The Monday Charge: January 29, 2024

As we delve into the financial landscape of 2024, the U.S. economy appears to be demonstrating robustness, with recent data suggesting a period of healthy expansion. The S&P manufacturing PMI, a critical measure of the health of the manufacturing sector...

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Large Cap S&P 500)

- Mailed to FREE newsletter subscribers (Covered on Tuesday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

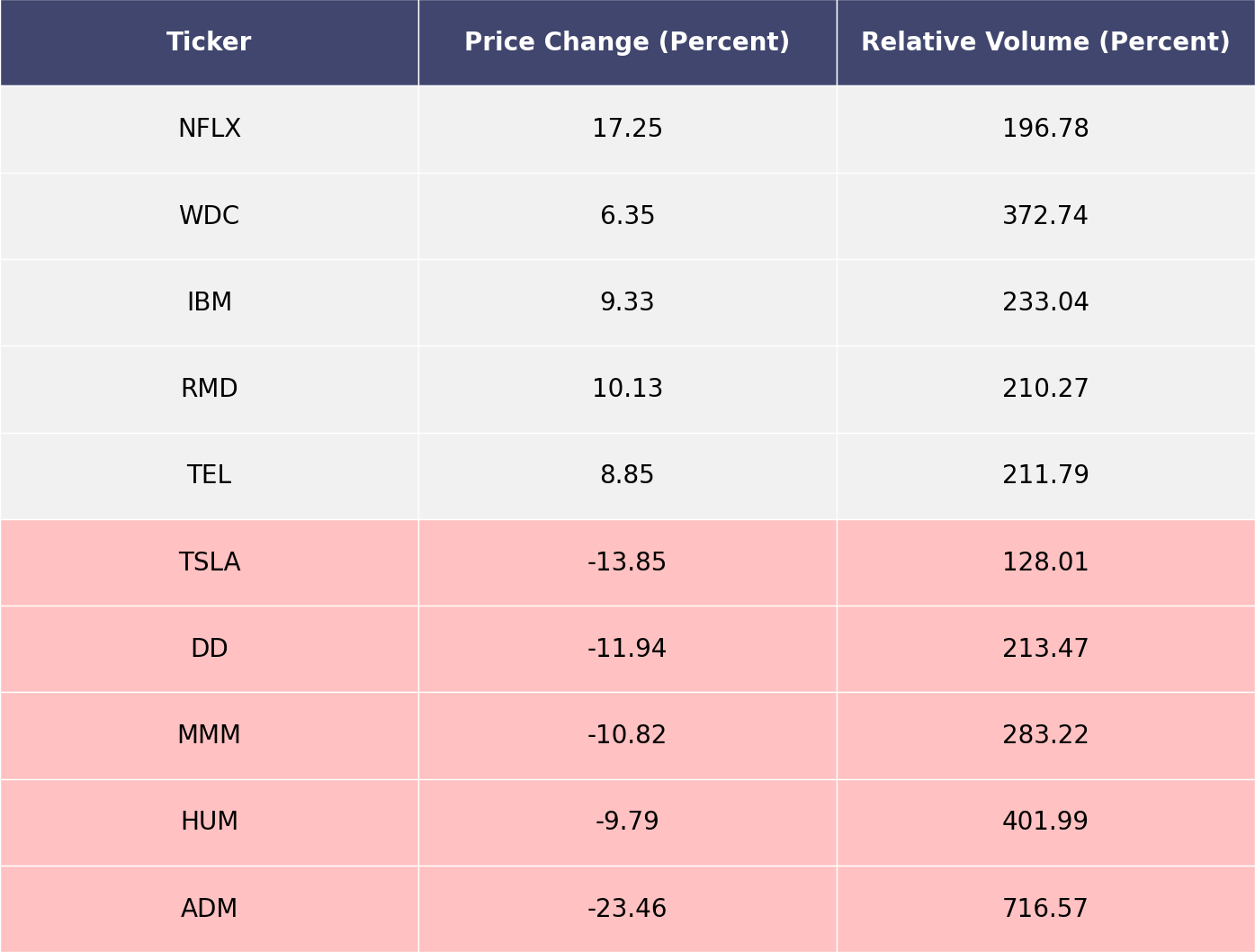

The biggest movers last week on price and volume (Large Cap S&P 500)

