The Monday Charge: August 5, 2024

In a stark departure from the typical summer lull, the final week of July saw the markets in a frenzy, driven by a deluge of earnings reports, central-bank meetings, and pivotal labor-market data.

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

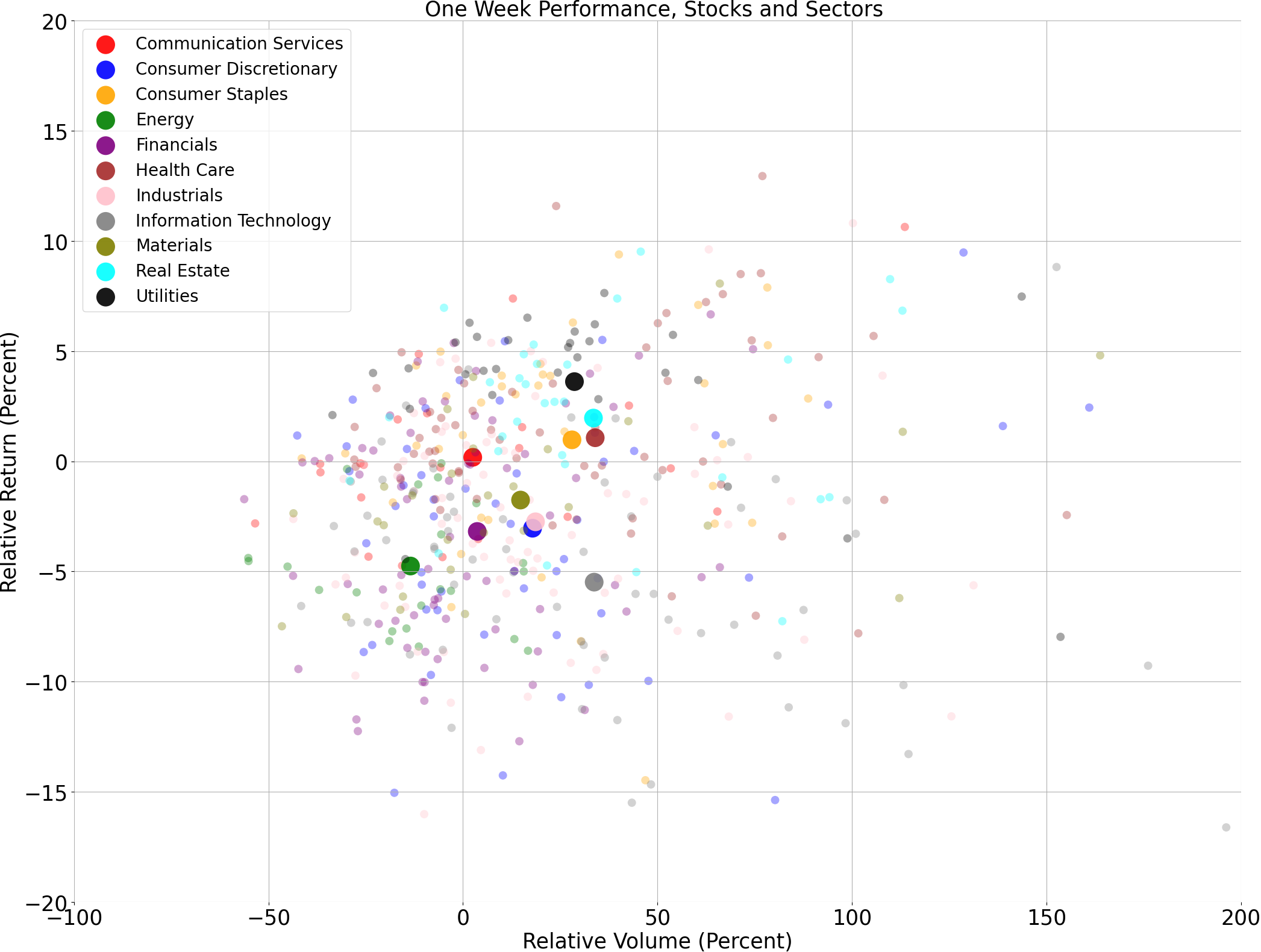

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

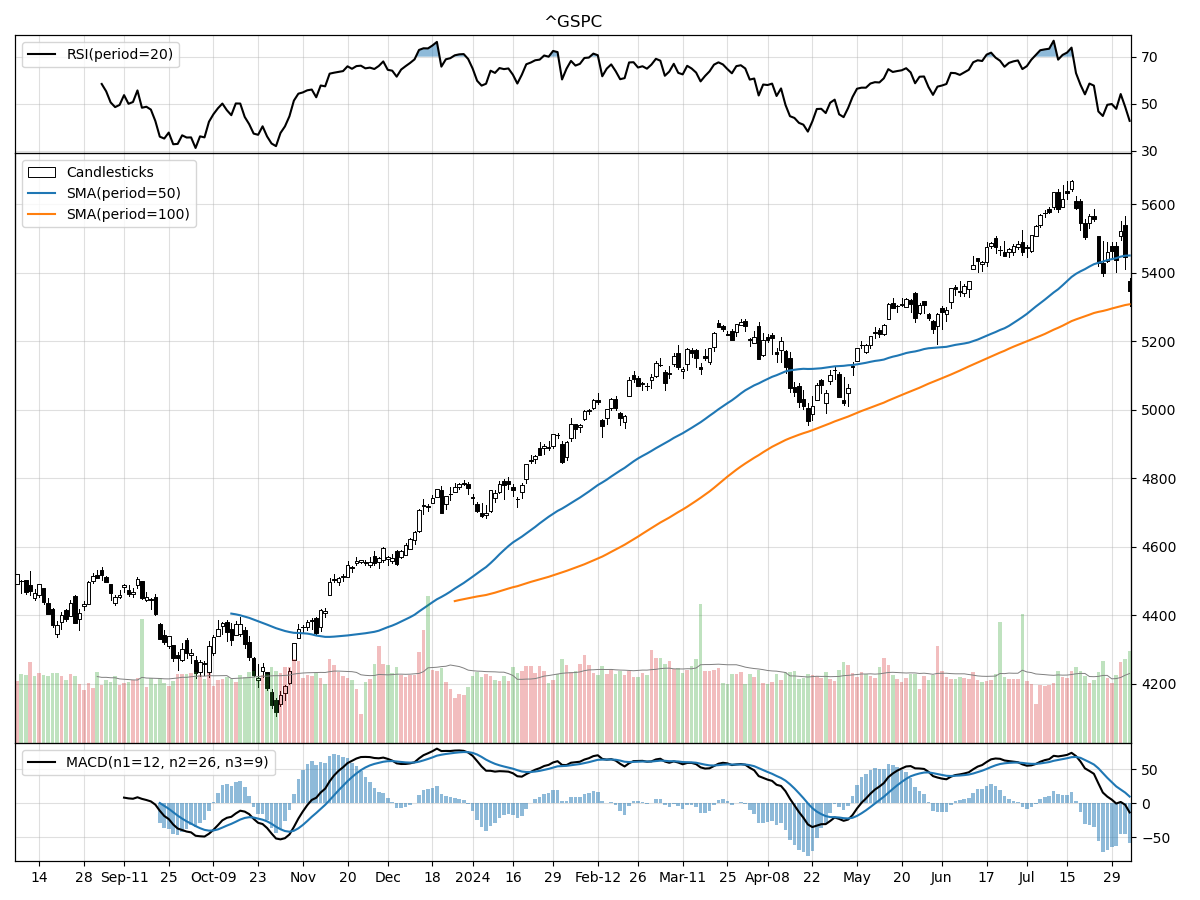

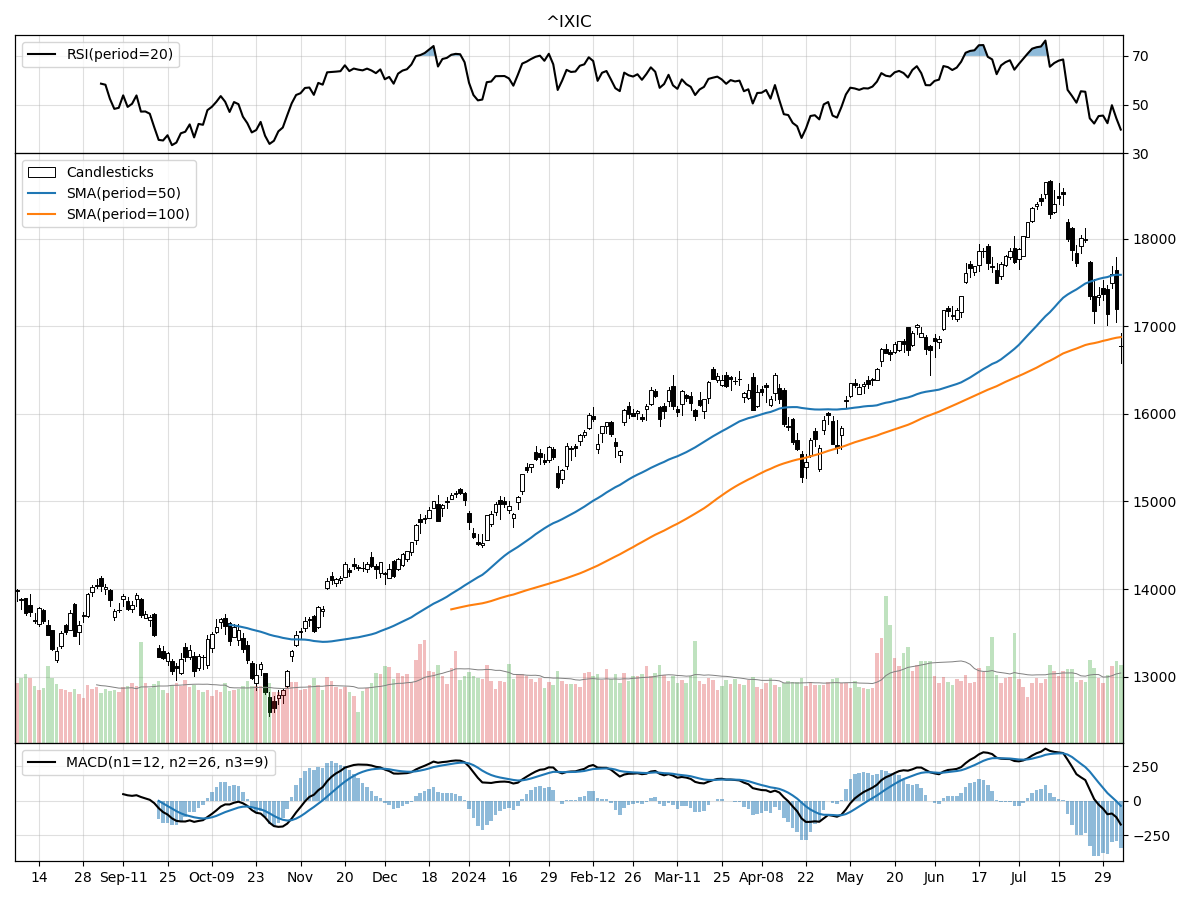

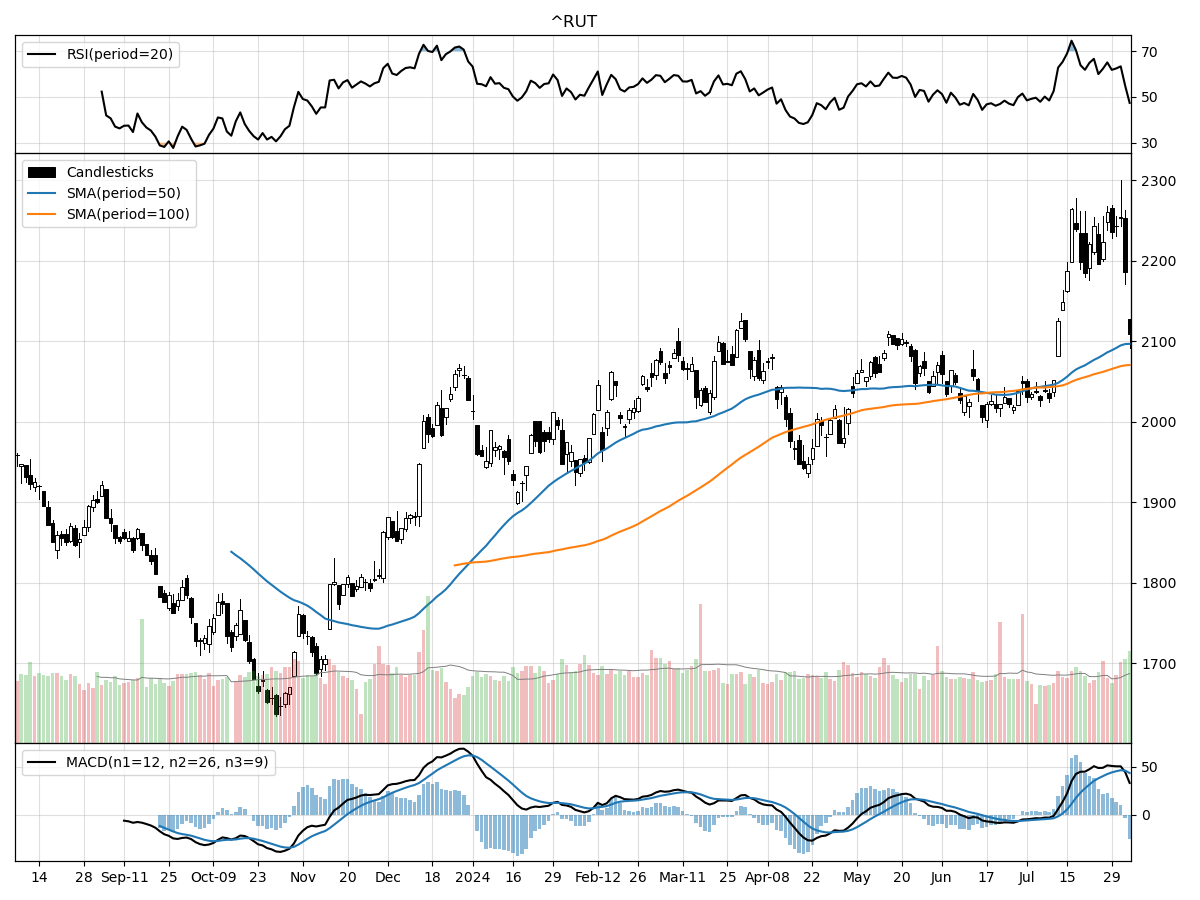

A technical analysis across indices

S&P500

Nasdaq

Russell 2000

The technical performances of the S&P 500, Nasdaq, and Russell 2000 indices present a mixed picture, with each index exhibiting unique characteristics and trends. The S&P 500 is currently priced at 5346.56, which is 29% above its 52-week low and 5% below its 52-week high. The index has remained relatively