The Monday Charge: January 15 2024

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Large Cap S&P 500)

- Mailed to FREE newsletter subscribers (Covered on Tuesday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

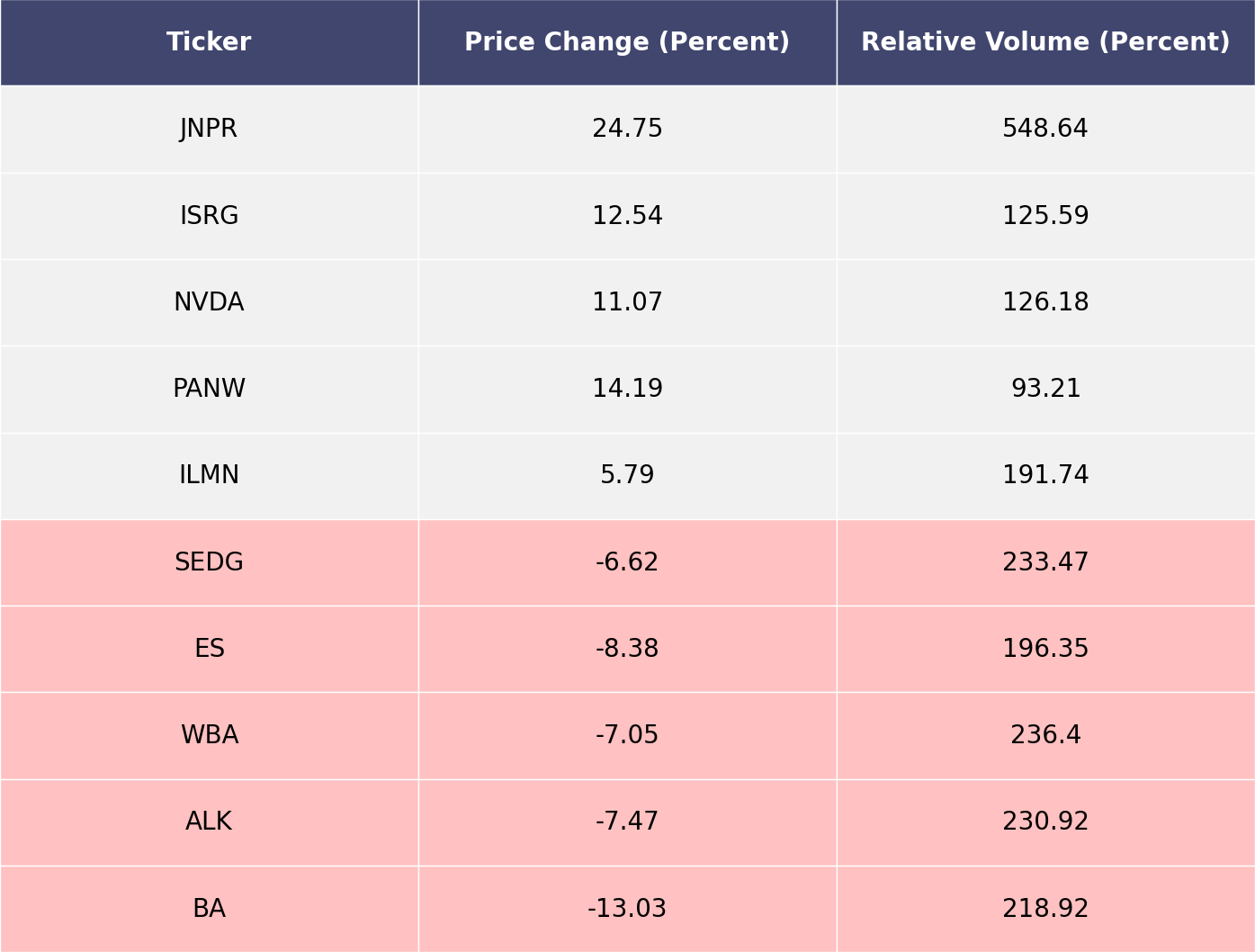

The biggest movers last week on price and volume (Large Cap S&P 500)

