The Monday Charge: July 15, 2024

In the first half of 2024, U.S. equity markets experienced a notable upswing, with large-cap stocks leading the charge with a 15.3% gain. This surge was primarily driven by the burgeoning excitement around artificial intelligence (AI) and strong profit growth...

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

The biggest movers last week on price and volume (Large Cap S&P 500)

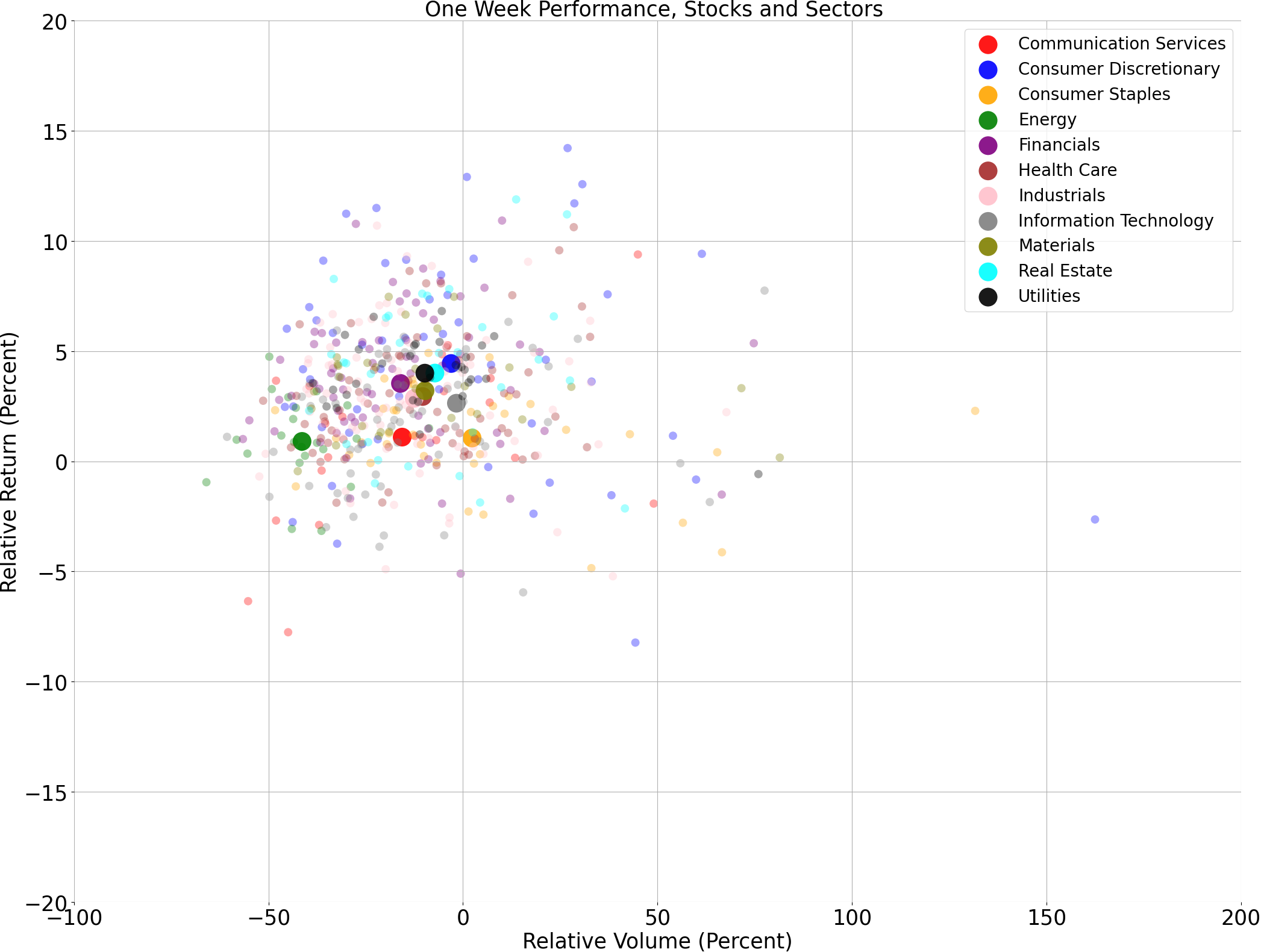

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

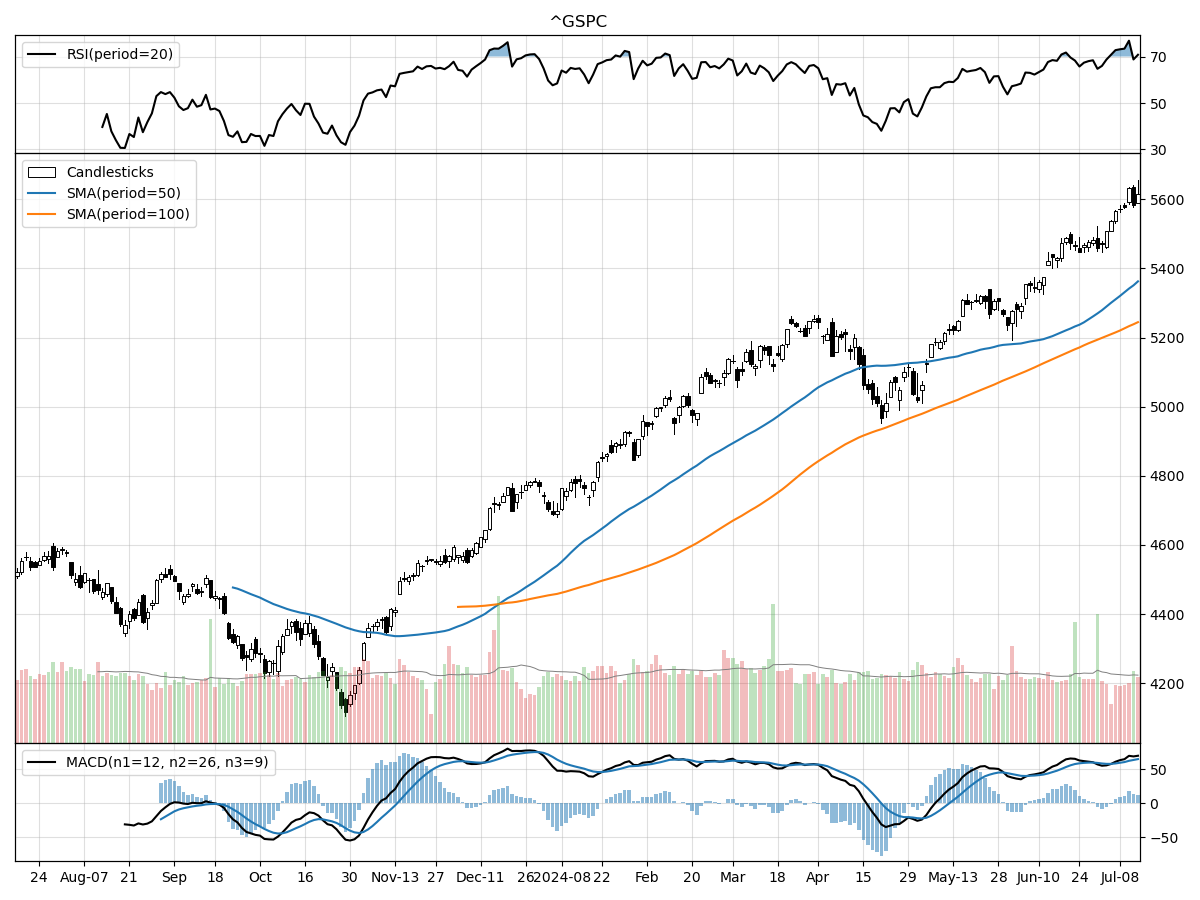

S&P500

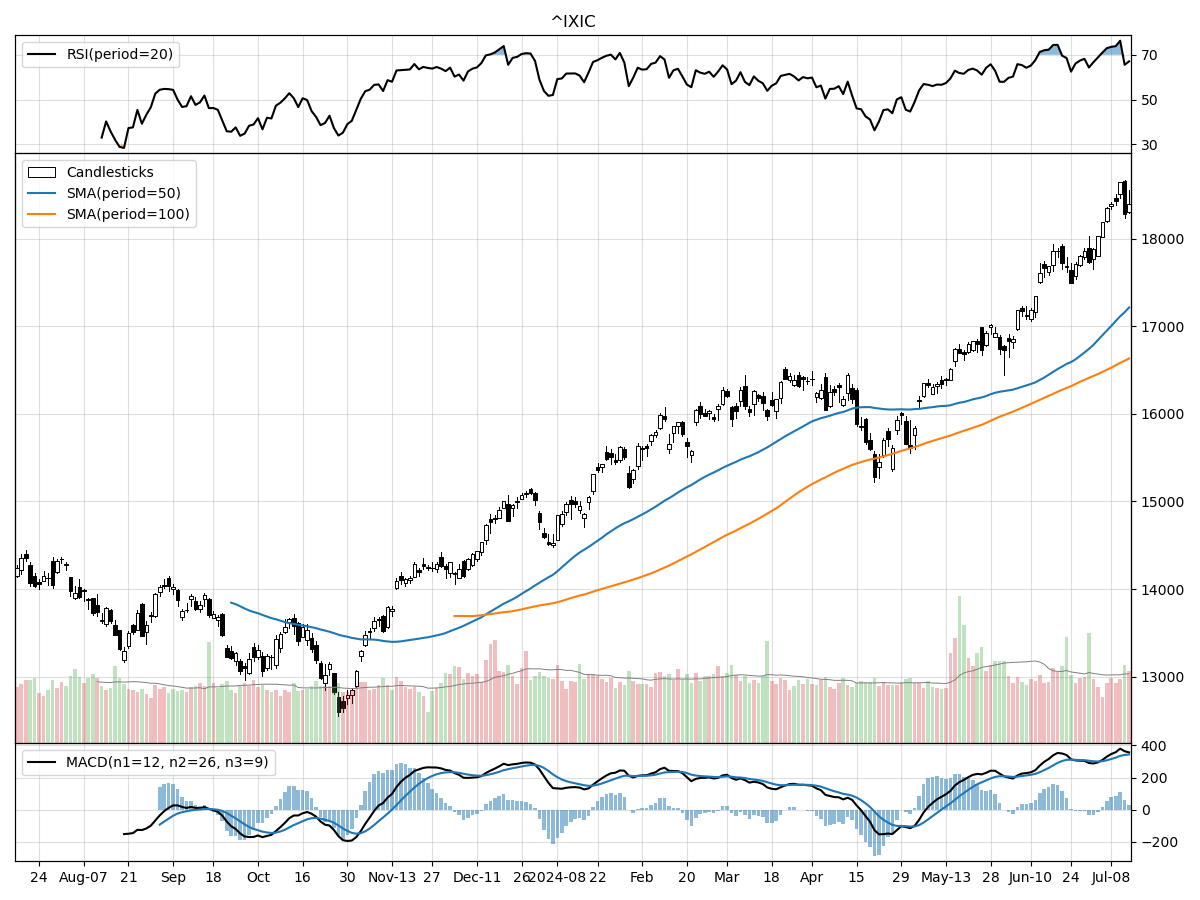

Nasdaq

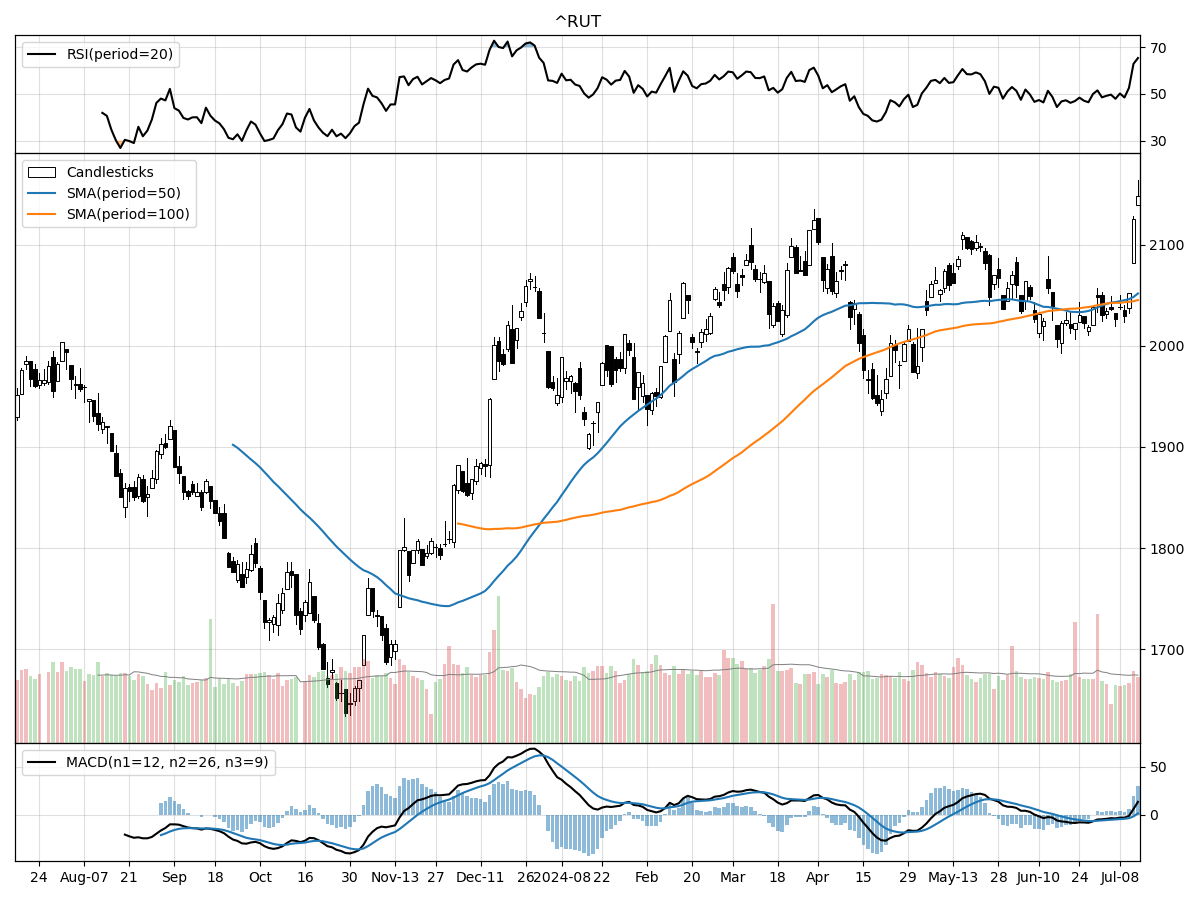

Russell 2000

The S&P 500, Nasdaq, and Russell 2000 indices are all exhibiting robust technical performances, but there are noteworthy differences in their trajectories and indicators. The S&P 500 is currently trading at an all-time high, sitting 36% above its 52-week low. Over the past