The Monday Charge: January 22, 2024

After a robust rally in the closing months of 2023, where the S&P 500 soared by an impressive 15% from late October to December, investors have been navigating through a more subdued and somewhat uneven terrain in the early weeks of the new year.

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

AI stock picks for the week (Large Cap S&P 500)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers (Covered on Tuesday)

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

- Mailed to FREE newsletter subscribers

(Based on a three month forward looking window)

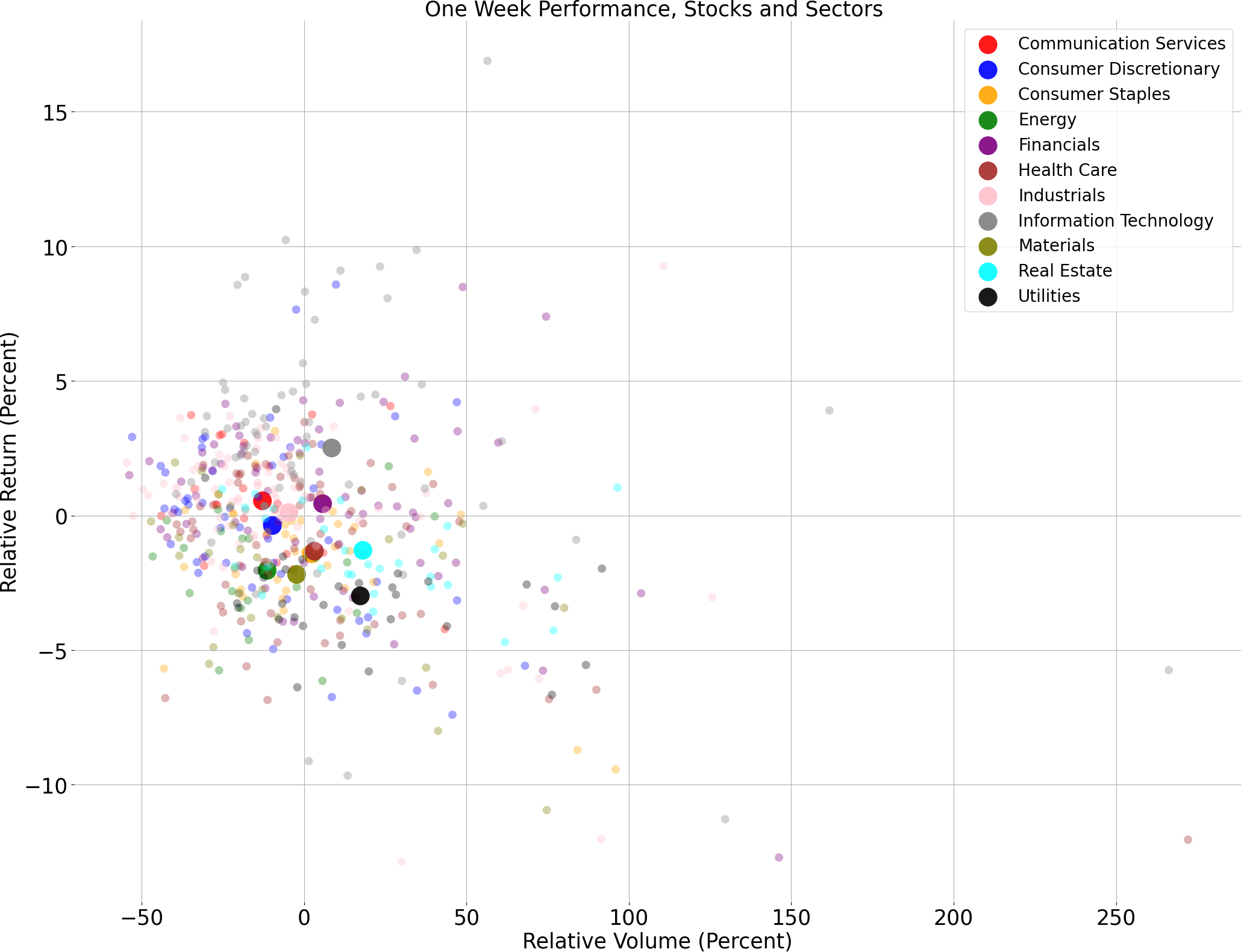

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

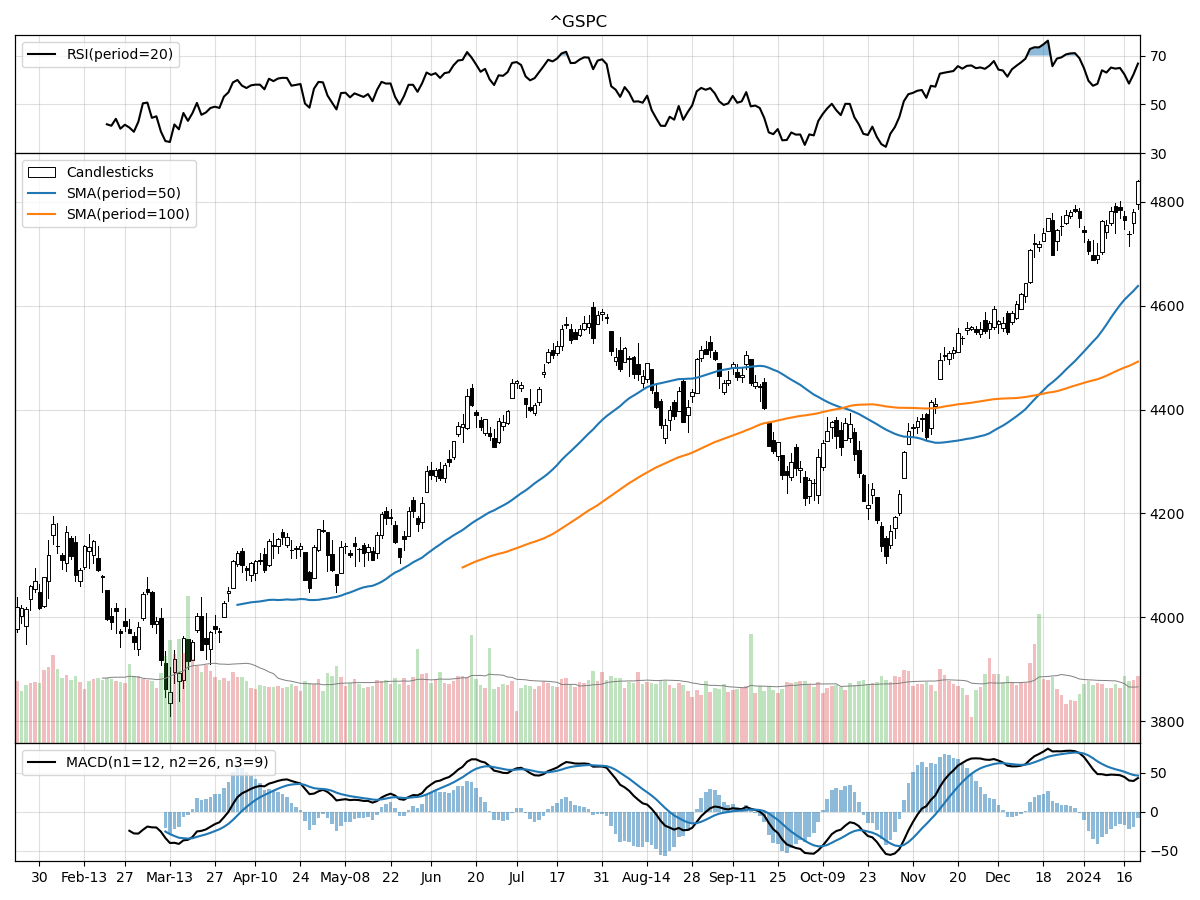