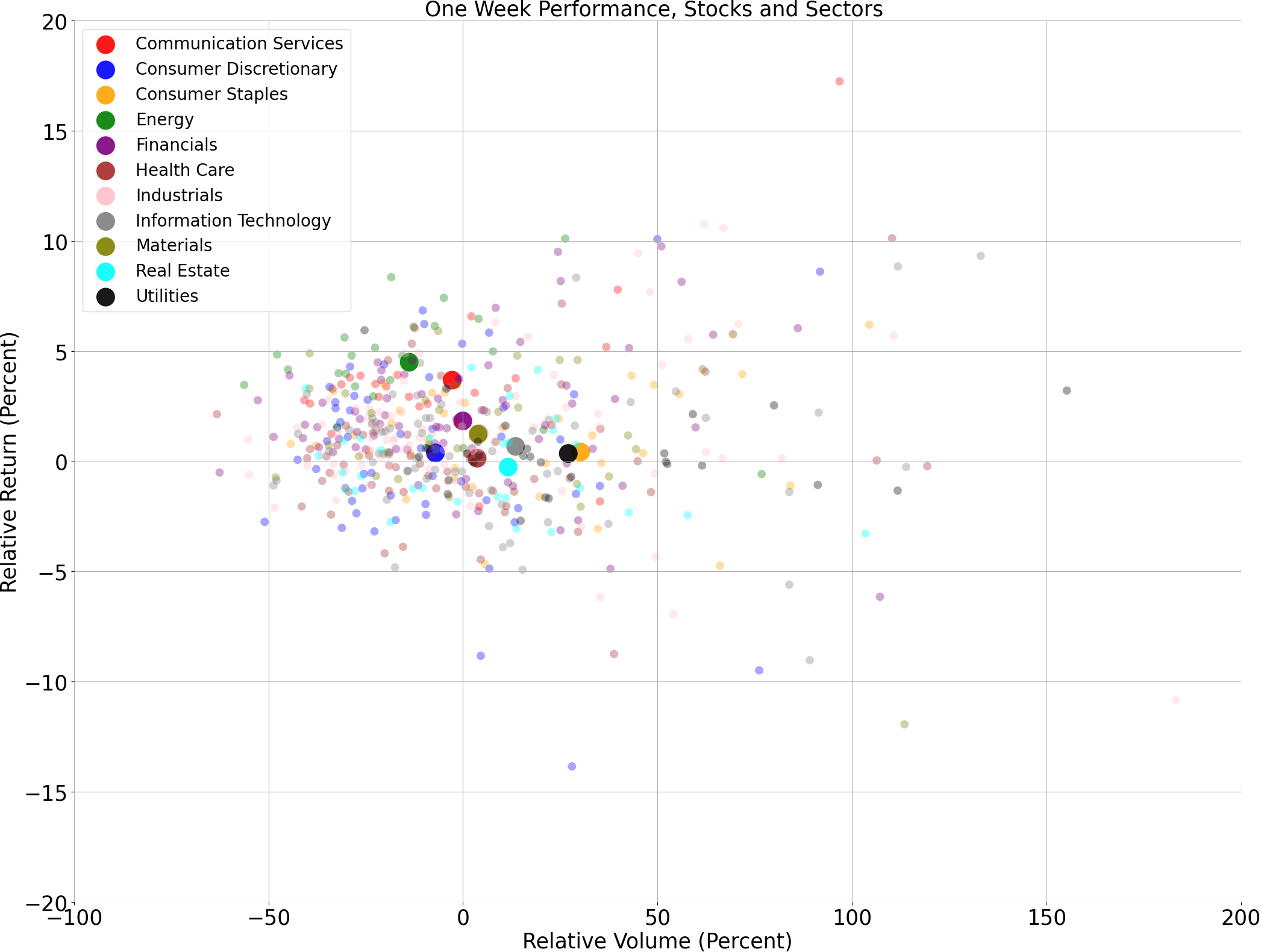

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

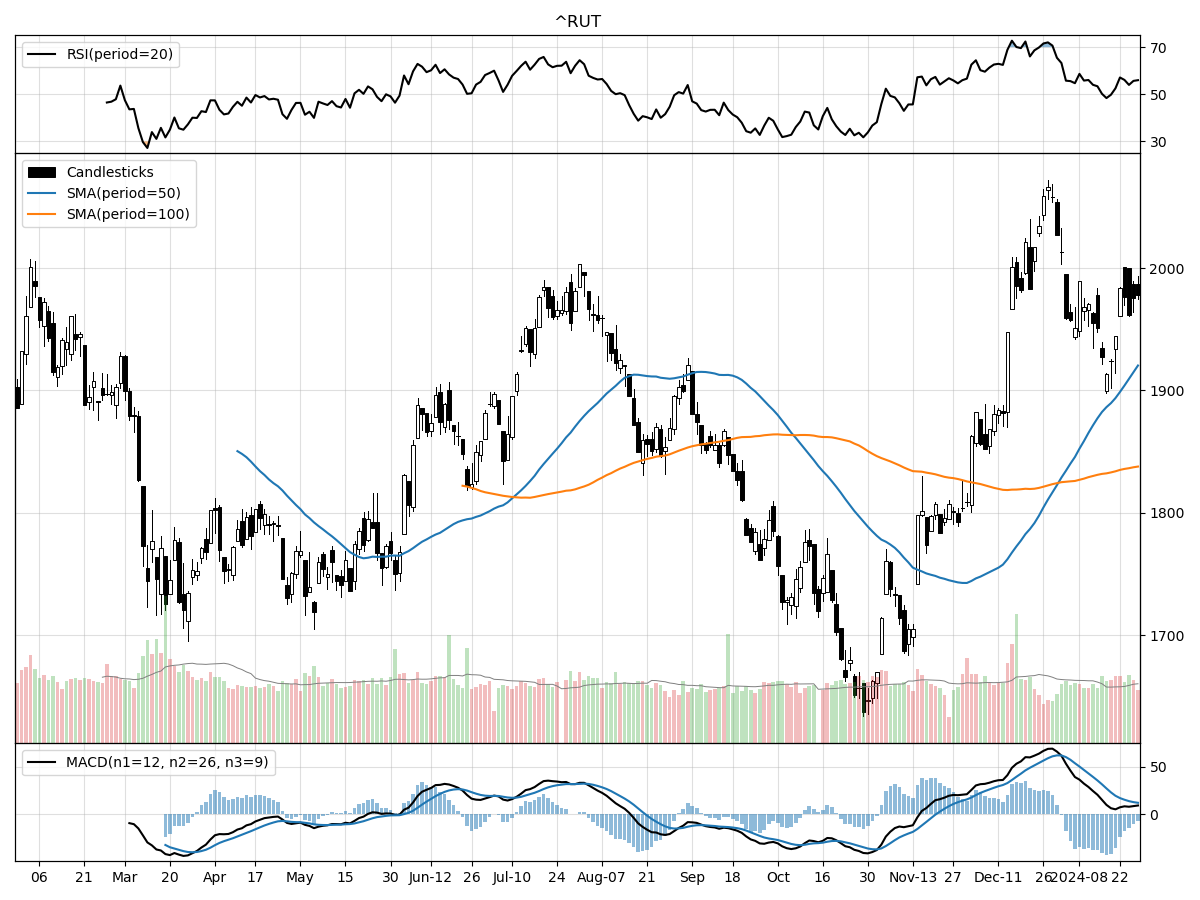

A technical analysis across indices

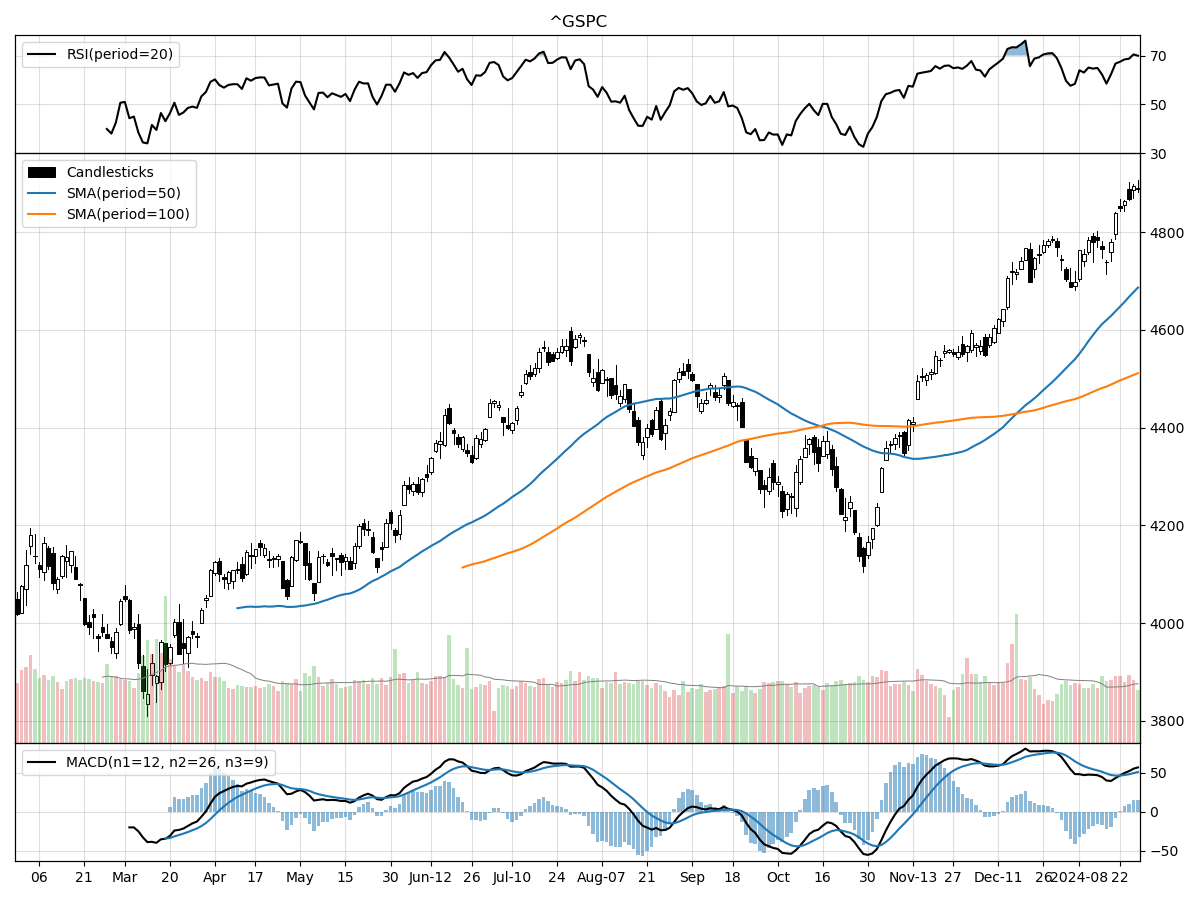

S&P500

