The Monday Charge: August 26, 2024

n the world of finance, last week's Federal Reserve symposium in Jackson Hole, Wyoming, served as a critical juncture for monetary policy observers. The annual event, often likened to a monetary-policy red carpet, provided no formal policy decisions but offered valuable insights...

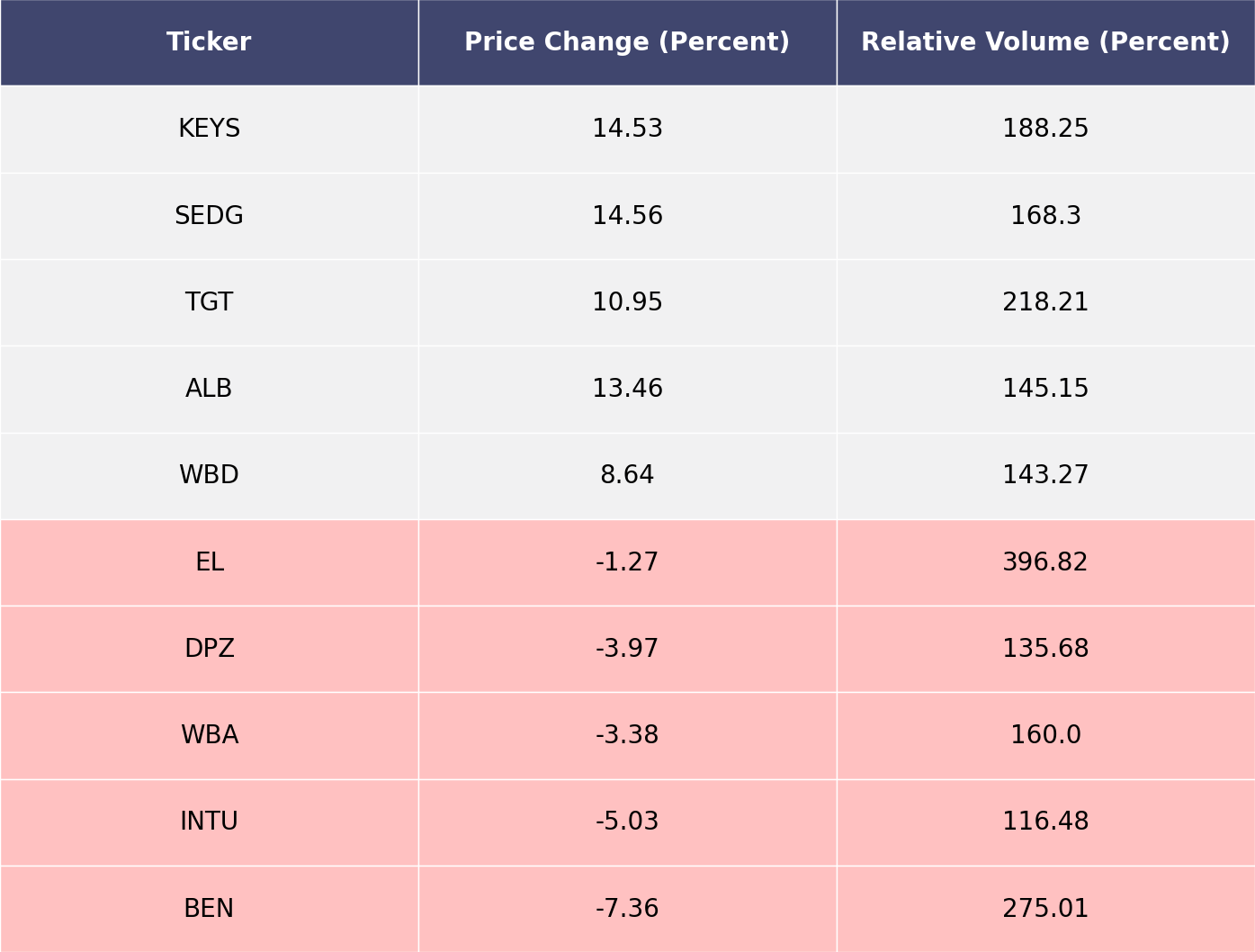

The biggest movers last week on price and volume (Large Cap S&P 500)