S&P500

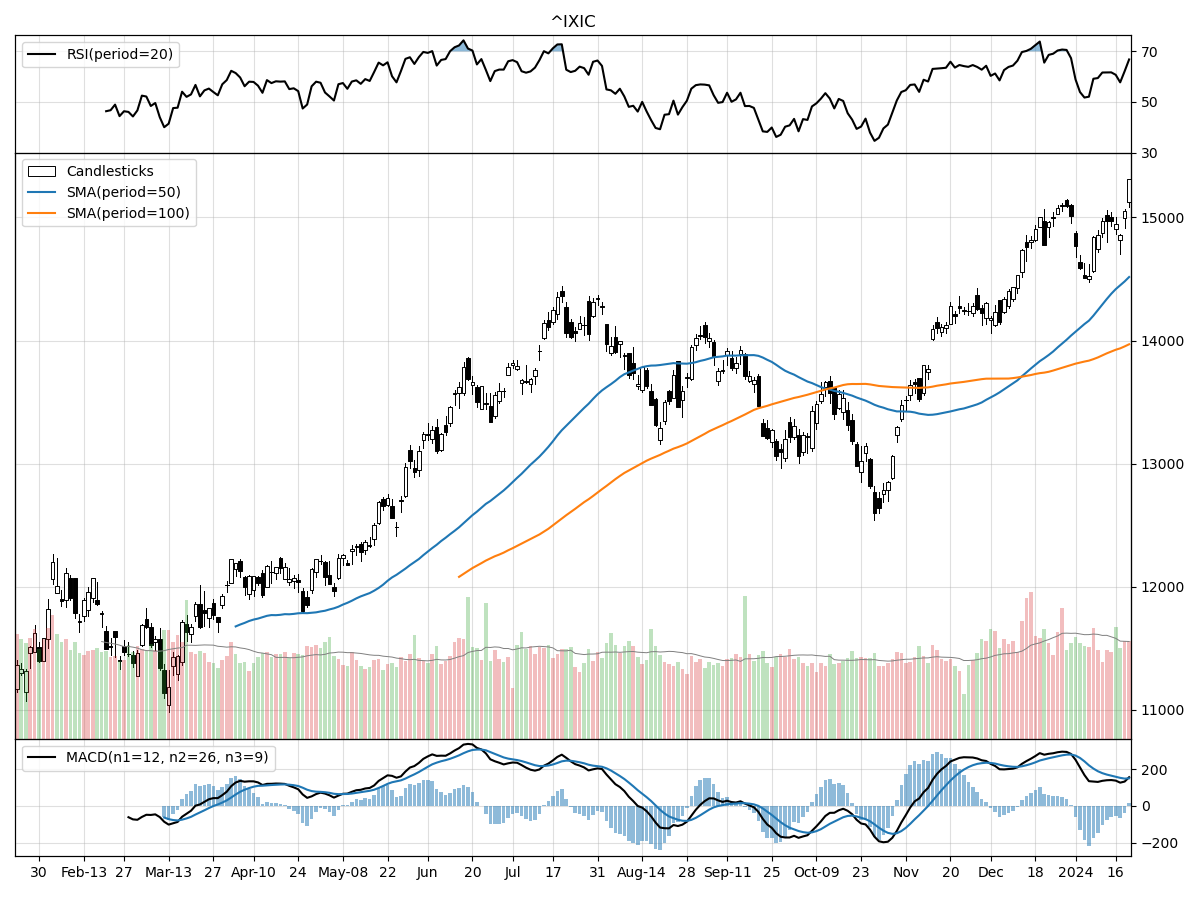

Nasdaq

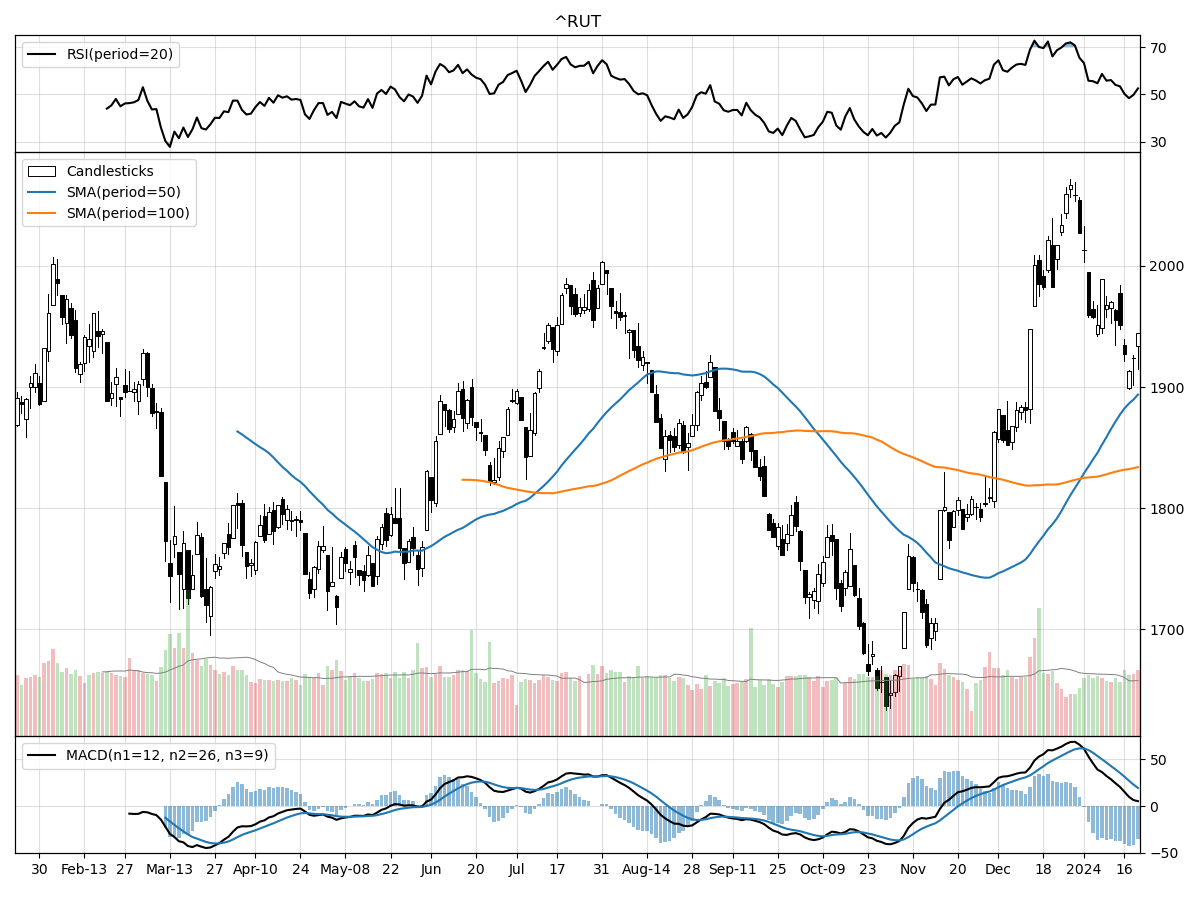

Russell 2000

Upon reviewing the technical performances of the S&P 500, Nasdaq, and Russell 2000 Small Cap indices, there are discernible variances and similarities that can inform an investment strategy. All three indices have experienced significant growth over the last three months, with the Nasdaq leading at a 16.52% increase, followed closely by the Russell 2000 at 15.77%, and the S&P 500 at 13.94%. This growth trajectory suggests a positive momentum across large-cap, tech-heavy, and small-cap stocks, indicative of a robust market sentiment.

In terms of their current positioning relative to their 52-week highs and lows, the Nasdaq is performing exceptionally well, trading at its 52-week high, which indicates strong investor confidence particularly in the technology sector that dominates this index. The S&P 500 is also at its 52-week high, reflecting a broad market strength across the diverse large-cap companies it represents. The Russell 2000, however, remains 5% below its 52-week high, suggesting there might be room for further growth or a potential undervaluation of small-cap stocks relative to their larger counterparts.

When looking at technical indicators, all indices show signs of accumulation, which means investors are generally buying more than selling, a bullish sign. The MACD (Moving Average Convergence Divergence) is bullish across all indices, with the Nasdaq exhibiting the highest value, reinforcing its strong upward momentum. However, the RSI (Relative Strength Index) points towards the S&P 500 and Nasdaq being modestly overbought, which could signal a near-term pullback or consolidation as markets digest recent gains. In contrast, the Russell 2000's RSI indicates a more balanced market without signs of being overbought or oversold, potentially offering a more stable investment opportunity at the moment. Overall, while all three indices are showing positive technical signs, there are nuances in their performances that could influence an investment strategy based on an investor's risk tolerance and market outlook.