three months, the index has risen by approximately 11.81%, which indicates a solid upward momentum. Despite a stable performance over the last month, the RSI suggests that the S&P 500 is overbought, hinting at a potential for a pullback. The MACD remains bullish at 65.16, suggesting continued upward momentum in the near term. The volume metrics are slightly below the long-term average, indicating moderate buying pressure and accumulation.

In comparison, the Nasdaq index is showing even stronger performance metrics, trading just 1% below its 52-week high and 46% above its 52-week low. The index has surged by 17.31% in the past three months, outpacing both the S&P 500 and the Russell 2000. The Nasdaq's volume is notably higher than its long-term average, reflecting substantial buying pressure. The RSI indicates that the index is modestly overbought, which could also signal a near-term correction. With a bullish MACD of 343.6, the Nasdaq's technical indicators suggest a more aggressive upward momentum compared to the S&P 500.

The Russell 2000 index, representing small-cap stocks, has also reached its 52-week high, similar to the S&P 500. It stands 31% above its 52-week low and has experienced a 10.28% rise over the past three months. However, the Russell 2000 has shown a more pronounced increase of 5.36% in just the last month. The RSI indicates that the index is overbought, suggesting a potential for a short-term pullback. Volume metrics are slightly below the long-term average, indicating moderate buying pressure and accumulation. The MACD at 1.159 is bullish but less pronounced compared to the Nasdaq and S&P 500, indicating a steadier, yet positive, momentum.

In summary, while all three indices are exhibiting bullish trends, the Nasdaq shows the strongest recent performance and buying pressure, followed by the S&P 500 and the Russell 2000. Investors should be mindful of the overbought conditions indicated by the RSI across all indices, which could lead to short-term corrections despite the generally bullish outlook.

Last week vs. history (Large Cap S&P 500)

Market Commentary

U.S. Markets Surge in First Half of 2024 Amid AI Enthusiasm and Robust Profit Growth

In the first half of 2024, U.S. equity markets experienced a notable upswing, with large-cap stocks leading the charge with a 15.3% gain. This surge was primarily driven by the burgeoning excitement around artificial intelligence (AI) and strong profit growth, particularly in the technology and communications services sectors. The enthusiasm for AI has not only buoyed these sectors but also contributed to a broader optimism in the market. Investors have been particularly drawn to mega-cap AI stocks, which have shown impressive earnings and maintain substantial cash reserves, allowing for significant reinvestment and shareholder returns.