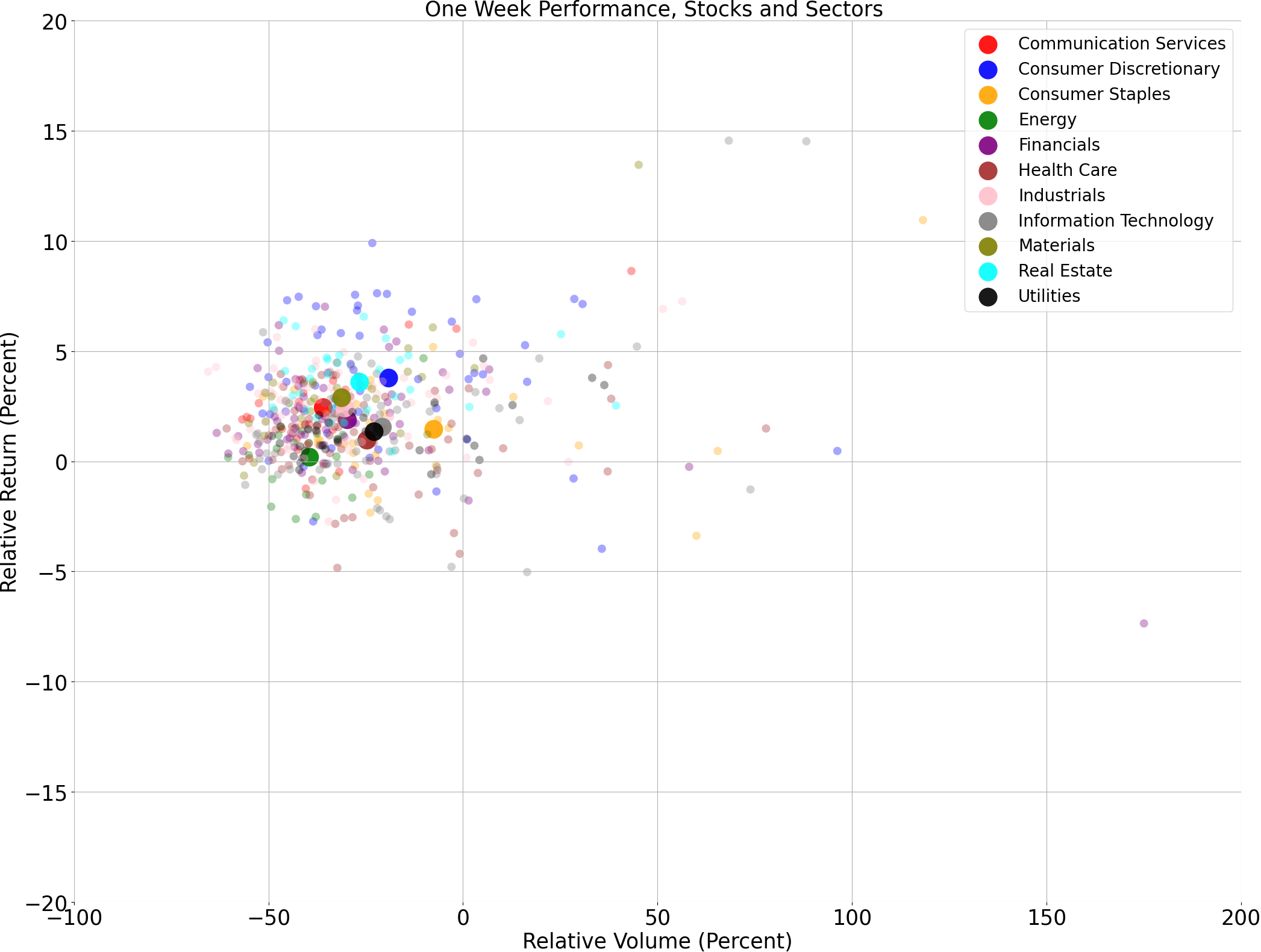

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

A technical analysis across indices