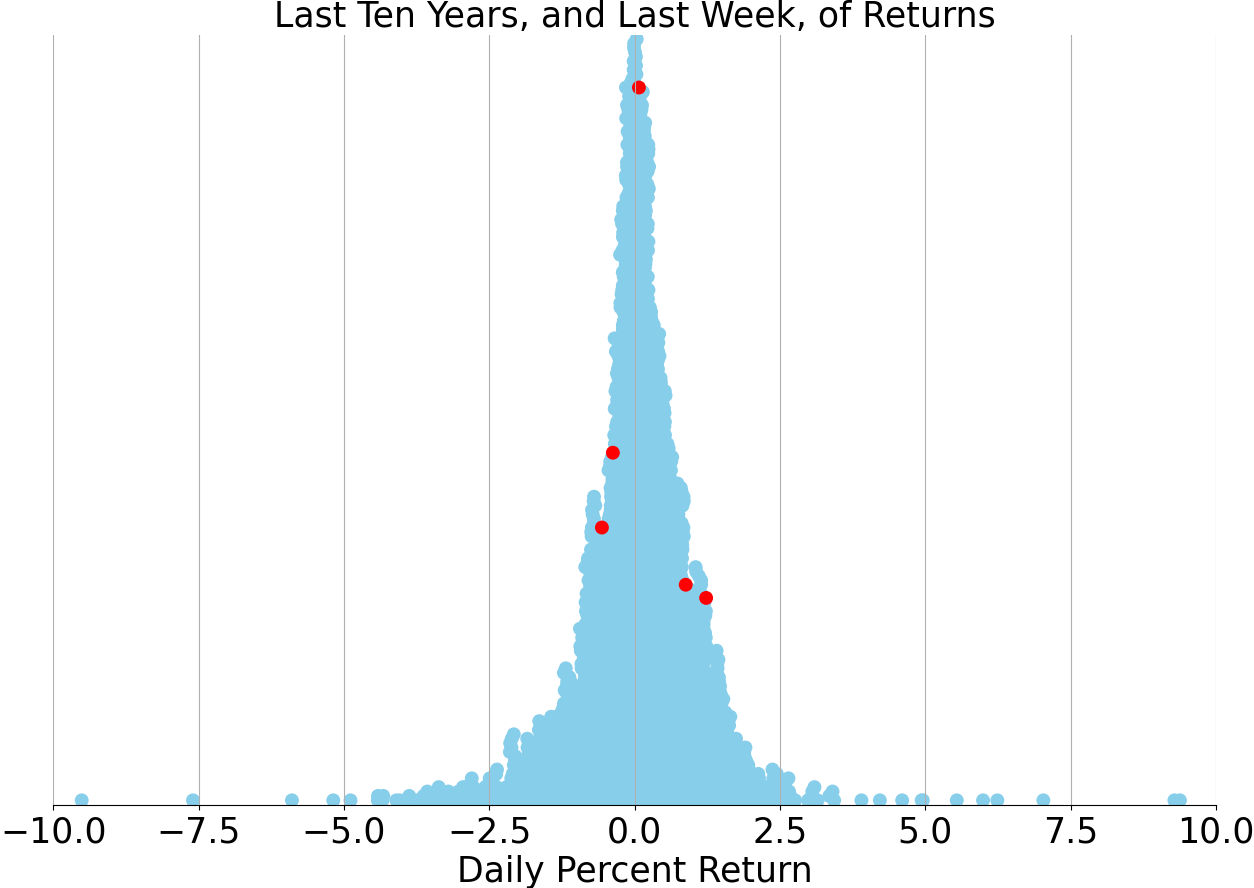

Last week vs. history (Large Cap S&P 500)

Market Commentary

Navigating Early 2024: A Mosaic of Market Dynamics

As we venture deeper into 2024, the financial markets present a kaleidoscope of evolving patterns, reflecting both the resilience and the underlying tensions that have come to define the current economic landscape. After a robust rally in the closing months of 2023, where the S&P 500 soared by an impressive 15% from late October to December, investors have been navigating through a more subdued and somewhat uneven terrain in the early weeks of the new year.

The initial days of 2024 have seen the S&P 500 eke out a modest gain of about 0.2%, suggesting a phase of consolidation that could be considered a healthy recalibration following the previous quarter's exuberance. Beneath the surface, however, the market's complexion is more nuanced. Sectors such as small-cap stocks and investment-grade bonds, which had previously shown signs of vitality, are now facing a bout of pressure. Conversely, technology and communication services continue to lead the charge, with defensive sectors like healthcare and consumer staples also outpacing expectations.

The adage "as goes January, so goes the year" has often been bandied about in investment circles, suggesting that a negative January forebodes a dismal annual performance. Yet, historical data since 1990 paint a different picture: out of 15 instances of a downbeat January for the S&P 500, only six years continued to tread in negative territory. This statistic serves to remind investors that a turbulent January does not necessarily set the tone for the remainder of the year.

A closer examination of the final weeks of January reveals several key data points that could offer deeper insights into the fundamental drivers shaping the markets and the broader economy. Among these are the anticipated slowdown in U.S. real GDP and consumption growth, with expectations for a rebound in the latter half of 2024. Furthermore, the Federal Reserve's interest rate policy remains a focal point, with the probability of a March rate cut having declined from over 70% to just above 50%.

Despite the potential for increased volatility, particularly as the Fed may resist market expectations for imminent rate cuts, the early-year market fluctuations are being viewed by some strategists as an opportunity to recalibrate investment portfolios. This could involve rebalancing and diversifying, as well as incorporating high-quality investments that may have been overlooked during the rapid rally at the end of the previous year.

The overarching narrative for 2024 is likely to be shaped by a triad of economic growth, inflation moderation, and the trajectory of Federal Reserve policies. With inflation expected to ease and the Fed potentially reducing rates, the economy could witness a resurgence. However, with the 10-year Treasury yield having crested above 4.0%, investors should brace for a bumpy ride in the short term.

In conclusion, while the start of 2024 has been marked by a degree of volatility and uncertainty, the underlying fundamentals suggest that there may be smoother sailing ahead for those who navigate these choppy waters with a strategic and measured approach. The themes of broader stock market leadership and improved performance from investment-grade bonds are anticipated to unfold throughout the year, offering potential opportunities for discerning investors.

Comments ()