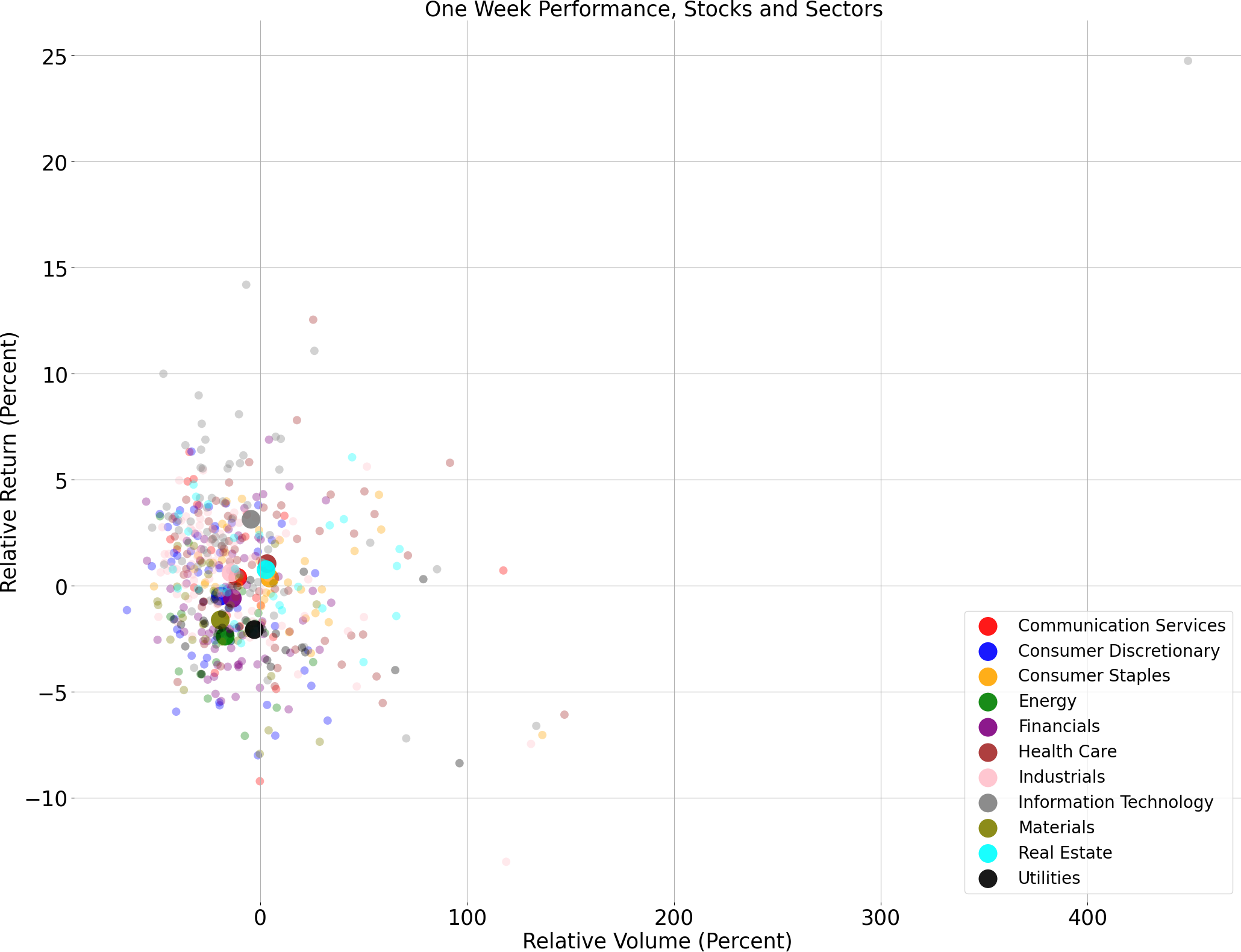

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

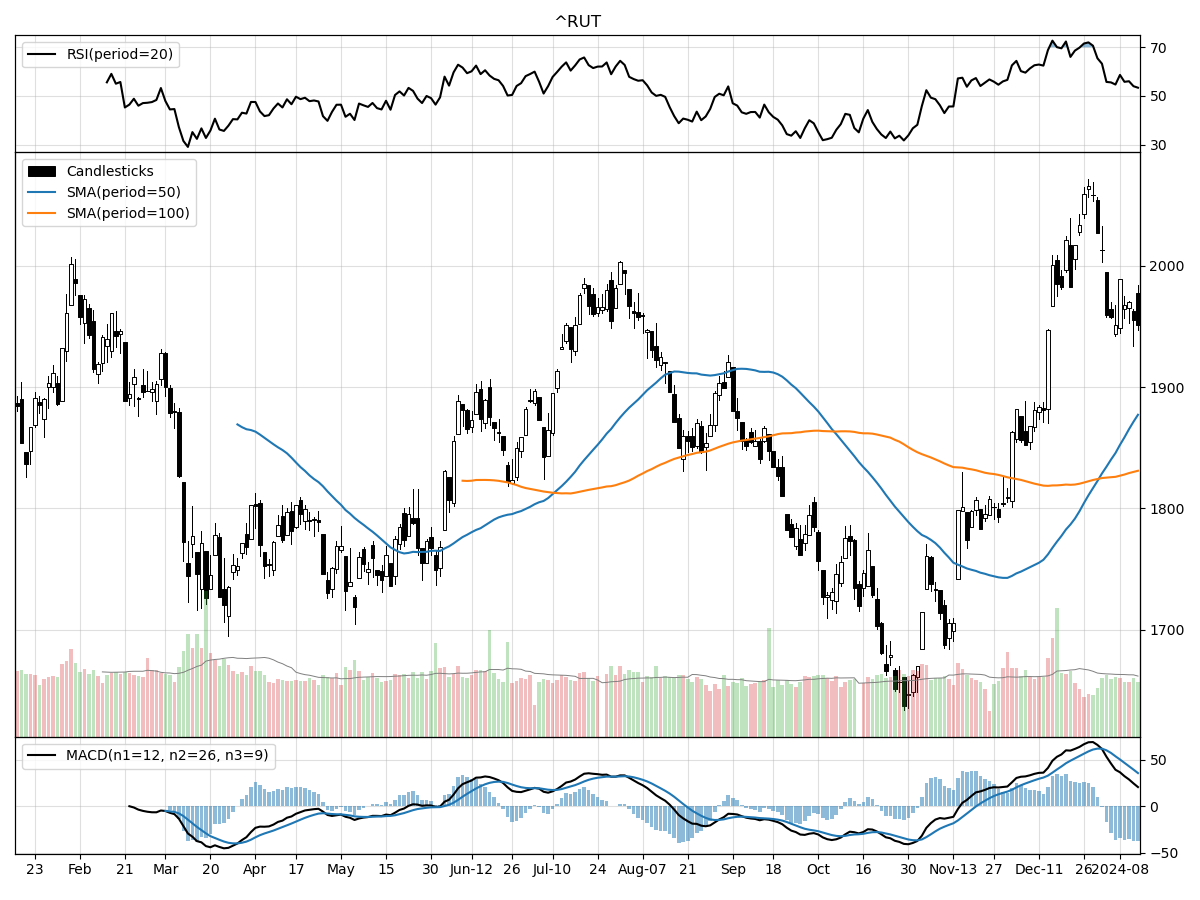

A technical analysis across indices

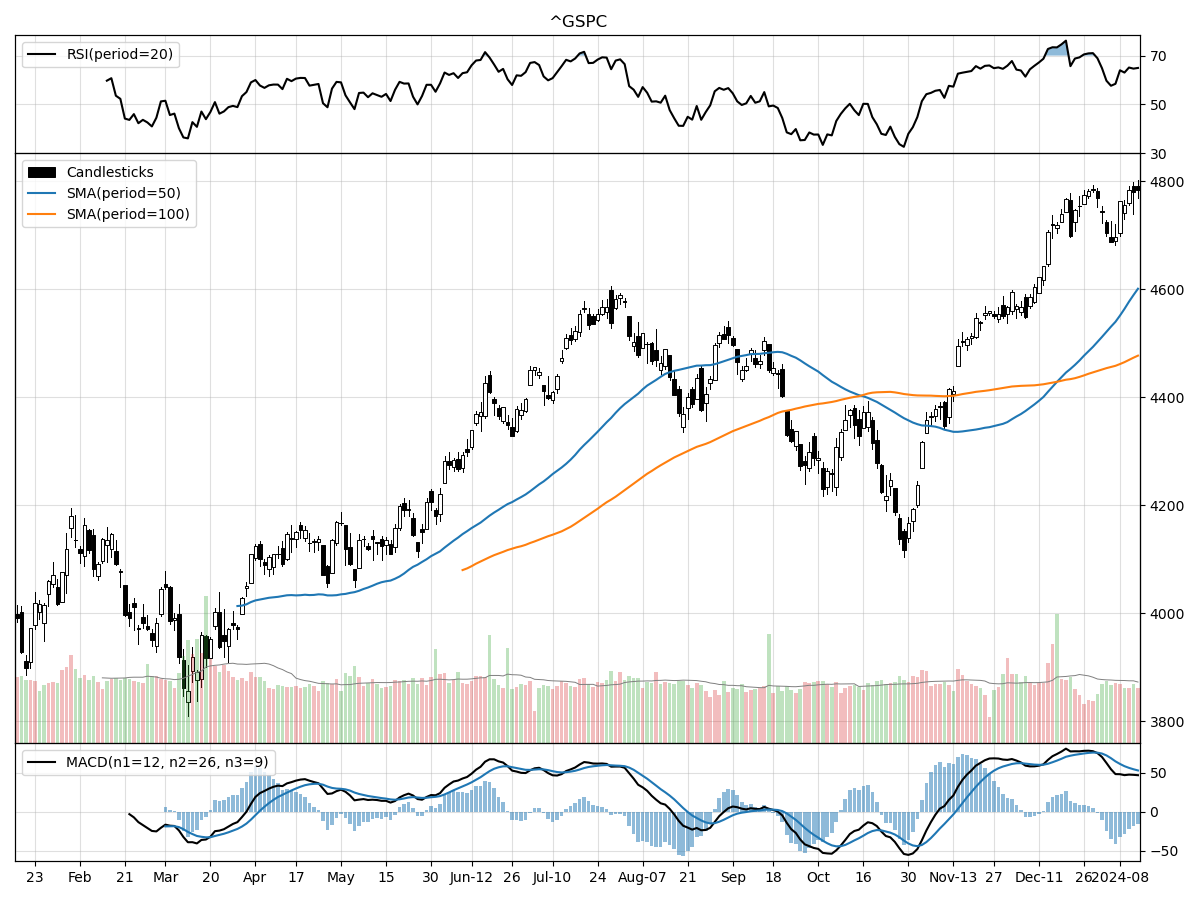

S&P500

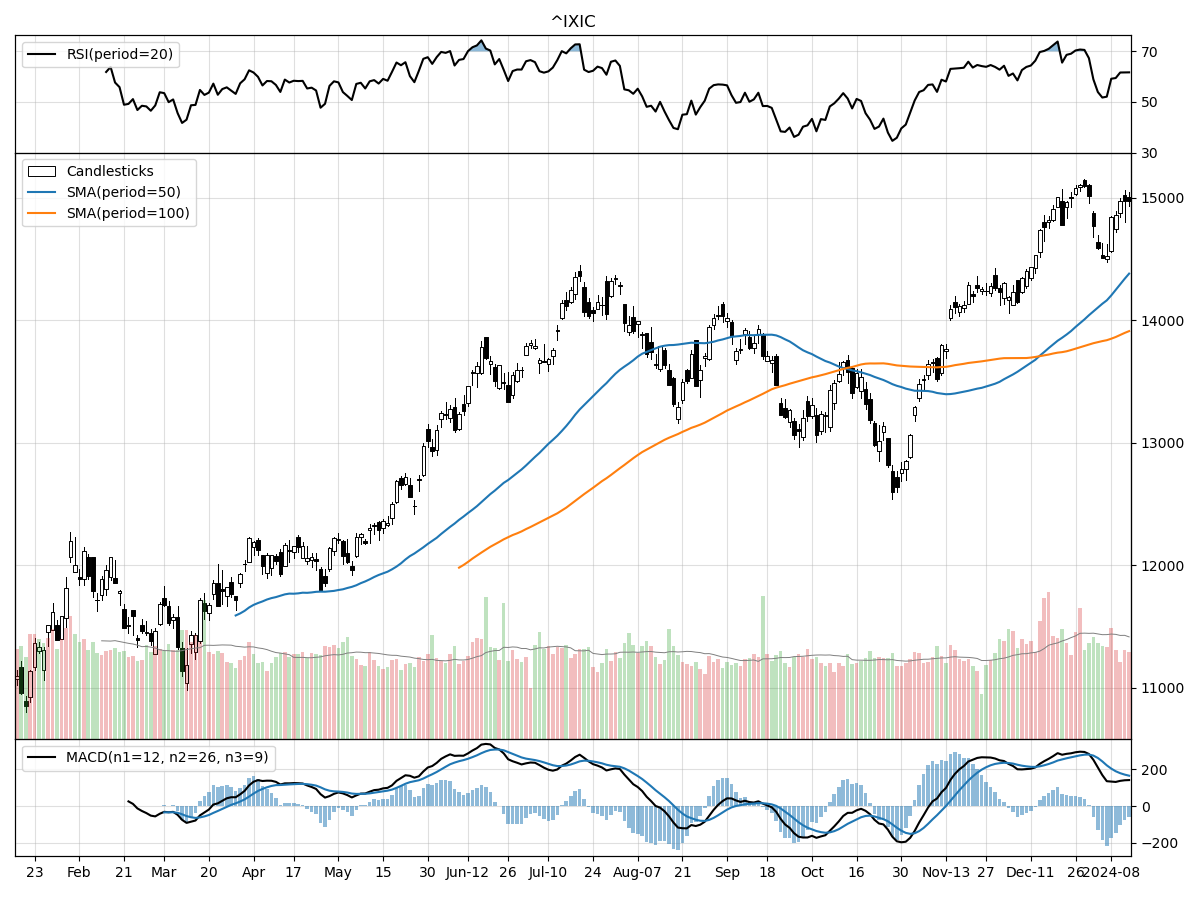

Nasdaq

Russell 2000

The S&P 500, Nasdaq, and Russell 2000 indices have all shown positive momentum over the last three months, with increases of 10.88%, 12.46%, and 12.85% respectively, suggesting a robust rebound in the broader market. However, there are subtle differences in