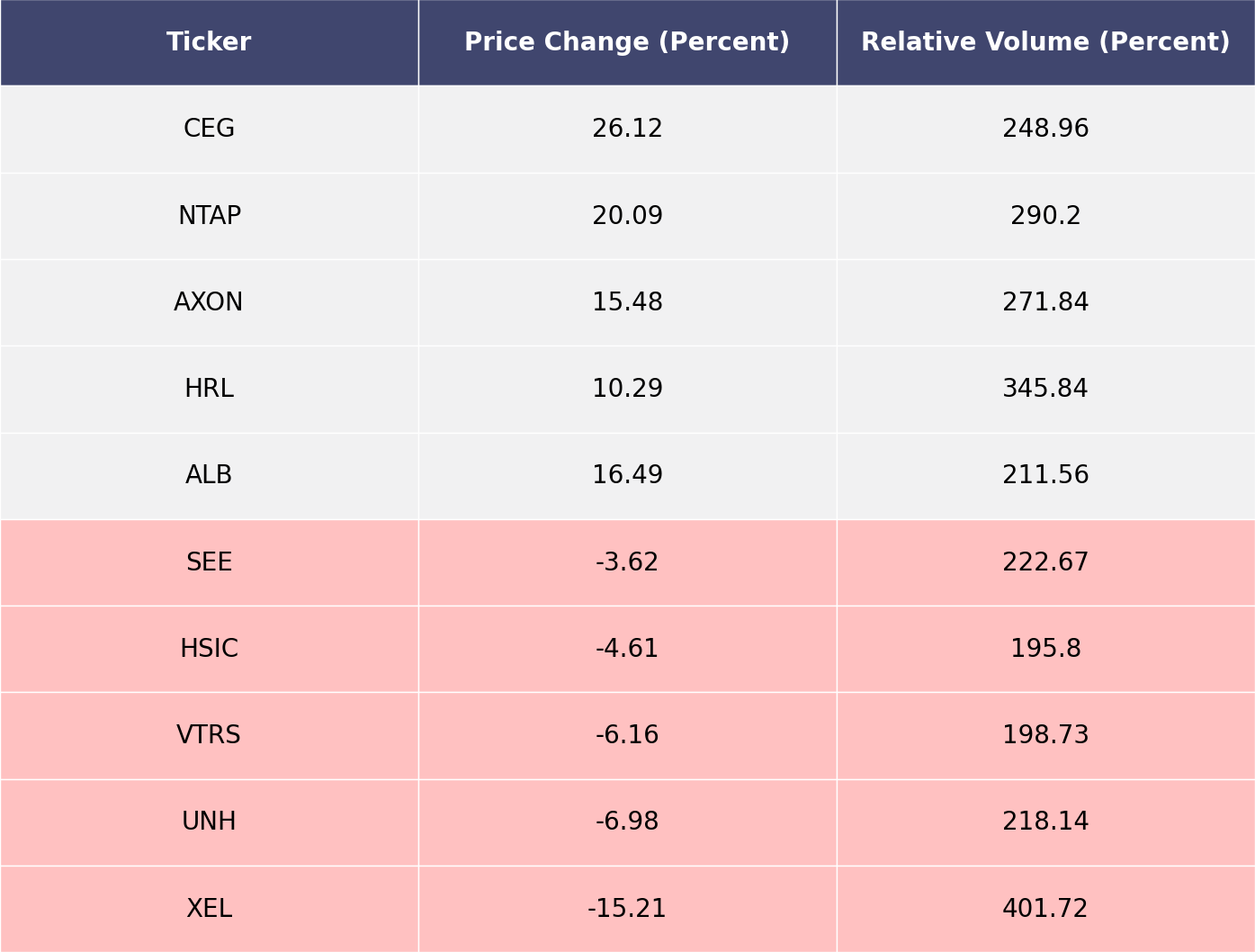

The biggest movers last week on price and volume (Large Cap S&P 500)

