The Monday Charge: July 29, 2024

In a notable shift in market dynamics, equity markets have been undergoing a rotation, with small-cap stocks and value and cyclical sectors outperforming their mega-cap technology and growth counterparts.

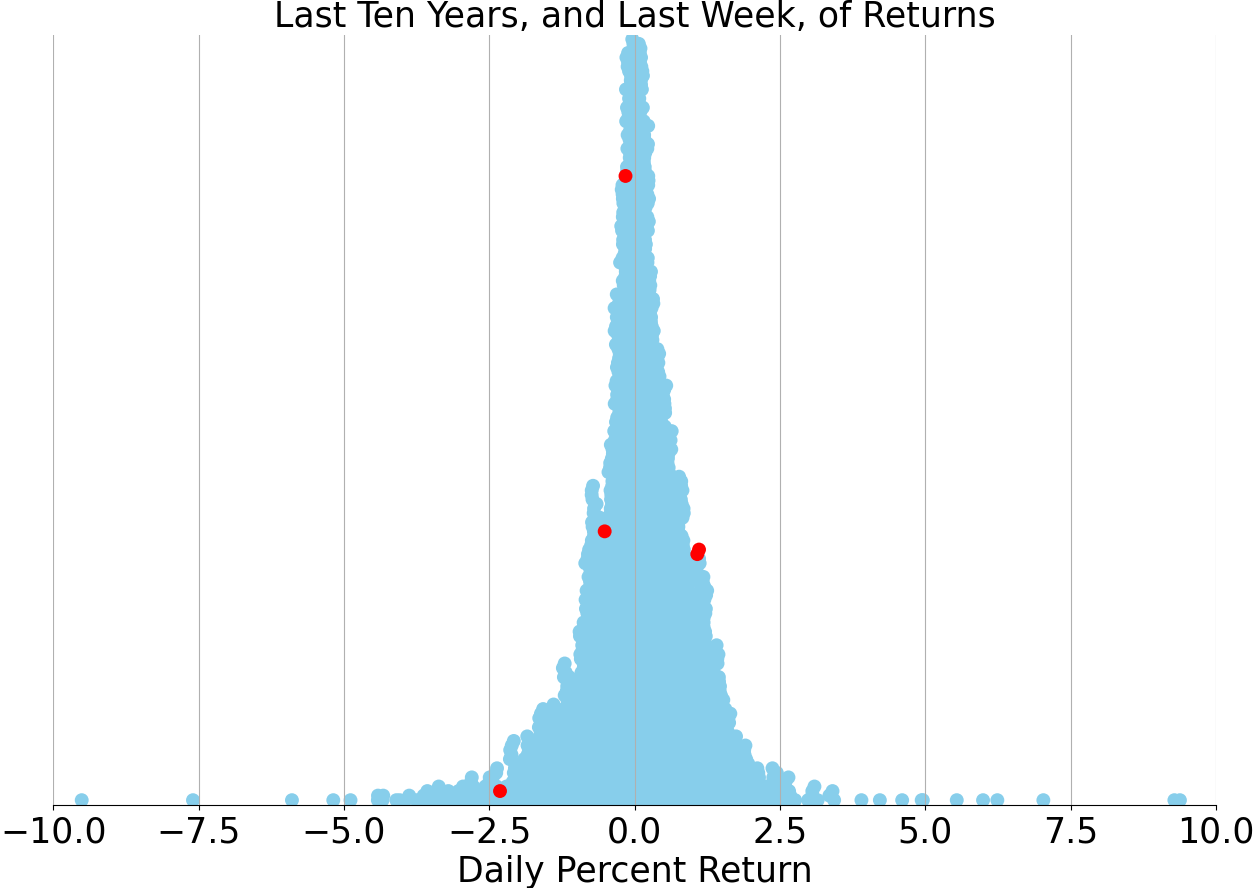

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

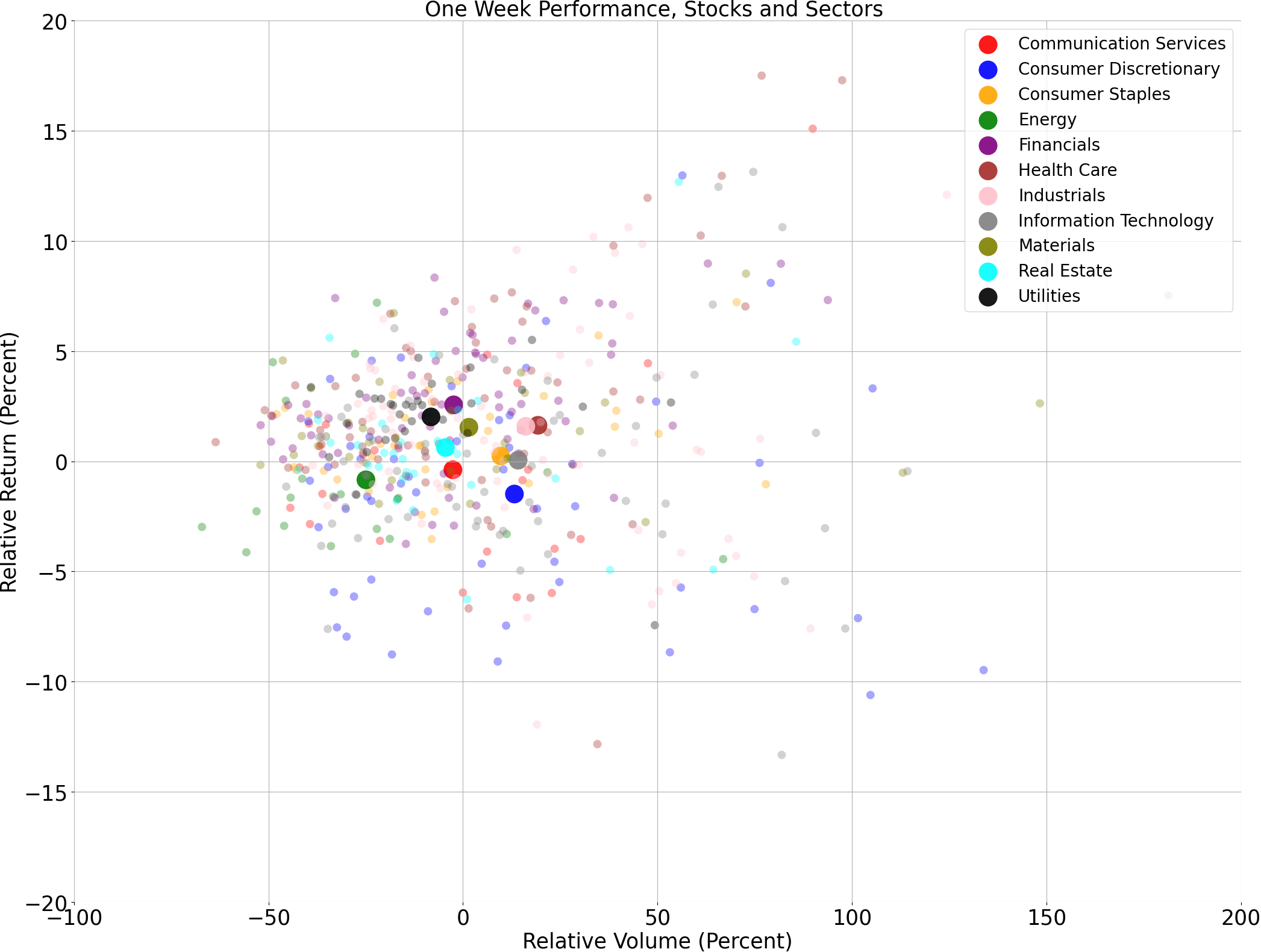

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

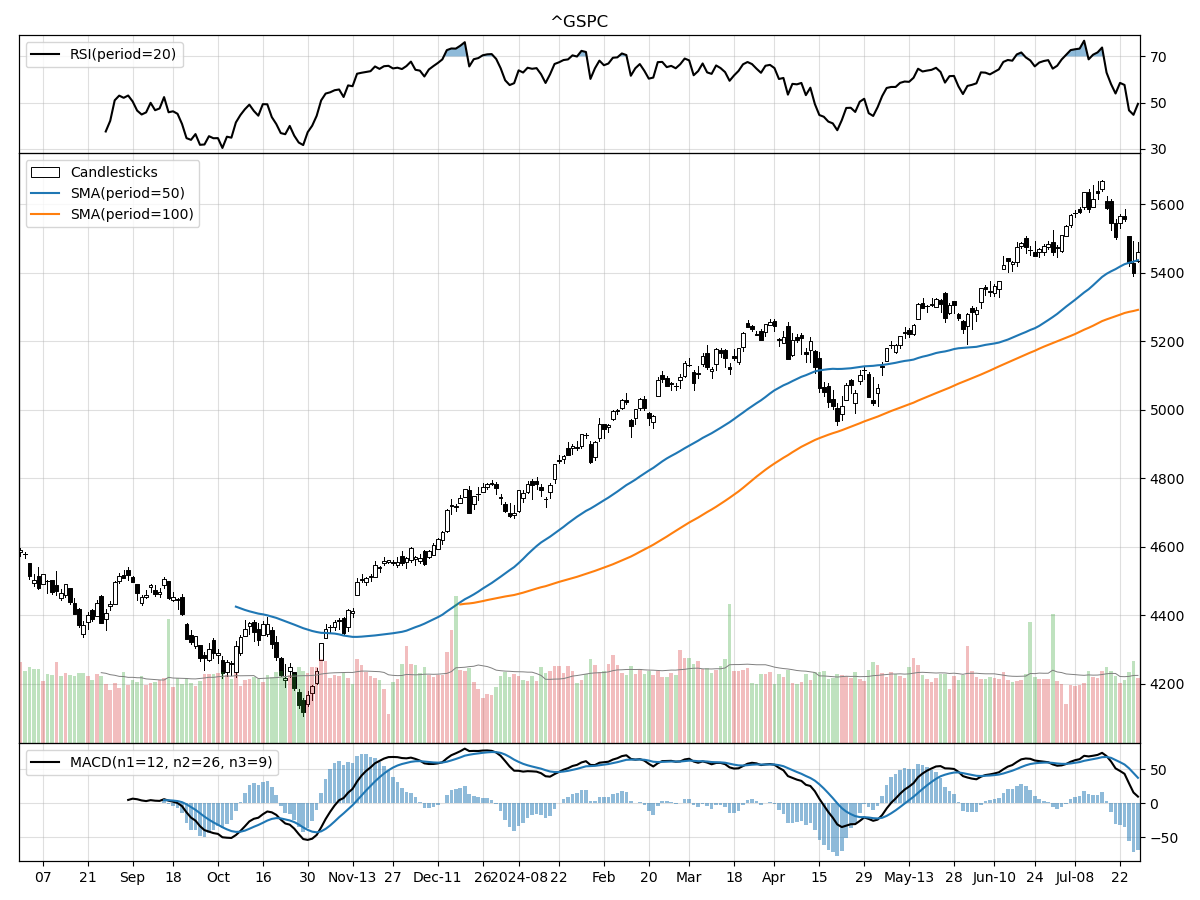

S&P500

