The Monday Charge: January 8 2024

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Large Cap S&P 500)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers (Covered on Tuesday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

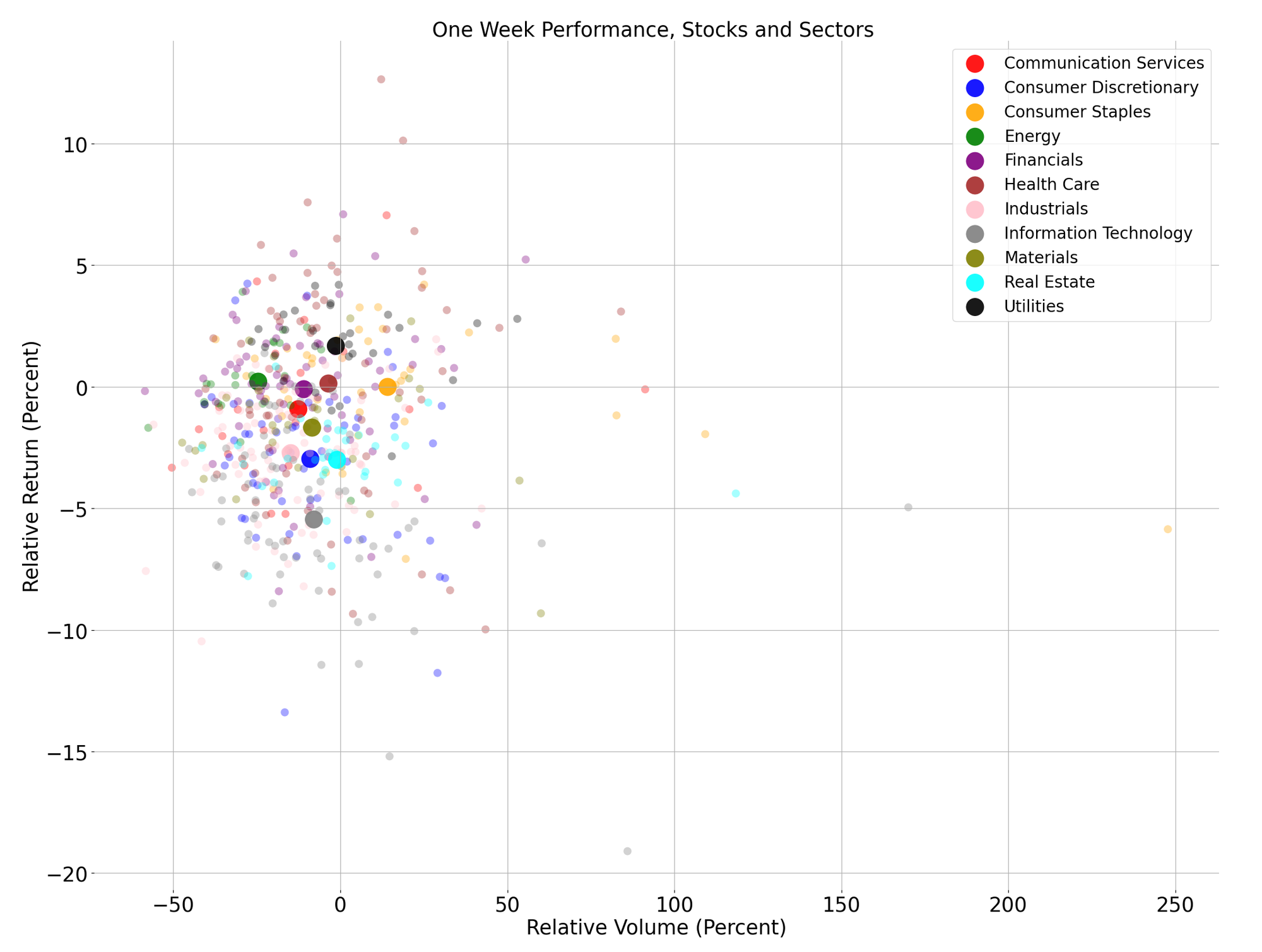

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

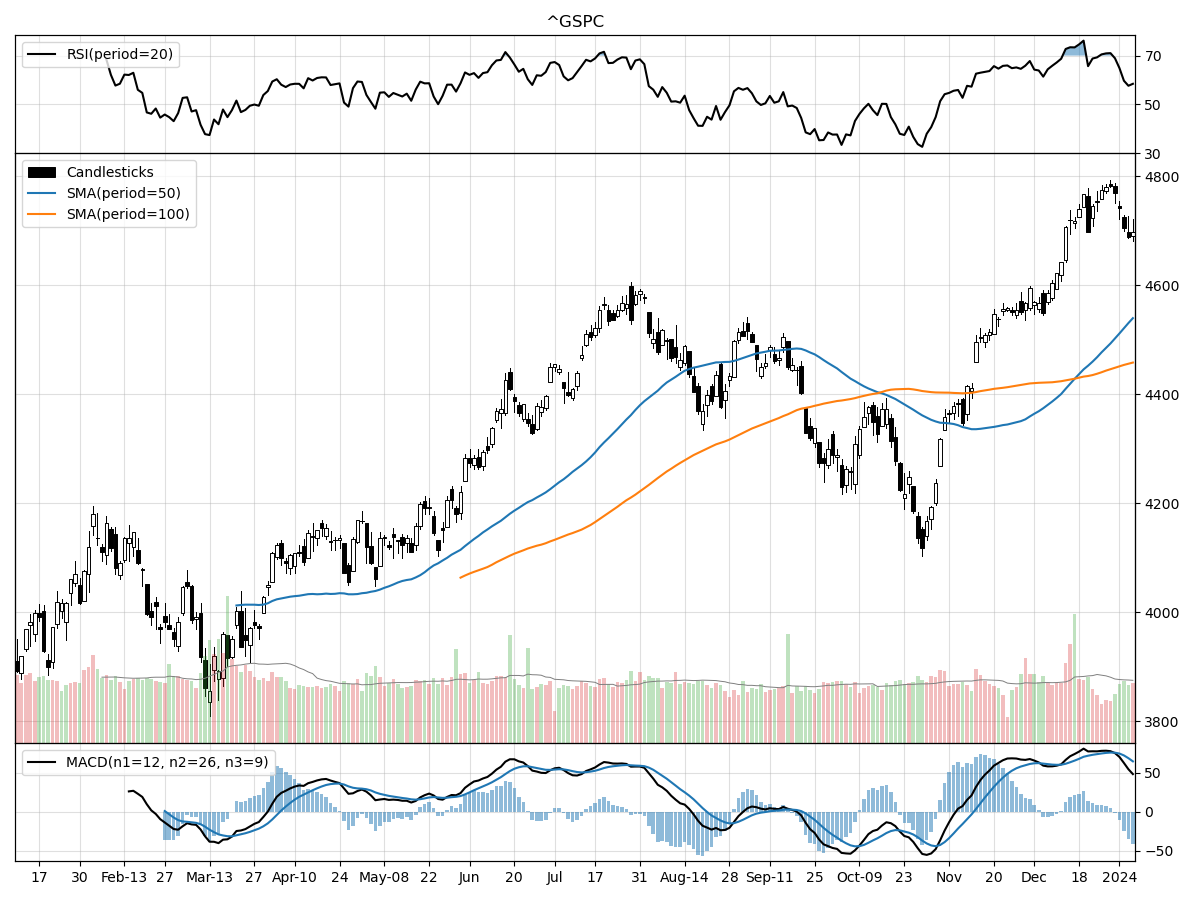

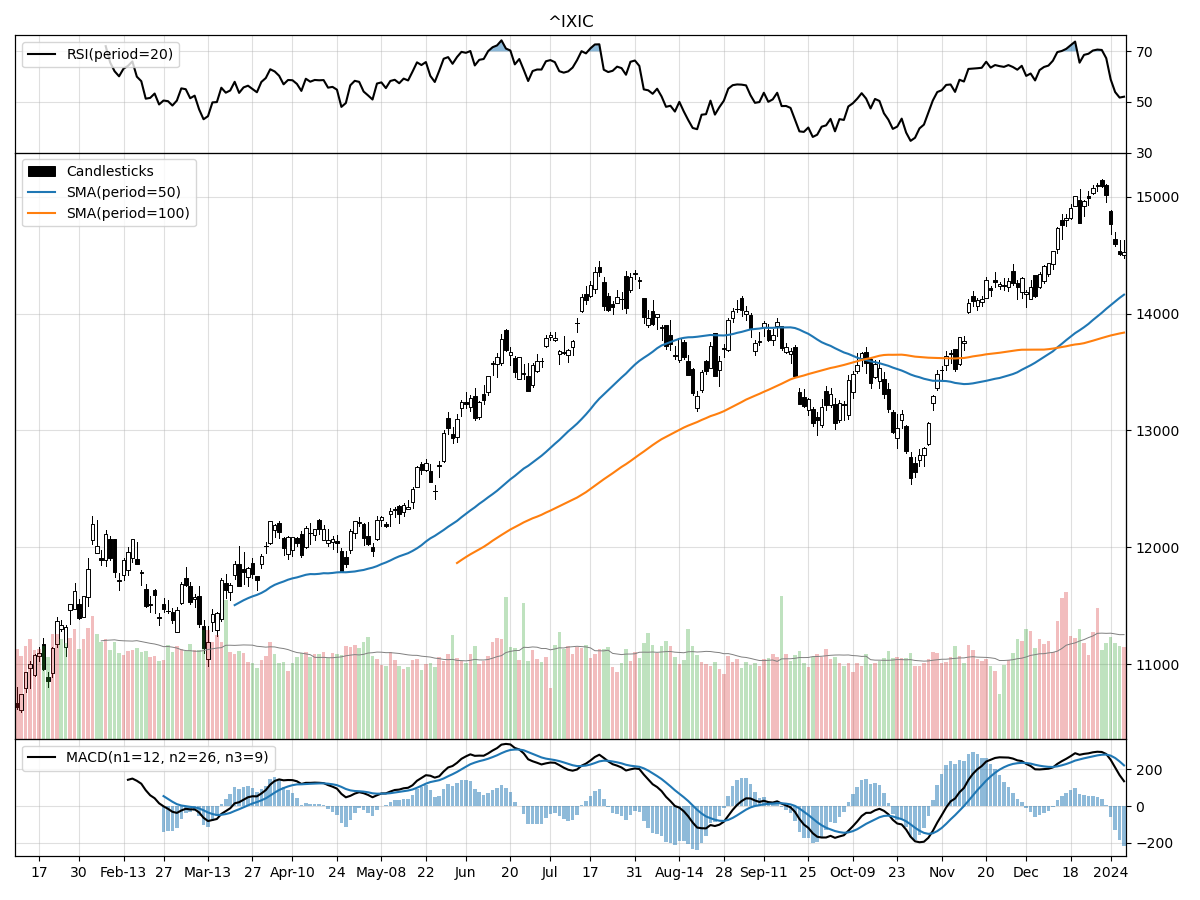

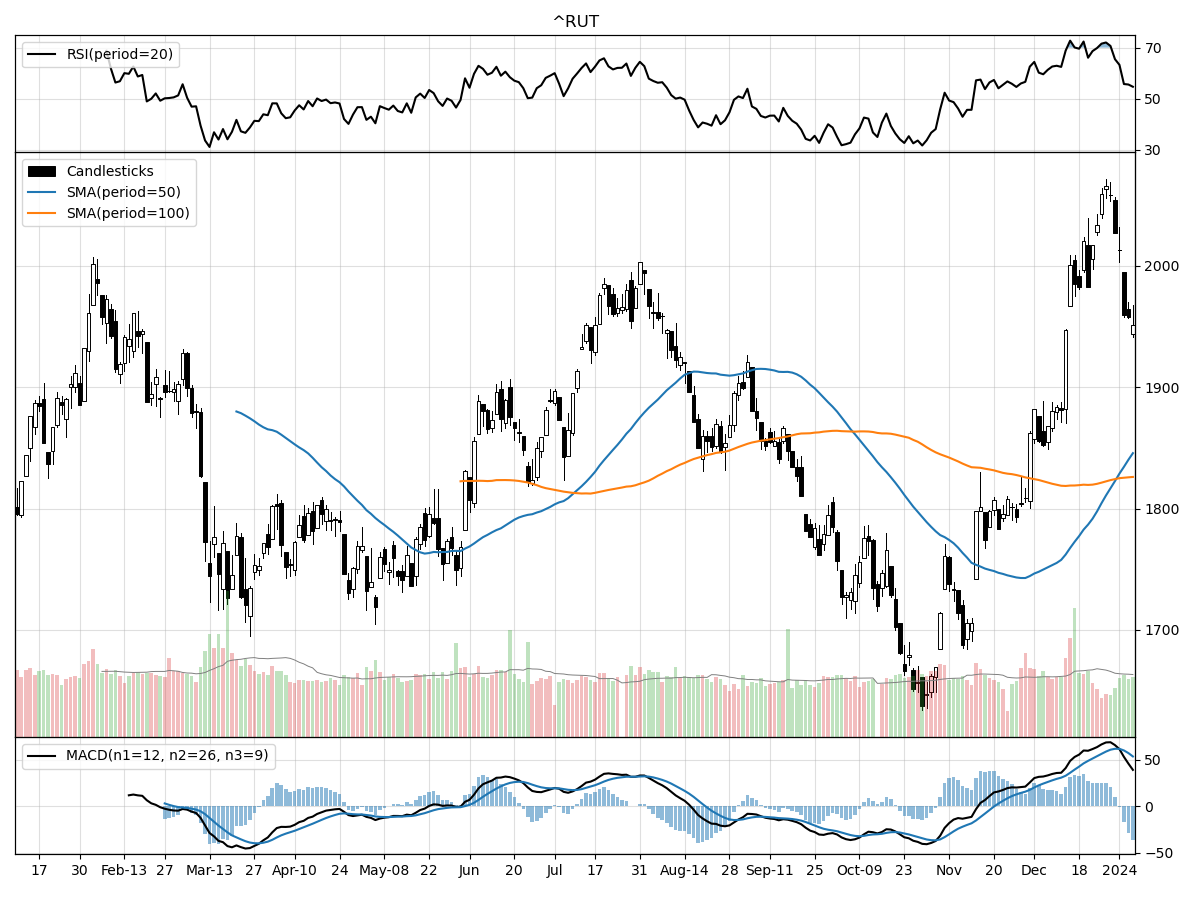

A technical analysis across indices

S&P500

Nasdaq

Russell 2000