their current technical positions. The S&P 500 and Nasdaq are currently at their 52-week highs, indicating strong bullish sentiment in large-cap and technology sectors. In contrast, the Russell 2000, which represents small-cap stocks, is trading 5% below its 52-week high, suggesting a slightly more cautious approach among investors towards smaller companies, possibly due to perceived risks or the expectation of a slower recovery in this market segment.

Volume analysis across the indices shows that recent daily volumes for the S&P 500 and Russell 2000 are slightly below their longer-term averages, while the Nasdaq's daily volume is significantly above its longer-term average. This suggests that there might be more investor interest in the tech-heavy Nasdaq stocks, potentially driven by specific sector-related catalysts or a more substantial appetite for growth stocks among investors.

Money flow and momentum indicators show moderate buying pressure for the S&P 500 and Nasdaq, with both indices seeing accumulation, which is reinforced by their bullish MACD readings of 52.74 and 164.0, respectively. The Russell 2000, however, exhibits moderate selling pressure and is under distribution, but still maintains a bullish MACD at 35.51. This divergence could imply that while investors are generally optimistic about the market, there is more caution in the small-cap space, which may be subject to more volatility and sensitivity to market shifts. Notably, the RSI indicates that all three indices are modestly overbought, which could signal a potential upcoming consolidation or pullback as the market digests the recent gains.