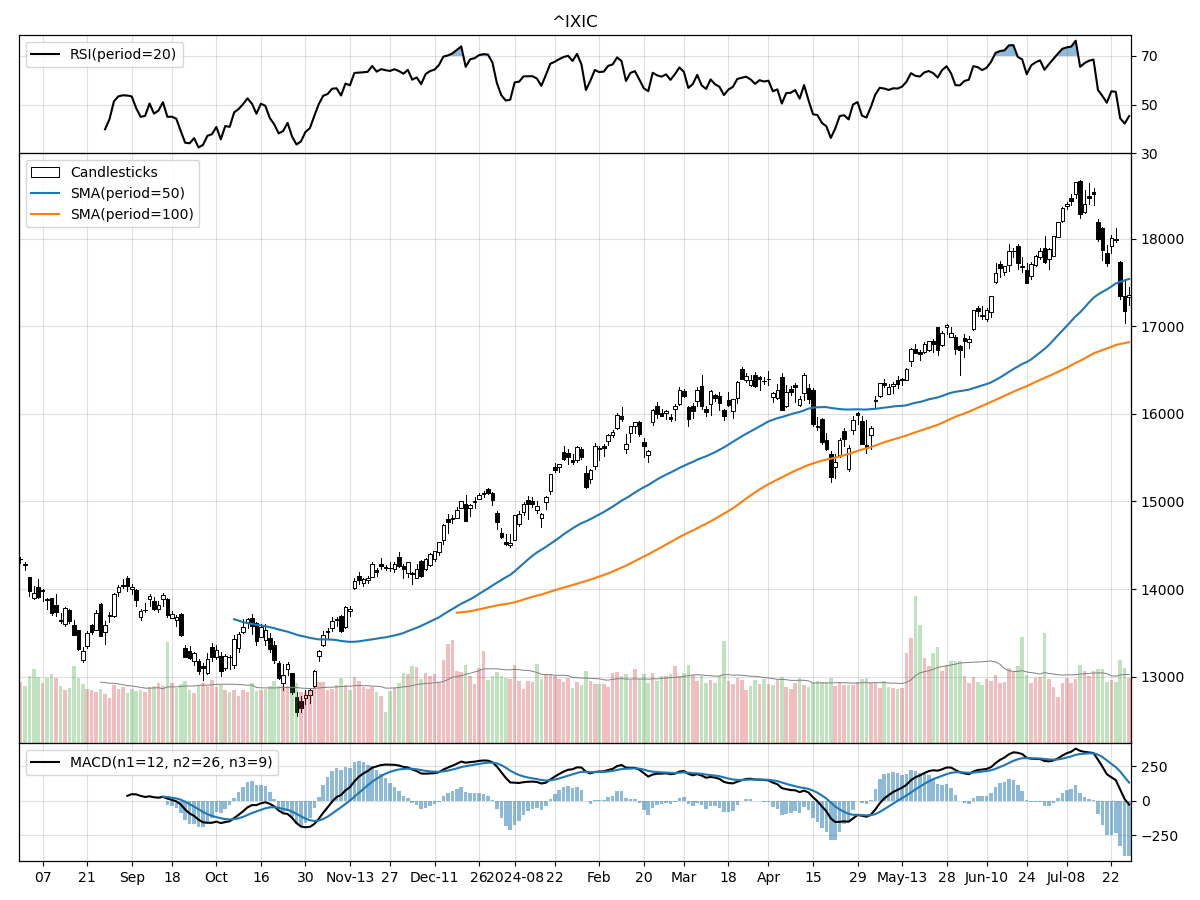

Nasdaq

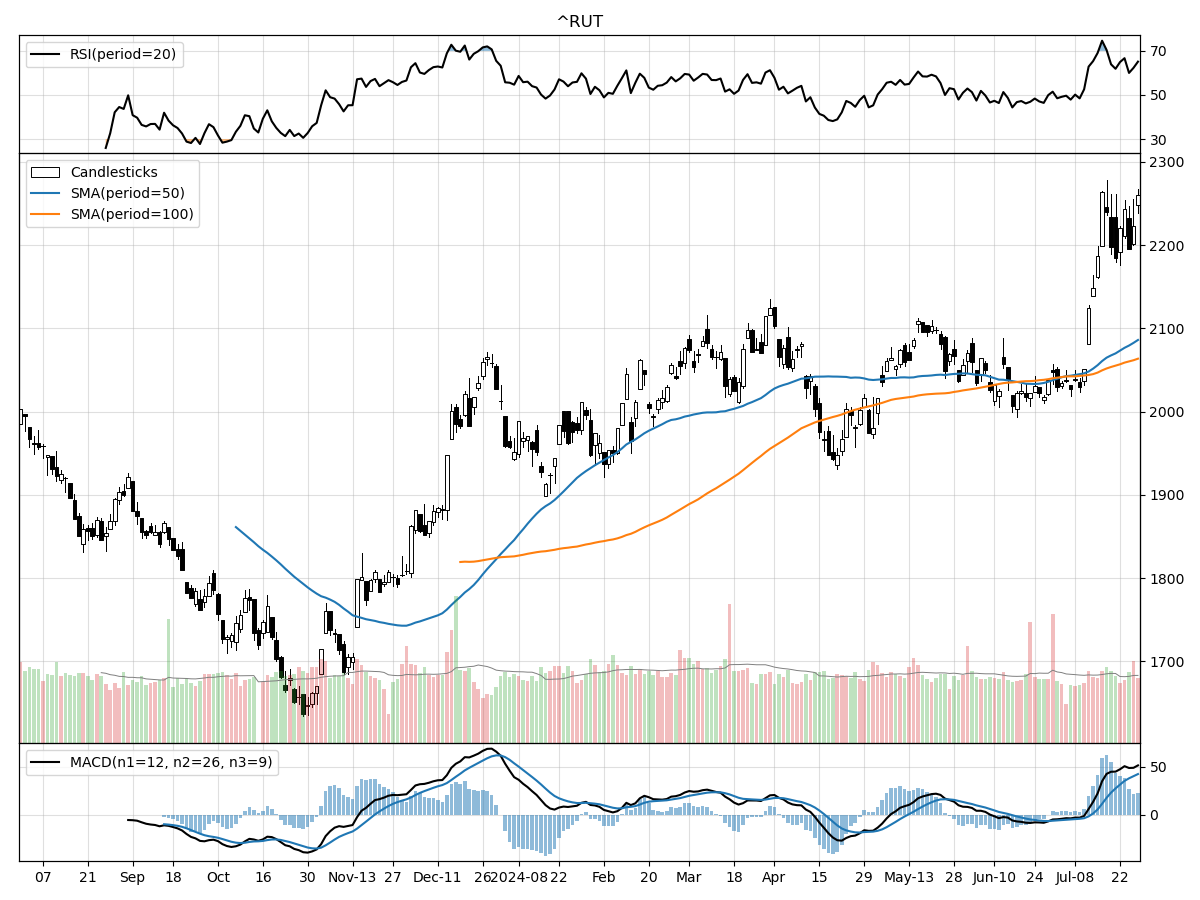

Russell 2000

The S&P 500, Nasdaq, and Russell 2000 indices have shown distinct yet somewhat correlated technical performances recently. The S&P 500 is currently trading at 5459.10, which is 32% above its 52-week low and 3% below its 52-week high. Over the past three months, the index has experienced a modest rise of 8.78%. Despite this upward trend, the recent daily volume has been slightly below the long-term average, indicating a potential slowdown in trading activity. The Money Flow indicators suggest moderate buying pressure, though the stock is under distribution, hinting at mixed sentiment among investors. The MACD is bullish at 37.54, reinforcing a cautiously optimistic outlook.

In comparison, the Nasdaq is trading at 17357.88, standing 37% above its 52-week low and 6% below its 52-week high. The index has outperformed the S&P 500 in terms of recent growth, with an 11.23% increase over the last three months. The daily trading volume has been above its long-term average, suggesting robust market participation. However, Money Flow indicators point to moderate selling pressure and distribution, which could imply that some investors are taking profits. Despite this, the MACD remains bullish at 132.9, indicating continued upward momentum.

The Russell 2000, representing small-cap stocks, has shown the strongest performance among the three indices. Currently priced at 2260.07, it is 38% above its 52-week low and has reached its 52-week high. Over the past month and three months, the index has surged by 10.37% and 14.13%, respectively, outperforming both the S&P 500 and Nasdaq. The recent daily volume is slightly below the long-term average, yet Money Flow indicators suggest moderate buying pressure. Despite being under distribution, the strong MACD reading of 42.34 signals bullish sentiment, indicating that investors are optimistic about the growth prospects of small-cap stocks.