The S&P 500, Nasdaq, and Russell 2000 indices are all showing bullish trends, as evidenced by their respective MACD (Moving Average Convergence Divergence) indicators. The MACD for the S&P 500 at 64.36, Nasdaq at 219.9, and Russell 2000 at 53.57 all suggest upward momentum in these markets. The Nasdaq is demonstrating the strongest bullish signal, with the highest MACD value, indicating significant positive momentum relative to the others. All three indices are currently not considered overbought or oversold, according to their respective RSI (Relative Strength Index) readings, which suggests that there is room for movement in either direction without immediate concern for a reversal due to extreme conditions.

Volume trends reveal that the Nasdaq is experiencing higher daily volumes compared to its longer-term average, while the S&P 500 and Russell 2000's volumes are slightly below their respective averages. Increased trading volume can be a sign of heightened investor interest and can sometimes precede price movement. In terms of price performance, all three indices are currently above their 52-week lows by significant margins (21% for S&P 500, 36% for Nasdaq, and 19% for Russell 2000), indicating a robust recovery from their lows.

In summary, while the general direction for the S&P 500, Nasdaq, and Russell 2000 is positive, the Nasdaq is showing a stronger bullish trend with a higher MACD value and trading volume above average. The S&P 500 and Russell 2000 are exhibiting moderate bullish signals with both indices under some accumulation. The Russell 2000 has the lowest MACD of the three, which might indicate a slower pace of growth, but it also has the highest percentage growth over the last three months, signaling a strong recent performance. Investors might consider these nuances when making decisions about asset allocation across these indices.