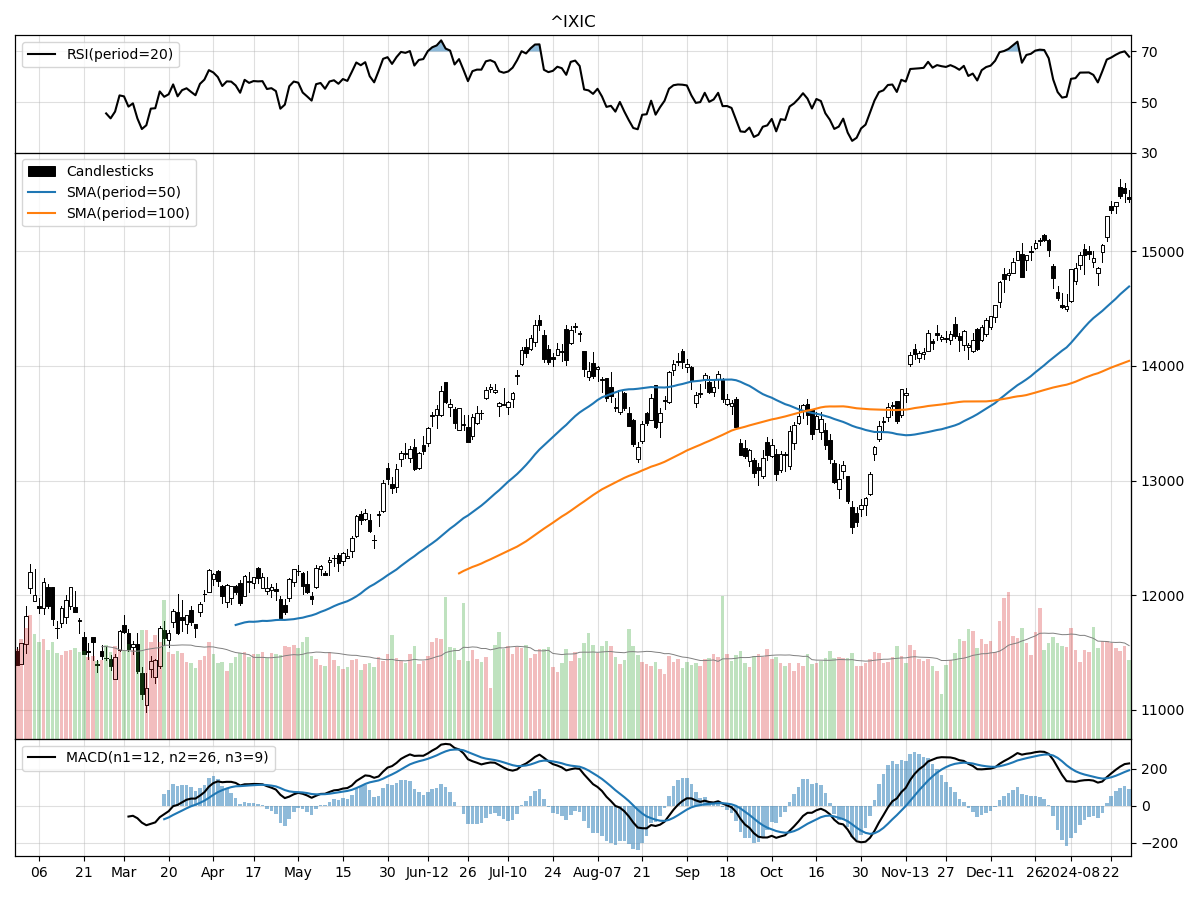

Nasdaq

Russell 2000

The S&P 500, NASDAQ, and Russell 2000 indices all have displayed bullish momentum in their recent performances, each rising significantly from their 52-week lows, with the NASDAQ showing the strongest rebound at 38% above its low. This suggests that large-cap, tech-focused stocks (which heavily influence the NASDAQ) have been particularly resilient or have benefited from specific market conditions more than the broader market and small-cap stocks. The S&P 500 and Russell 2000 are 26% and 20% above their 52-week lows respectively, indicating positive sentiment but to a lesser extent than the NASDAQ.