However, the bond market faced headwinds as interest rates climbed, putting pressure on investment-grade bonds. Despite this, resilient economic growth provided support for lower-quality issuers, leading to modest gains in U.S. high-yield bonds and emerging-market debt. The European Central Bank (ECB) and the Bank of Canada (BoC) were the first among G7 central banks to lower policy rates after a series of rate hikes aimed at curbing inflation. In the U.S., inflation saw a downward trend in the second quarter, following a period of higher-than-expected readings earlier in the year.

International stocks also performed well in the first half of 2024, with emerging-market stocks outpacing their developed international large-cap counterparts. China's fiscal support played a significant role in boosting emerging-market stocks, while improved economic growth in Europe and robust corporate profit growth in Japan helped developed international stocks. However, the strength of the U.S. dollar partially offset these gains. The global market landscape continues to be influenced by varying economic policies and growth trajectories across different regions.

The U.S. economy has shown signs of cooling after the above-trend growth witnessed in 2023, with GDP growth slowing to an annualized rate of 1.4% in the first quarter of 2024. This moderation is expected to continue into the second half of the year, driven by a normalization in the labor market and softening consumer spending. The labor market has started to show signs of better balance, with the unemployment rate rising to 4.1%, the highest since 2021. Indicators such as job openings and the quits rate have fallen to recent lows, suggesting further softening ahead.

Inflation has been a key focus, with recent data showing a downward trend. In June, the consumer price index (CPI) inflation was at 3.0% annualized, the lowest since March 2021, while core CPI, excluding volatile food and energy prices, ticked down to 3.3% annualized. Two potential drivers could help bring core PCE inflation closer to the Federal Reserve's 2% target: a moderation in shelter and rent components of inflation, and a cooling of services inflation as wage growth slows. These factors are crucial for the Fed's future policy decisions.

Looking ahead, technology-focused sectors are expected to continue playing a significant role in portfolios. The technology, communication services, and consumer discretionary sectors, which include mega-cap AI stocks, represent more than half of the S&P 500. While recent earnings growth has been largely driven by technology-related companies, other sectors are expected to contribute equally by the fourth quarter. As the Federal Reserve moves closer to potential rate cuts, cyclical areas of the market may benefit, supported by lower yields.

Historically, stock markets have experienced volatility in the weeks leading up to U.S. elections, but they typically recover afterward. In the current election cycle, a divided Congress is expected, which means no major new regulation or legislation is likely, regardless of the winning party. Markets generally favor political gridlock as it provides a more predictable operating environment for companies. Over the long term, market fundamentals such as inflation, interest rates, and economic growth tend to have a more significant impact than political events.

The Federal Reserve's June meeting indicated a potential for one interest-rate cut this year, with moderating inflation possibly allowing for cuts in September and/or December. As the timing and pace of these cuts become clearer, short-term yields are expected to decline, likely steepening the yield curve. This scenario presents higher reinvestment risk for short-term bonds and CDs, making intermediate- and long-term bonds and bond funds more attractive for locking in rates. A Fed pivot to rate cuts would be favorable for stocks, with bonds typically performing well during such cycles.

Internationally, a modest recovery appears to be underway in the eurozone, with growth exceeding expectations in the first quarter. Despite historically low unemployment, inflation pressures have eased, prompting the ECB to begin policy easing. This recovery, coupled with U.S. economic normalization, suggests that international developed-market stocks offer potential catch-up opportunities and diversification benefits. Meanwhile, in China, policymakers have introduced measures to support the economy amid an ongoing real estate crisis, although the sustainability of the recent stock rebound remains uncertain.

Overall, the global economic landscape remains complex, with varying regional dynamics and policy responses shaping market outcomes. Investors should remain vigilant and consider diversification to navigate the evolving economic environment. As always, understanding the risks involved in different investments and aligning them with individual financial goals and risk tolerance is crucial for long-term success.

Stock study for Tuesday

(AKAM)

Akamai Technologies Inc. operates in three primary business sectors: security, content delivery, and cloud computing. The company's main platform, Akamai Connected Cloud, utilizes an extensive network infrastructure with over 4,100 edge points in roughly 130 countries to enhance digital experiences and security. Their security solutions focus on protecting against cyberattacks using advanced techniques like "zero trust" and microsegmentation, strengthened by the acquisitions of Guardicore Ltd. and Neosec, Inc. In content delivery, Akamai optimizes web and mobile performance and media delivery for global enterprises. Recently, Akamai has expanded into cloud computing, bolstered by acquiring Linode Limited Liability Company, positioning itself to compete with leading cloud providers through a distributed cloud model aimed at enterprise-grade core computing and edge regions.

Comments ()