The Monday Charge: March 11, 2024

As the U.S. labor market navigates through the early months of 2024, recent data suggests a subtle yet notable cooling trend, potentially signaling a shift in the economic landscape. The latest figures indicate an uptick in the unemployment rate, reaching its highest point since January 2022...

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

The biggest movers last week on price and volume (Large Cap S&P 500)

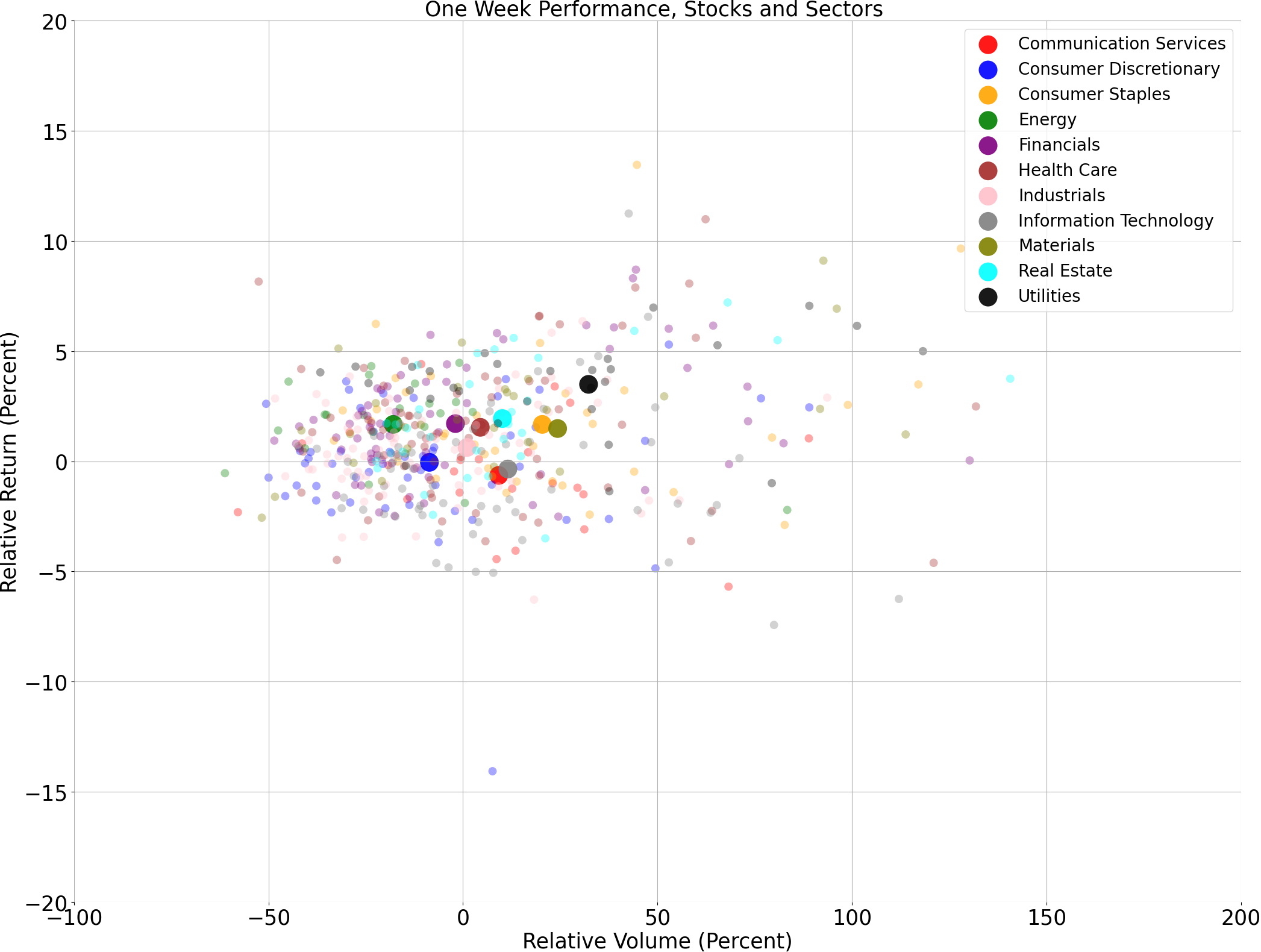

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

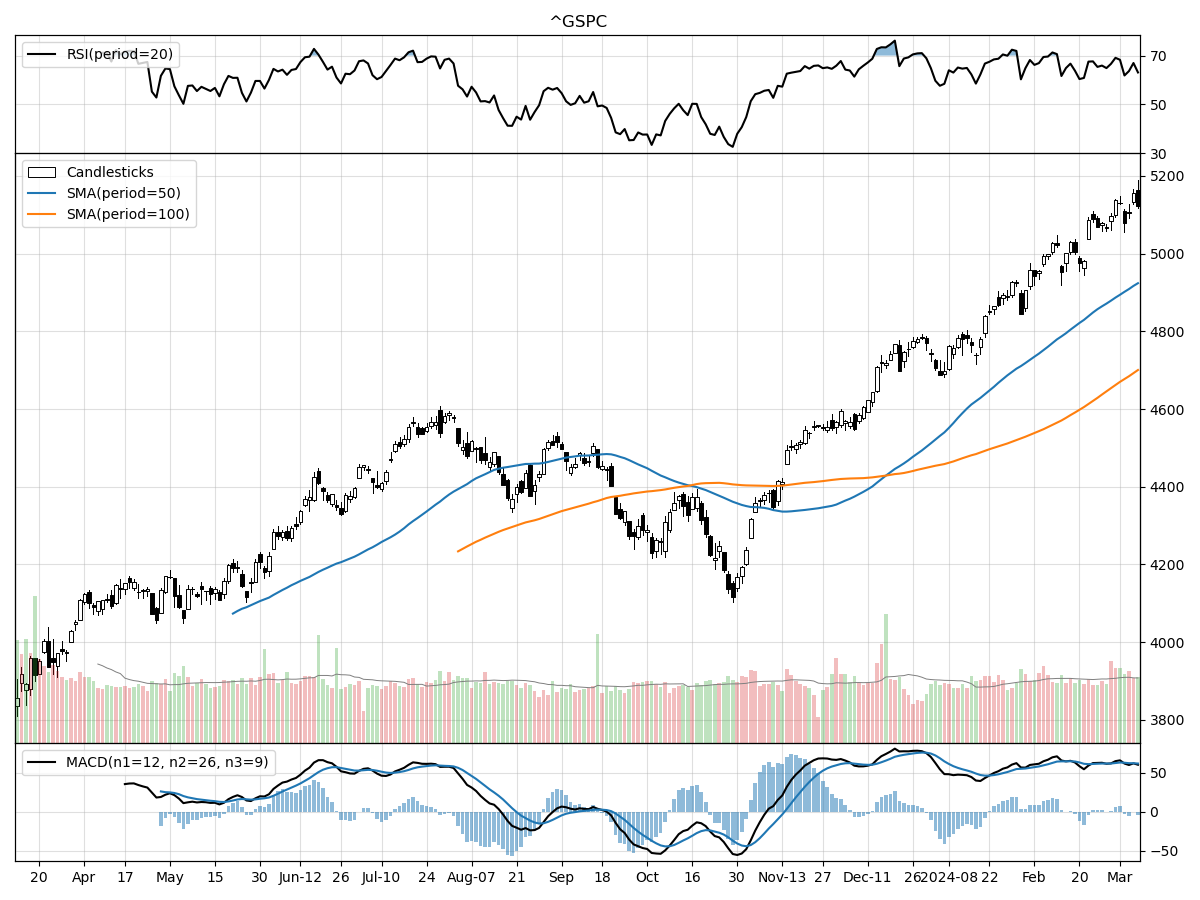

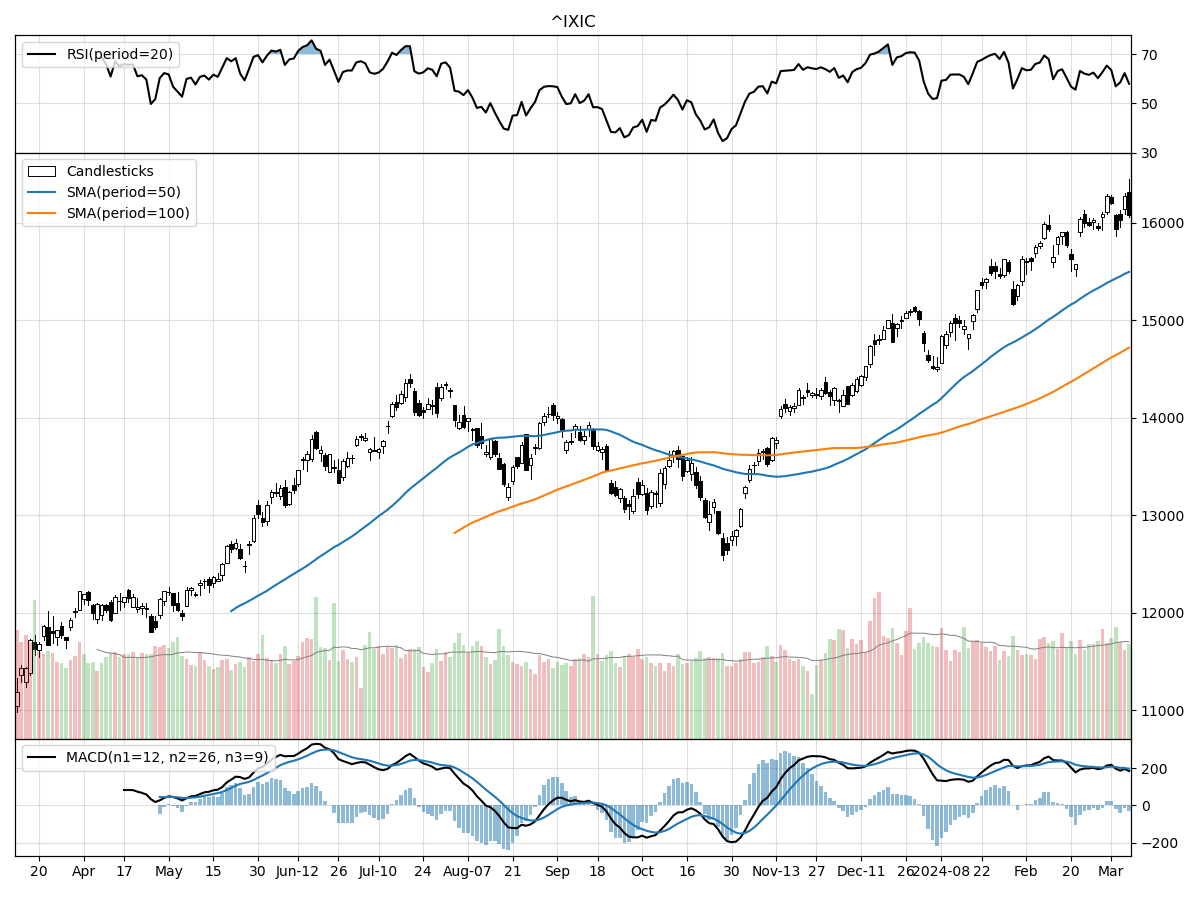

A technical analysis across indices

S&P500

Nasdaq