stable over the past month and three months, indicating a potential consolidation phase. Despite moderate selling pressure and distribution as indicated by money flow indicators, the MACD is bullish at 9.883, suggesting that the underlying trend could still be favorable, albeit with caution due to the selling pressure.

On the other hand, the Nasdaq index, trading at 16776.16, shows a more pronounced divergence in its technicals. The index is 33% above its 52-week low but remains 10% below its 52-week high. Unlike the S&P 500, the Nasdaq has experienced an 8.84% decline in the last month, reflecting a more significant short-term bearish sentiment. The MACD is bearish at -36.3, indicating downward momentum. This bearish outlook is further supported by moderate selling pressure and distribution, suggesting that the tech-heavy Nasdaq may face continued headwinds in the near term.

Finally, the Russell 2000 index, at 2109.31, sits 28% above its 52-week low and 6% below its 52-week high. Similar to the S&P 500, it has remained relatively stable over the past month and three months. However, the Russell 2000 stands out with a bullish MACD at 43.37, indicating a stronger positive momentum compared to the other indices. Despite this bullish signal, the index is also under moderate selling pressure and distribution, which implies that while there is potential for upward movement, investors should be cautious of the selling trends.

In summary, while the S&P 500 and Russell 2000 indices show relative stability with bullish MACD signals, the Nasdaq displays a bearish trend with significant short-term declines and a bearish MACD. Each index is under moderate selling pressure and distribution, highlighting a cautious market sentiment across the board.

Last week vs. history (Large Cap S&P 500)

Market Commentary

Market Turbulence Amid Earnings and Economic Data: A Summer Like No Other

In a stark departure from the typical summer lull, the final week of July saw the markets in a frenzy, driven by a deluge of earnings reports, central-bank meetings, and pivotal labor-market data. The Federal Reserve's decision to hold rates steady, coupled with Chair Jerome Powell's acknowledgment of growing labor market risks, added to the complexity. Despite corporate earnings surpassing expectations, stocks have been on a downward trajectory since the onset of the second-quarter earnings season. The market's concerns about economic growth have led to a reversal in the recent rotation into cyclical and small-cap stocks, while artificial intelligence (AI) favorites experienced their most significant pullback of the year.