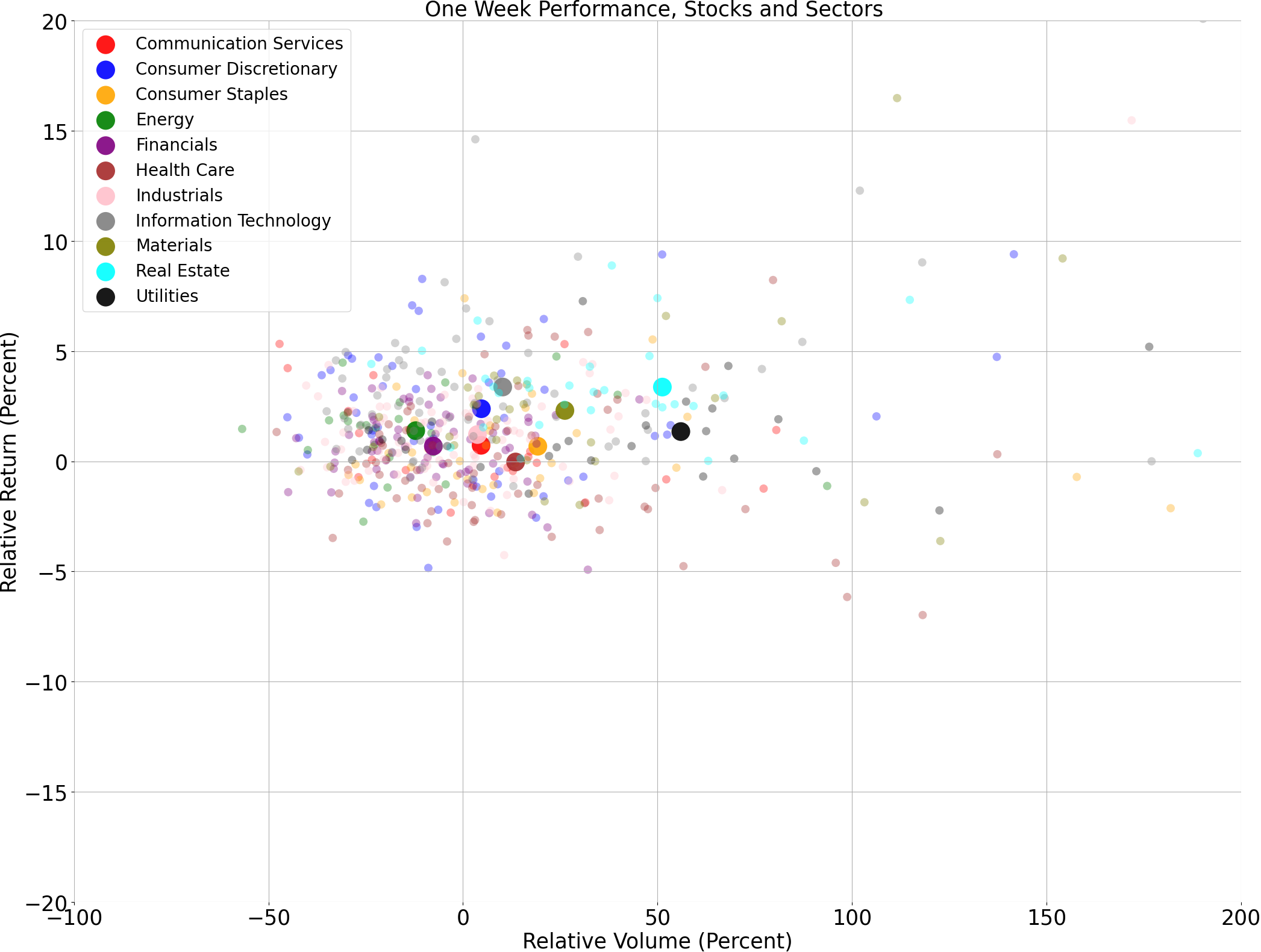

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

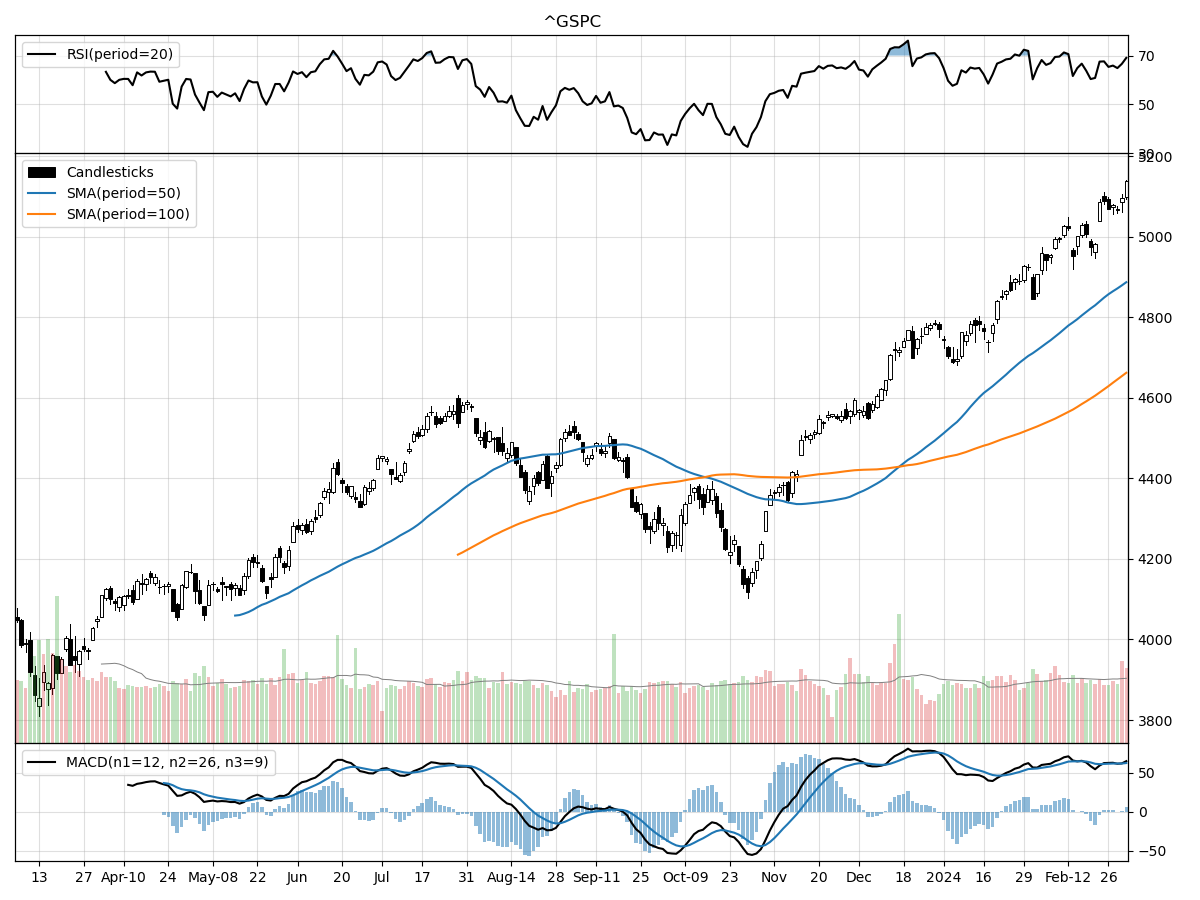

S&P500

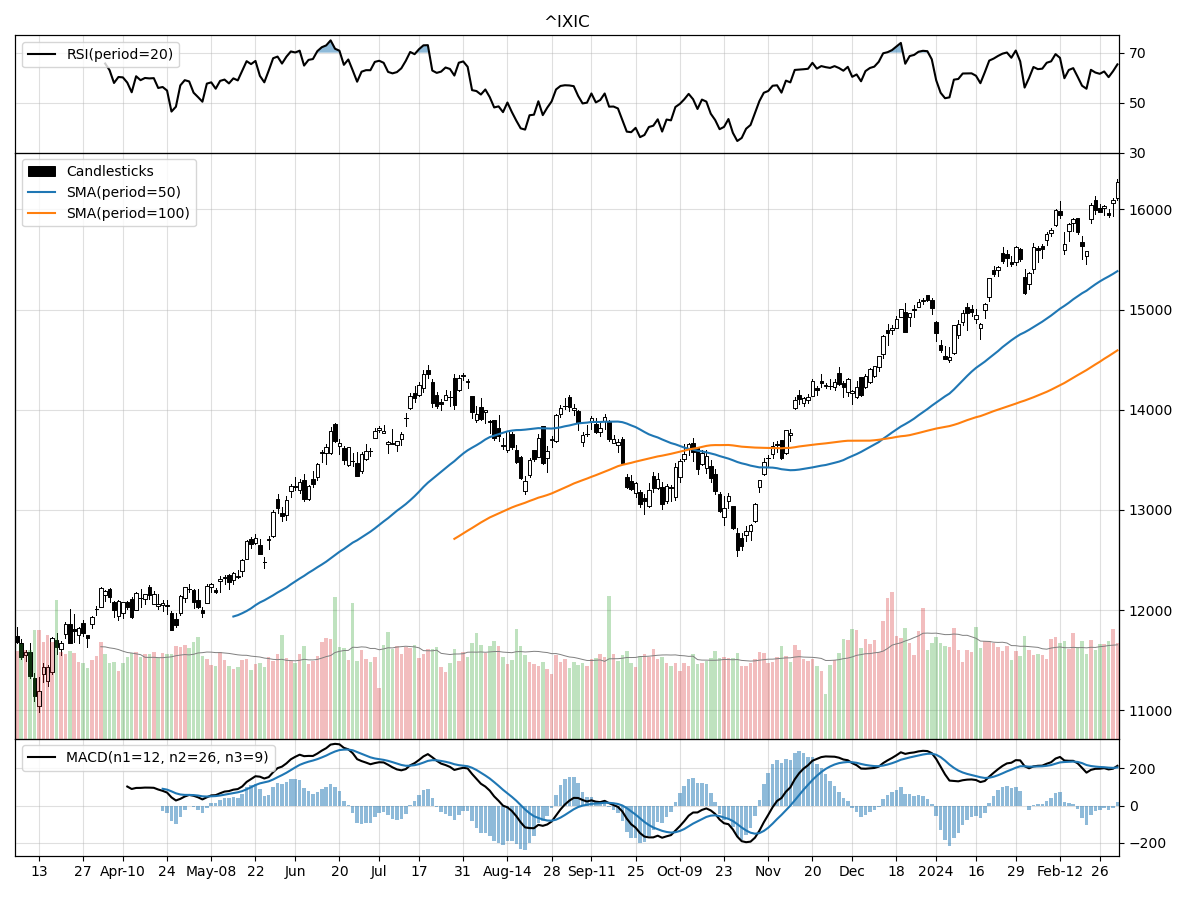

Nasdaq

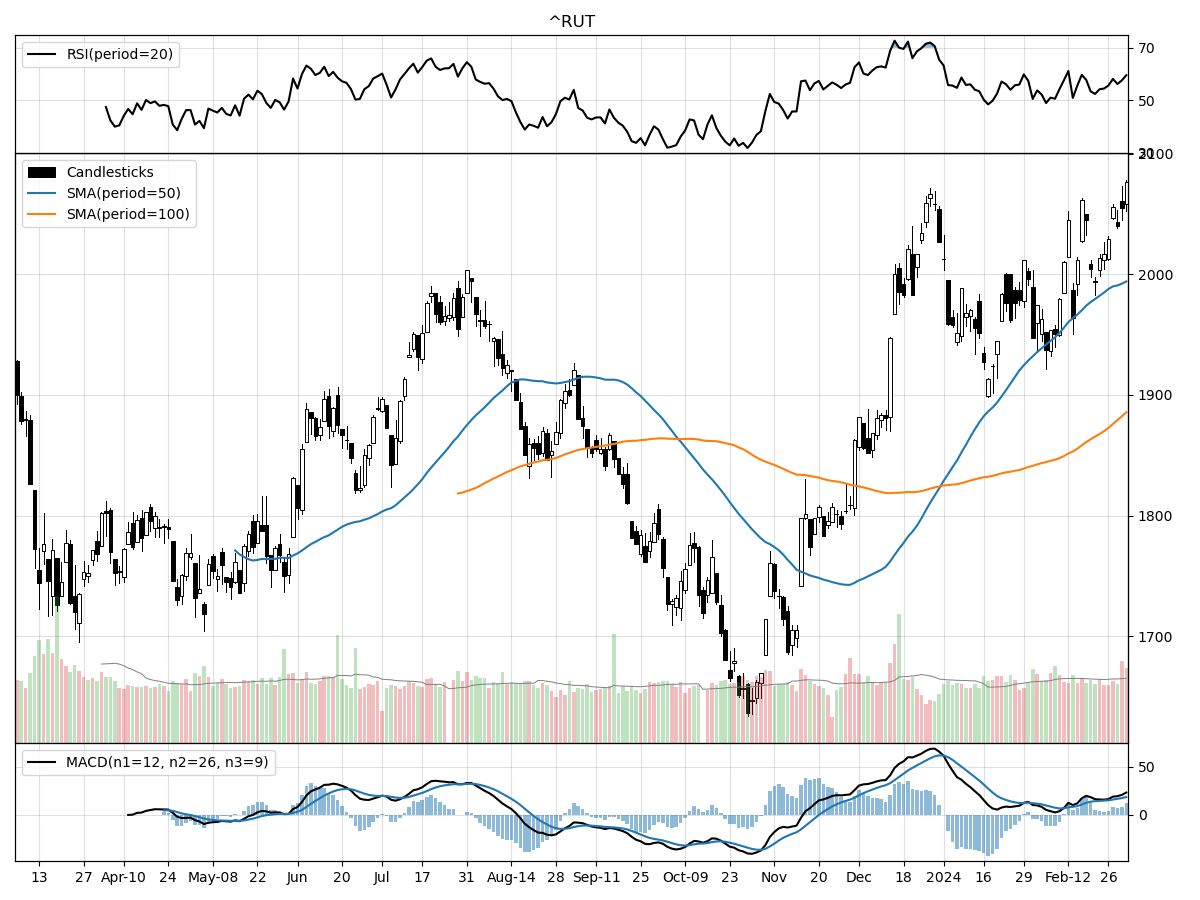

Russell 2000

The S&P 500, Nasdaq, and Russell 2000 Small Cap indices exhibit positive momentum with each index currently trading at or near their respective 52-week highs, which suggests investor confidence across different segments of the market. All three indices show a pattern of accumulation, as indicated by money flow indicators, suggesting that investors are buying in rather than selling off their positions. This is further corroborated by the bullish MACD (Moving Average Convergence Divergence) readings for each index, with the Nasdaq showing the most significant bullish value at 204.5, followed by the S&P 500 and the Russell 2000, with values of 62.20 and 18.39 respectively.