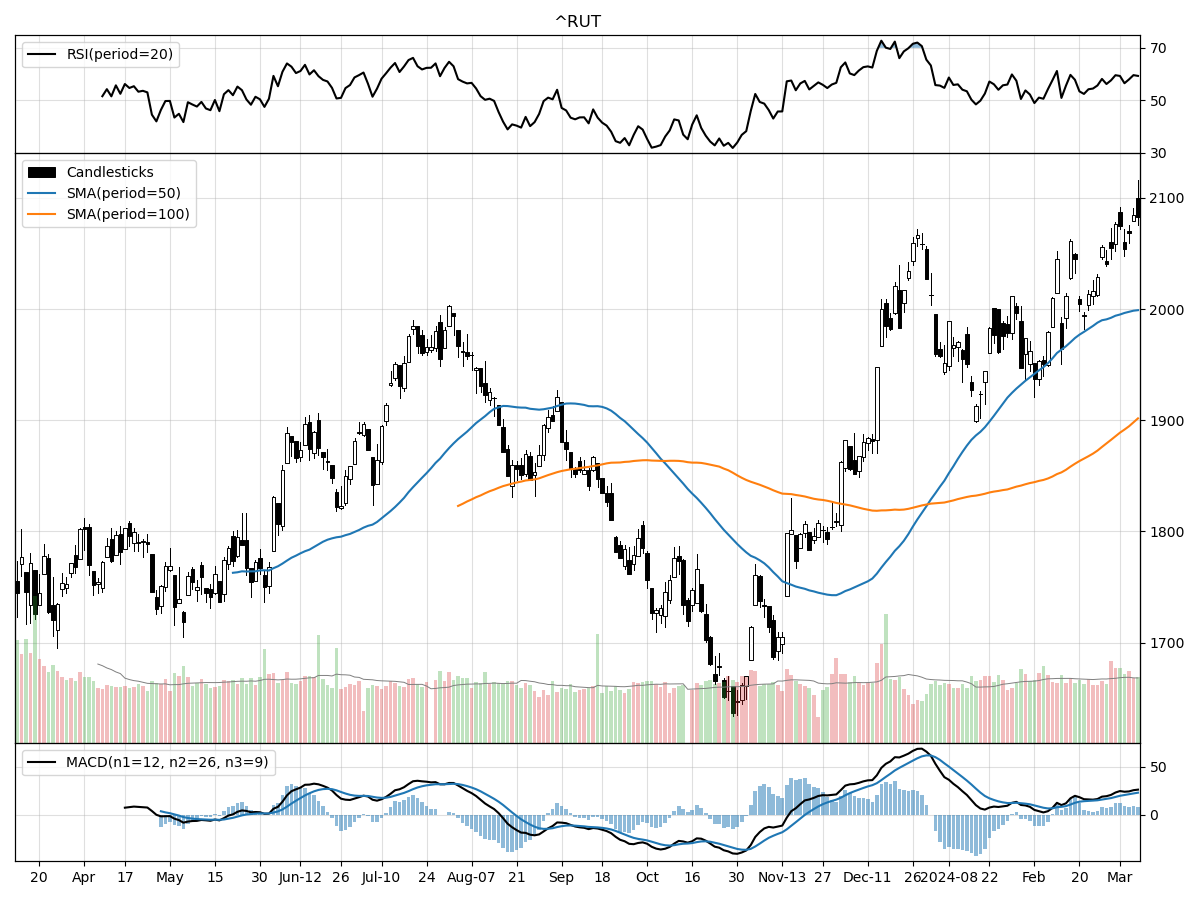

Russell 2000

When comparing the technical performances across these three major indices – the S&P 500, Nasdaq, and the Russell 2000 Small Cap – several key points stand out. Firstly, all indices are currently experiencing bullish momentum as indicated by their respective MACD (Moving Average Convergence Divergence) values, which are positive. The S&P 500's MACD is at 61.61, the Nasdaq's is significantly higher at 196.6, and the Russell 2000's is at 22.87. This suggests that while all indices are demonstrating upward trends, the strength of the trend is most pronounced in the Nasdaq, followed by the S&P 500, and is least strong in the Russell 2000.