The Federal Reserve's recent actions suggest a potential shift in monetary policy. After an aggressive tightening cycle and a prolonged pause, the Fed is signaling that an easing cycle might be imminent. Inflation has been the primary focus for the past two and a half years, but as the Fed nears its goal of stable prices, it is increasingly attentive to its mandate of maximum employment. The Fed's unchanged policy rate of 5.25% to 5.50% and the possibility of a September rate cut, as indicated by Powell, underscore this shift. With inflation trending below the Fed's year-end projection and unemployment surpassing forecasts, the labor market data may play an equally, if not more, significant role in shaping future Fed policy.

Labor market data from July painted a mixed picture, with the economy adding 114,000 jobs, falling short of the expected 175,000. The unemployment rate rose to 4.3%, and wage growth saw its smallest increase in over three years. While these figures suggest that the labor market is adjusting to slower economic growth, it's essential to view this data in context. The three-month average in nonfarm payrolls through July is now modestly below the monthly average from 2010 to 2019. Despite the recent slowdown, employment conditions remain relatively healthy.

The bond market has reacted to the Fed's hints at easing monetary policy, leading to a rally in bond prices and a drop in yields. The policy-sensitive two-year yield fell below 4.0% for the first time since May, while the ten-year yield dipped below 3.90%. This shift suggests that the market is pricing in a more aggressive easing cycle. Investors are advised to slightly overweight duration relative to an investment-grade bond benchmark, favoring intermediate and long-term bonds. With the Fed likely to embark on a rate-cutting cycle, now is an opportune time to consider the reinvestment risk of holding an overweight allocation to cash.

The tech sector, particularly the mega-cap stocks, faced scrutiny as four of the "Magnificent 7" reported earnings. Despite strong growth, the tech-heavy Nasdaq entered correction territory, down 10% from its peak. Investors are growing impatient for the heavy spending on AI to translate into returns. While AI is poised for rapid growth over the next five to ten years, there will likely be a timing gap between costs and benefits. Beyond tech, the broader earnings outlook remains positive, with S&P 500 earnings growth on track to accelerate from 6% in the first quarter to about 11% in the second.

Volatility has made a notable return in the second half of the year, with the VIX index, a proxy for stock-market fluctuations, showing significant intraday swings. Concerns about the Fed's timing on rate cuts and election-related uncertainties are potential catalysts for increased volatility. Historically, the period between August and October has been challenging for stocks, with lower returns and higher volatility. However, when stocks are in a strong uptrend, as they are this year, the negative seasonality tends to be less pronounced.

Despite the recent market turbulence, the fundamental outlook remains relatively positive. Inflation is moving closer to the Fed's target, providing room for the central bank to ease up on restrictive policies. The economy continues to expand, albeit at a slower pace, and corporate earnings are on the rise. While short-term pullbacks are uncomfortable, they present opportunities for investors to rebalance, diversify, and deploy fresh capital. The bull market, which began in October 2022, appears to have staying power, supported by improving productivity and rising forward earnings per share of the S&P 500.

In conclusion, the final week of July has been anything but typical for the markets. The interplay between corporate earnings, central bank policies, and labor market data has created a complex landscape for investors. While volatility and short-term pullbacks are likely, the overall economic and earnings outlook remains positive. Investors are encouraged to stay diversified and take advantage of opportunities presented by market fluctuations. As the Fed navigates its dual mandate of stable prices and maximum employment, the coming months will be crucial in determining the market's trajectory.

Stock study for Tuesday

Robert Half Inc. (RHI) operates in specialized talent solutions and consulting services through its Robert Half and Protiviti brands, covering finance, technology, marketing, legal, and administrative support sectors. Founded in 1948, the company transitioned from a franchise model to owning its locations in 1986, enhancing operational control and uniformity. In 2022, Robert Half streamlined its various branded divisions to improve market presence and brand awareness. The company provides contract and permanent placement talent solutions, charging clients a fixed hourly rate for contract workers and a placement fee for permanent hires. Its subsidiary, Protiviti, established in 2002, offers consulting services and leverages AI to enhance talent matching and lead generation, positioning AI-enabled solutions as a future growth driver.

Comments ()