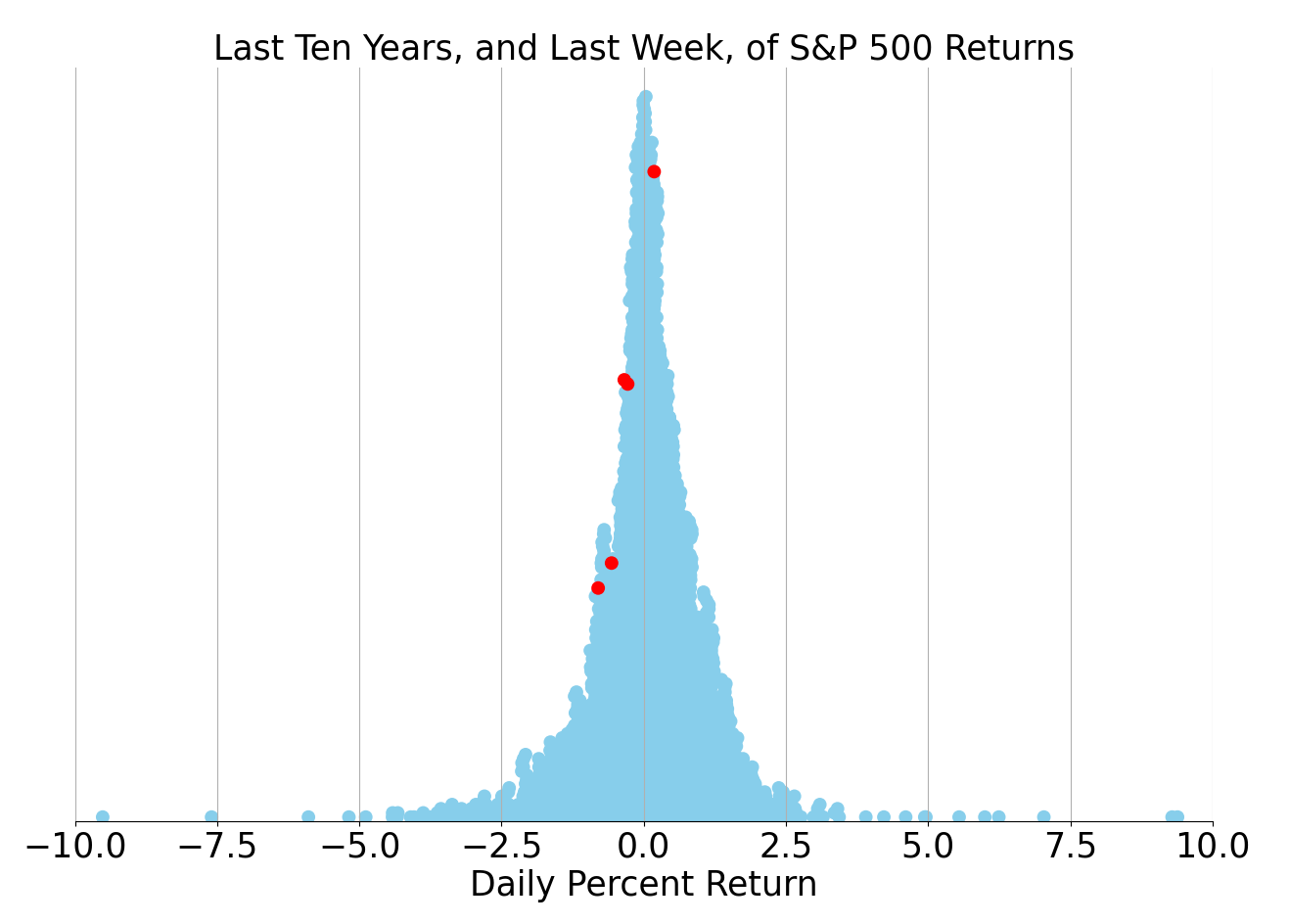

Last week vs. history (Large Cap S&P 500)

Market Commentary

Market Momentum Meets Caution: A Look at 2024's Financial Landscape

As we delve into the financial narrative of 2024, the market's robust rally witnessed in the closing chapters of 2023 has met a moment of moderation. The S&P 500, which enjoyed nine consecutive weeks of gains, experienced a slight retreat in the first week of the new year. This pause in the equity ascent is attributed to investors recalibrating their portfolios in the wake of a remarkable 16% surge in the index during the last two months of the previous year. While the market's optimism remains high, there is a sense of vulnerability that could be exposed by any unexpected economic disappointments.

The performance trajectory of 2024 is expected to be shaped by two pivotal forces: the Federal Reserve's interest rate decisions and the overall direction of the economy. The silver lining is the anticipation of a generally favorable environment, with a moderated inflation and continued economic growth—albeit at a slower pace. The labor market's resilience is underscored by the addition of 216,000 jobs in December, maintaining a stable unemployment rate of 3.7%. Despite this positive data, a gradual deceleration in job gains and a slight uptick in unemployment is projected, suggesting a more cautious consumer spending pattern, yet not indicative of a full-blown recession.

Wage growth, a critical component linking consumer spending and inflation, saw a modest increase in December. However, the broader employment trends suggest a potential moderation in wage increases throughout the year. This could ideally alleviate inflationary pressures while still bolstering consumer spending. The Federal Reserve's December meeting minutes revealed a consensus that interest rates are nearing their peak, with further hikes only likely should inflation unexpectedly surge. The market's anticipation of rate cuts could be premature, with the Fed adopting a cautious stance, potentially delaying cuts until mid-2024.

Historically, equity markets have responded favorably in the lead-up to the Fed's initial rate reduction, with mixed outcomes post-cut. However, in years where a recession was not on the horizon, stocks continued to thrive post-cut. While economic growth is expected to slow in the first half of 2024, a severe recession is not anticipated, suggesting that Fed rate cuts could support the continuation of the bull market.

Despite the market's tempered start to 2024, the historical correlation between January's performance and the rest of the year offers a glimmer of hope. In the past 30 years, a positive January often heralded a prosperous year for stocks. Conversely, a weak January start sometimes signaled a challenging year ahead. Nevertheless, the market's strong finish in December, with a 4.4% gain, suggests that a breather in January is not uncommon following a robust end-of-year rally.

As 2024 unfolds, the market is expected to navigate through a mix of headwinds and tailwinds. The Federal Reserve's policy decisions and economic indicators will be closely monitored for signs of stability or volatility. While the year's initial performance may not set the tone for the entire year, it provides valuable insights into the market's sentiment and trajectory. Investors are advised to stay informed, as the financial landscape of 2024 continues to evolve amidst a backdrop of cautious optimism and strategic anticipation.

Comments ()