In terms of price relative to their 52-week highs and lows, all three indices are currently much closer to their 52-week highs than their lows, with the S&P 500 and Russell 2000 both at 0 percent below their highs, indicating they are at or very near peak levels, while the Nasdaq is only 1 percent below its high. The current prices of all three indices are significantly above their respective 52-week lows, with the Nasdaq showing the greatest increase (44 percent above), followed by the S&P 500 (32 percent above), and the Russell 2000 (27 percent above). This suggests a robust recovery from any lows experienced over the past year, with the Nasdaq leading in terms of price recovery.

Volume analysis shows daily trading volumes for the Nasdaq are higher than its longer-term average, suggesting increased investor interest or activity in the stocks that comprise this tech-heavy index. The S&P 500 and the Russell 2000 are also seeing volumes around their respective longer-term averages. All indices are under moderate buying pressure and are being accumulated, as indicated by money flow indicators. However, the RSI (Relative Strength Index) points to modest overbought conditions for the S&P 500 and Russell 2000, which could indicate a potential for a pullback or consolidation in the near term, while the Nasdaq's RSI suggests a more balanced market that is neither overbought nor oversold.

In summary, all indices are showing bullish signs with the Nasdaq having the strongest upward momentum and greatest recovery from its 52-week low, suggesting a strong investor confidence particularly in the technology sector. The S&P 500 and Russell 2000 also show positive trends but are slightly overbought, which could lead to some near-term volatility or consolidation. Investors may want to keep an eye on these overbought conditions while also considering the strong bullish signals when making investment decisions.

Last week vs. history (Large Cap S&P 500)

Market Commentary

Signs of Cooling in the U.S. Labor Market Emerge Amidst Economic Uncertainty

As the U.S. labor market navigates through the early months of 2024, recent data suggests a subtle yet notable cooling trend, potentially signaling a shift in the economic landscape. The latest figures indicate an uptick in the unemployment rate, reaching its highest point since January 2022, a development that warrants close scrutiny from policymakers and investors alike.

The Institute for Supply Management (ISM) Manufacturing and Services Employment indexes have both retreated into contractionary territory, underscoring a potential slowdown in labor demand. In the manufacturing sector, the employment index has contracted for five consecutive months, with a majority of industries reporting a decline in workforce numbers. The services sector, which had previously exhibited growth, also reported a contraction in employment, although some industries anticipate a resurgence in hiring as the year progresses.

This downward trend in employment is mirrored by a reduction in job openings and a deceleration in the year-over-year growth of average hourly earnings. These indicators suggest a rebalancing of the labor market, with a gradual increase in labor supply meeting a softer demand for workers. Such a dynamic could lead to a tempering of wage inflation, contributing to a more stable employment environment.

The Federal Reserve, under the guidance of Chair Jerome Powell, has signaled a cautious approach to monetary policy, hinting at the possibility of a rate-cutting cycle commencing once sufficient confidence in the economic outlook is established. The recent labor market data adds a layer of complexity to the Fed's deliberations, as it points to easing inflationary pressures, potentially paving the way for rate reductions as early as June this year.

Financial markets have responded to these developments with a mix of caution and optimism. Last week saw a modest dip in stock market performance, while the bond market experienced gains, buoyed by lower Treasury yields. Despite this, the S&P 500 remains in close proximity to record highs, and the market has not experienced a significant correction in recent months.

Investment strategists suggest that the current market conditions may be ripe for consolidation, although there is little expectation for a deep or extended bear market. The anticipated moderation of inflation, coupled with the Fed's likely shift towards rate cuts later in the year, and a labor market that remains robust despite recent softening, provides a foundation for cautious optimism among investors.

In light of these developments, investors are encouraged to view market volatility as an opportunity to enhance their portfolios, diversify across sectors, and consider lengthening the duration of investment-grade bonds. While the economic landscape presents its challenges, a strategic approach to investing can leverage these conditions to achieve long-term financial goals.

AI stock picks for the week (Large Cap S&P 500)