In terms of market activity, all three indices are experiencing varying degrees of buying pressure as indicated by Money Flow indicators. The S&P 500 is under "heavy" buying pressure, while the NASDAQ and Russell 2000 are under "moderate" buying pressure. This could reflect more aggressive accumulation in large-cap stocks compared to their smaller counterparts and tech-focused stocks. However, the Russell 2000 shows signs of distribution according to its money flow indicators, which could signal cautious or profit-taking behavior among investors in small-cap stocks.

The Relative Strength Index (RSI) suggests that stocks in all three indices are overbought, with the S&P 500 and NASDAQ being more pronounced in this regard. This is a sign that the recent price increases may have been steep and that there could be a potential for a pullback if investors start to feel that the market is overheating. The Moving Average Convergence Divergence (MACD) readings for all three are bullish, with the NASDAQ having a significantly higher value, which reinforces the strong upward momentum in tech-heavy stocks. The daily trading volumes are mixed, with the NASDAQ seeing a recent daily volume higher than its longer-term average, potentially indicating higher investor interest or speculative activity, while the S&P 500 and Russell 2000 are trading below their longer-term average volumes, perhaps suggesting a more cautious approach from investors in these markets.

Last week vs. history (Large Cap S&P 500)

Market Commentary

Navigating Early 2024: A Mosaic of Market Dynamics

Title: U.S. Economy Shows Resilience Amidst Inflation Moderation, Fed Rate Cuts on the Horizon

As we delve into the financial landscape of 2024, the U.S. economy appears to be demonstrating robustness, with recent data suggesting a period of healthy expansion. The S&P manufacturing PMI, a critical measure of the health of the manufacturing sector, has hit a high not seen since late 2022, signaling a resurgence in industrial activity. Concurrently, the real GDP and personal consumption figures have outperformed expectations, painting a picture of an economy with enduring consumer confidence and spending power.

The inflation narrative, which has dominated economic discourse in recent years, is showing signs of a welcome shift. The prices-charged index within the PMI report has descended to levels reminiscent of early pandemic days, indicating a softening of inflationary pressures. This trend is corroborated by the core PCE inflation data, the Federal Reserve's favored inflation gauge, which dipped below the 3% threshold for the first time since 2021. This moderation in core inflation is fueling optimism about potential easing of monetary policy.

Investors and analysts are now keenly anticipating the upcoming Federal Reserve meeting. While the market has priced in multiple rate cuts for the year, the Fed's more conservative "dot plot" suggests a more measured approach. The discrepancy between market expectations and the Fed's signaling could lead to a recalibration of forecasts, with the market currently split on the likelihood of a rate cut as soon as March.

The strategic direction of the Fed is crucial, as historical patterns suggest that markets tend to respond favorably to rate cuts outside of recessionary periods. Since 1990, the average 12-month return following the initial rate cut in a non-recessionary environment is significantly higher. Given the current economic indicators, the possibility of a 'soft landing' for the economy is emerging, which could spell positive outcomes for market returns as the Fed potentially shifts towards a rate-cutting cycle.

The market's performance last year, particularly the impressive rally of the S&P 500, was driven by a combination of technological advancements, particularly in AI, and an economy that remained resilient despite aggressive Fed rate hikes. However, it's worth noting that the rally was concentrated in a select group of stocks and sectors. Looking ahead, a more diversified market leadership is expected, with both equities and investment-grade bonds poised to benefit from a gradual rate reduction strategy by the Fed.

As we approach the end of January, the financial markets are bracing for a series of pivotal events that could shape investor sentiment. The Federal Reserve's policy meeting, along with a slew of mega-cap tech earnings reports and the release of the nonfarm payrolls report, are all on the horizon. These events are likely to inject volatility into the markets, with the potential for a "sell on the news" reaction to the tech earnings, given the sector's recent highs.

In conclusion, the U.S. economy's current trajectory, coupled with a moderation in inflation, presents a cautiously optimistic outlook. The Federal Reserve's upcoming decisions will be instrumental in either reinforcing this sentiment or altering the course. Investors may therefore find themselves at a crossroads, where strategic positioning and a keen eye on central bank cues will be essential for navigating the financial markets in 2024.

Comments ()