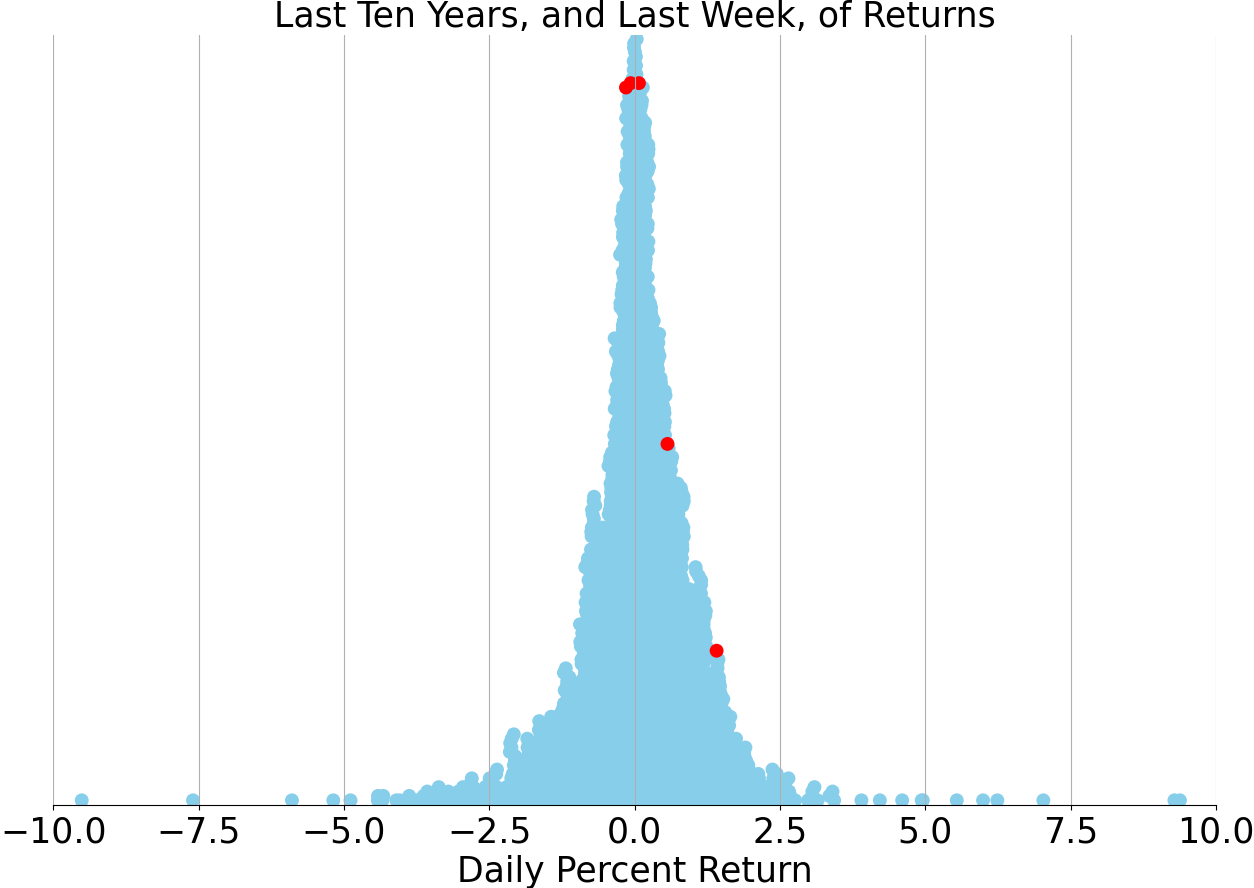

Last week vs. history (Large Cap S&P 500)

Market Commentary

Title: Navigating Choppy Waters: Insights into Market Volatility and Economic Indicators

As we forge ahead into 2024, the financial markets continue to be dominated by discussions around inflation and the Federal Reserve's monetary policy. The first week of trading has already given us a taste of what's to come, with fresh data on consumer prices stirring the pot of rate hike expectations and market volatility.

Inflation, as measured by the Consumer Price Index (CPI), has been a focal point for investors, with the latest figures prompting a debate over the Federal Reserve's next move. While the CPI data showed a slight uptick, indicating persistent inflationary pressures, the Zillow rent index suggested a potential cooling in rent inflation, which could lead to more favorable readings in the coming months. It's important to note, however, that past performance is not a reliable indicator of future results.

Shipping costs, as tracked by the World Container Index, have seen an increase due to recent geopolitical tensions in the Red Sea. Such fluctuations in shipping rates can have ripple effects across global trade and commodity markets, underscoring the interconnected nature of today's economic landscape.

The relationship between headline CPI and the Federal Reserve's policy rate remains a key area of focus. With the central bank's 2% inflation target as a backdrop, the tug-of-war between market expectations and the Fed's guidance continues to play out in real time. Investors are closely watching for signs of a shift in the Fed's stance, particularly as they weigh the prospects of a rate cut later in the year.

Corporate earnings, as always, are a barometer for the health of the economy. The forward 12-month earnings estimates for the S&P 500 are being scrutinized for signs of resilience or weakness in the corporate sector. As the market navigates through these uncertain times, the time it takes for the S&P 500 to enter a bear market after reaching new highs is being closely monitored.

The upcoming week promises to shed more light on the state of the economy with key data releases on retail sales, housing starts, and building permits. These indicators will provide further clarity on consumer behavior and the housing market's momentum, both of which are critical components of overall economic health.

In summary, the financial markets are at a crossroads, with inflationary concerns and central bank policies at the heart of the conversation. As investors digest the latest economic data and anticipate future rate moves, the importance of a well-considered investment strategy becomes ever more apparent. With potential choppiness ahead, a keen eye on market indicators and a diversified portfolio may be the prudent course for weathering the uncertainty that lies ahead.

Comments ()