Last week vs. history (Large Cap S&P 500)

Market Commentary

In a notable shift in market dynamics, equity markets have been undergoing a rotation, with small-cap stocks and value and cyclical sectors outperforming their mega-cap technology and growth counterparts. This change marks a departure from the dominance of large-cap growth sectors and the so-called "Magnificent 7"—Apple, Microsoft, Amazon, Meta Platforms, Alphabet, Tesla, and NVIDIA—that have led the market for over a year and a half. Several key factors have contributed to this rotation, including cooling inflation, anticipated Federal Reserve interest rate cuts, and a potential pickup in consumption and economic growth. These elements suggest that the broadening of market leadership could have staying power, though not without potential volatility.

Despite this shift, it is important to note that the U.S. economy is not in an early expansion stage, typically a period when small-caps and cyclical sectors exhibit sustained leadership. Economic growth is expected to soften in the coming quarters, yet the narrative of a "soft landing" remains plausible if inflation continues to cool and the Fed cuts rates. Large-cap technology companies, with their solid earnings growth and strong balance sheets, may also benefit from lower rates and improved consumption. This could lead investors to diversify into both growth and cyclical/value sectors, promoting a true broadening of market leadership.

Political developments have also added a layer of uncertainty to the markets. President Biden's recent decision to exit the presidential race and endorse Vice President Kamala Harris has reshaped the political landscape. Harris has quickly garnered the support of a majority of Democratic delegates, making her the party's nominee. Early polling and betting odds indicate a much closer race between Harris and former President Trump compared to Biden, adding to market volatility as investors grapple with the potential implications of this political shift.

Market volatility is not uncommon in election years, and historical data shows that it tends to increase ahead of election day before subsiding afterward. This pattern is largely due to the lifting of uncertainty once the election results are known. Despite the political turbulence, the fundamentals of the market remain supportive of ongoing equity expansion. Second-quarter GDP growth exceeded expectations, driven by healthy consumption growth, indicating that the economy remains resilient.

As we navigate through this period of market and political volatility, the focus should remain on the underlying fundamentals. The backdrop of cooling but positive economic growth, easing inflation, and a Fed poised to cut rates continues to support equity markets broadly. Investors should use this period of volatility to diversify and rebalance their portfolios, adding quality investments at more attractive prices. Sectors like industrials and utilities are expected to participate more in the broadening of market leadership.

While cash-like instruments such as CDs and money-market funds may seem attractive in a volatile environment, they carry the risk of losing value as interest rates head lower. The coming months could provide opportunities to dollar-cost average into strategic allocations in equities and bonds, aligning with individual risk and reward preferences. This approach ensures that long-term financial goals remain on track despite short-term market fluctuations.

In summary, the recent rotation in market leadership from mega-cap technology to small-cap and value sectors, coupled with political shifts, has introduced new dynamics into the market. However, the fundamentals of the economy remain strong, supported by positive economic growth, easing inflation, and anticipated Fed rate cuts. Investors should embrace portfolio diversification and strategic rebalancing to navigate through this period of uncertainty and position themselves for long-term success.

Stock study for Tuesday

Lamb Weston Holdings, Inc. (LW) is a prominent global producer, distributor, and marketer of value-added frozen potato products, such as French fries, operating in over 100 countries. Headquartered in Idaho, the company operates primarily in two segments: North America and International. In North America, Lamb Weston’s products are sold to restaurants, foodservice distributors, non-commercial channels, and retailers under brands like Lamb Weston, Grown in Idaho, and Alexia. Internationally, the company holds significant joint ventures, including a 90% interest in an Argentine venture and full ownership of a European venture. Lamb Weston focuses on research and development to drive future revenue and profit growth through new product creation, process innovations for sustainability, and joint menu planning with customers.

Comments ()