In terms of relative strength, the RSI (Relative Strength Index) suggests that the S&P 500 and Nasdaq are modestly to significantly overbought, which may indicate a potential for a near-term pullback as traders might take profits. Conversely, the Russell 2000's RSI points to modest overbought conditions, which might be seen as slightly less risky in the immediate term. Furthermore, the percentage increase over the last three months shows that the Nasdaq leads with a 14.37% gain, closely followed by the S&P 500 at 12.48%, while the Russell 2000 shows a smaller yet substantial increase of 11.87%.

Volume analysis shows that recent daily trading volumes for all three indices are above their longer-term averages, with the Nasdaq observing the most significant increase in daily volume. This may indicate heightened investor interest or increased liquidity in the market, which can be a positive sign for sustaining the current uptrend. The Russell 2000's performance, while trailing in terms of percentage gain over the last three months, does show a significant price increase of 5.79% in the last month, which might indicate a catch-up rally or a rotation into small-cap stocks. Overall, while each index has its unique characteristics and risk profiles, the technical analysis underlines a strong market with bullish undertones across the board, albeit with potential overbought risks in the short term.

Last week vs. history (Large Cap S&P 500)

Market Commentary

Markets Climb Amid Optimism and Earnings Strength: A February Recap

As we bid farewell to February, the financial markets have provided investors with a reason to smile. The S&P 500 surged by 5% last month, marking one of its best February performances since 1980. The upswing wasn't isolated to the United States; global equities also soared, with the German DAX, the French CAC, and Japan's Nikkei reaching zeniths not seen in decades. This rally in equities came despite a backdrop of rising bond yields, indicating a robust appetite for risk among investors.

The resilience of the stock market can be attributed to several key factors. Corporate earnings for the fourth quarter came in strong, with the S&P 500 companies reporting a commendable 7.5% earnings growth. This bullish sentiment was further fueled by a wave of excitement around AI technology, following optimistic projections from industry leader NVIDIA. Additionally, the U.S. economy's growth, pegged at 3.2% for the last quarter, has continued to outpace expectations, driven by solid consumer spending and a rebound in productivity.

However, not all segments of the market enjoyed the same success. Bonds faced pressure for the second consecutive month as yields ticked upwards, a reaction to higher-than-anticipated consumer and producer prices. This has led to a recalibration of expectations for Federal Reserve rate cuts, with market predictions dialing down from six to three this year, aligning more closely with the Fed's own forecasts.

Despite the market's recent rally being largely driven by an expansion in valuations, the latest earnings season has provided reassurance that corporate profitability is on the rise. This suggests that equities may continue to trend upwards, albeit with potential bouts of increased volatility. As earnings season draws to a close, investors are shifting their focus back to economic indicators and the upcoming Federal Reserve meeting in March, which will offer fresh insights into economic and interest-rate projections.

The bond market, on the other hand, presents a different narrative. Investment-grade bonds dipped in February, but there's a silver lining. As inflation shows signs of abating and the Fed considers rate cuts potentially starting in June, there's an opportunity for a bond market rebound. This could be an opportune moment for investors to consider extending the duration of their fixed-income portfolios, especially as the likelihood of a multiyear rate-cutting cycle by the Fed becomes more apparent.

Notably, the dominance of the "Magnificent 7" mega-cap tech stocks in the U.S. equity market is showing signs of waning. While NVIDIA, Meta, and Amazon have propelled the market forward, others like Microsoft, Apple, and Alphabet have lagged behind, with Tesla experiencing a significant drop year-to-date. This could signal a forthcoming shift in market leadership, with investors potentially turning their attention to undervalued segments of the market, such as mid- and small-cap stocks.

In conclusion, February's market performance has been a testament to the resilience of equities in the face of rising rates and the potential for continued corporate earnings growth. While bonds have faced headwinds, there's potential for resurgence as the Fed adjusts its policy stance. As we move forward, the market's ability to sustain its momentum will be closely tied to economic data, corporate profitability, and policy decisions from central banks. Investors would do well to keep a watchful eye on these developments as they calibrate their portfolios for the rest of the year.

AI stock picks for the week (Large Cap S&P 500)