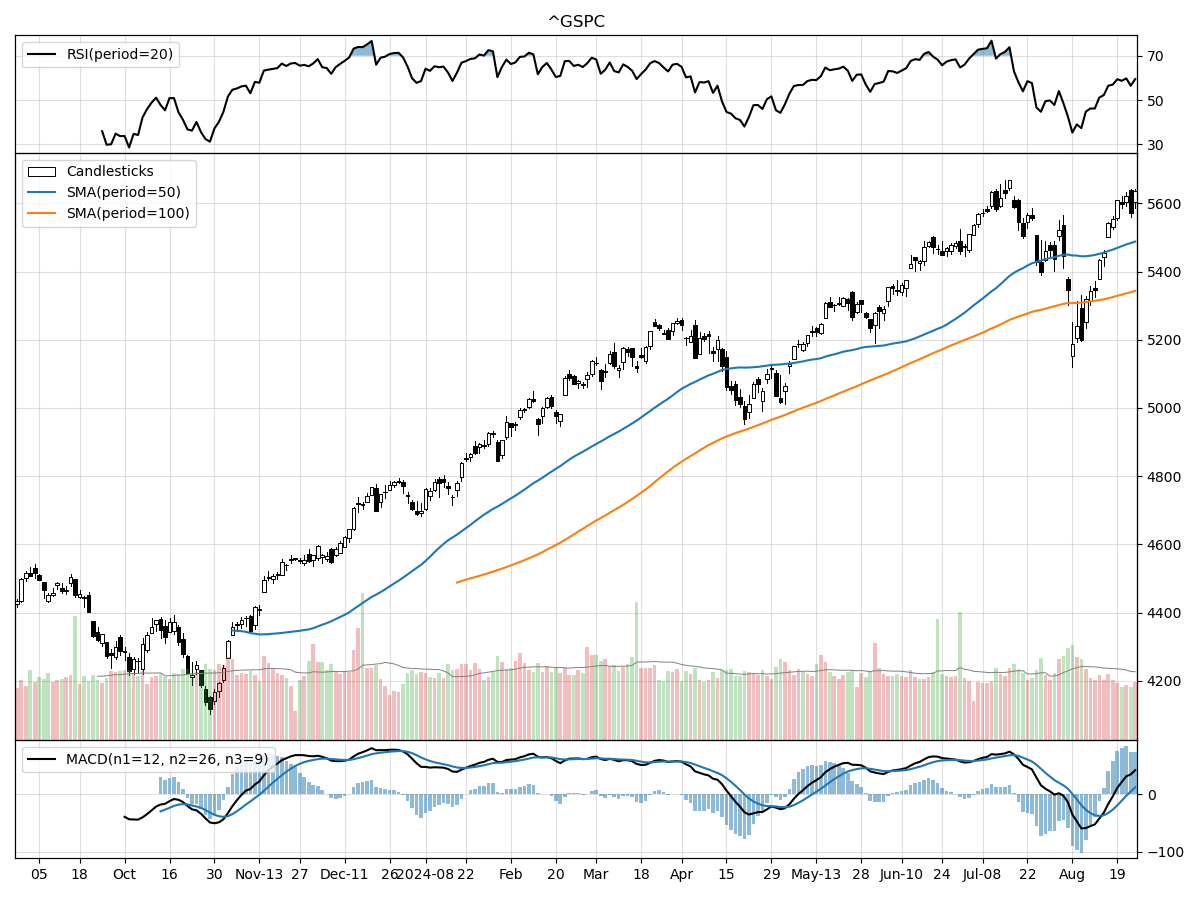

S&P500

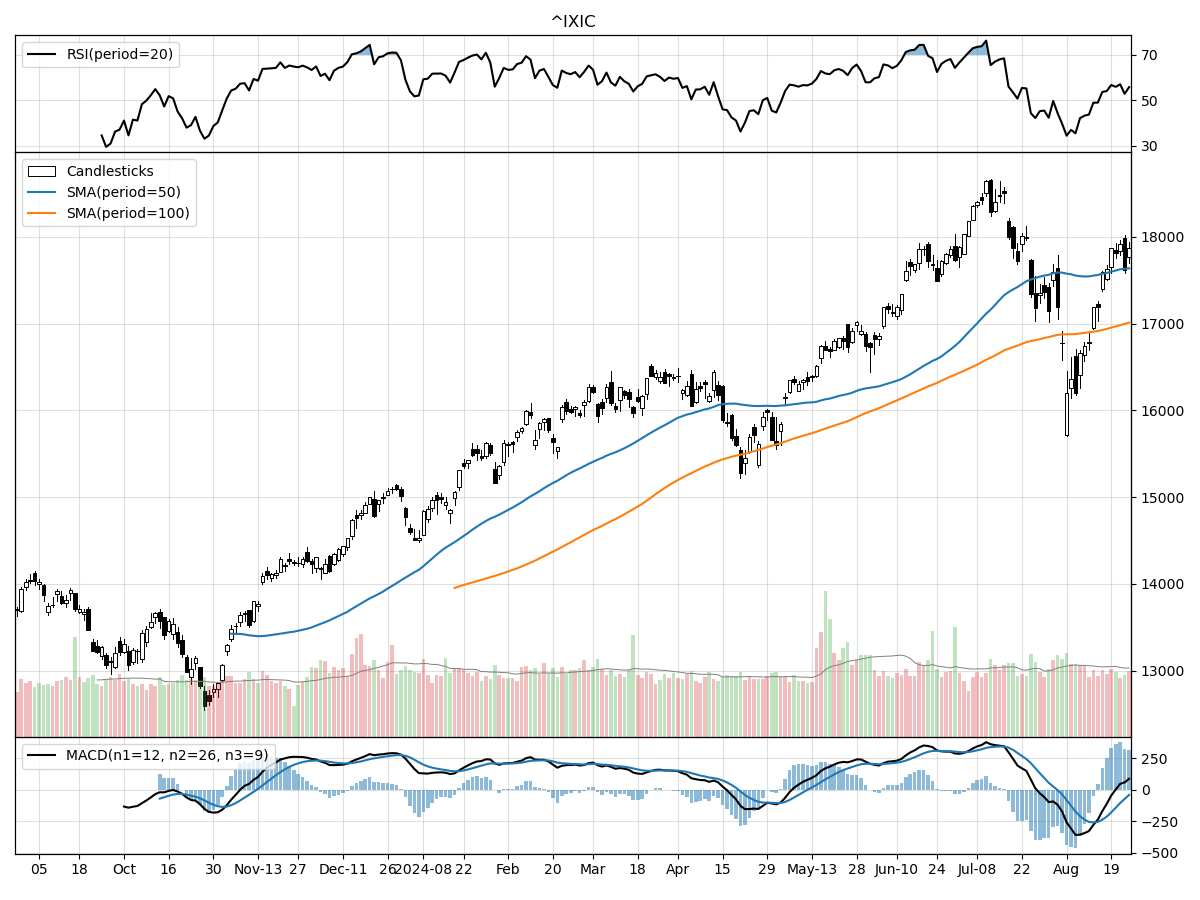

Nasdaq

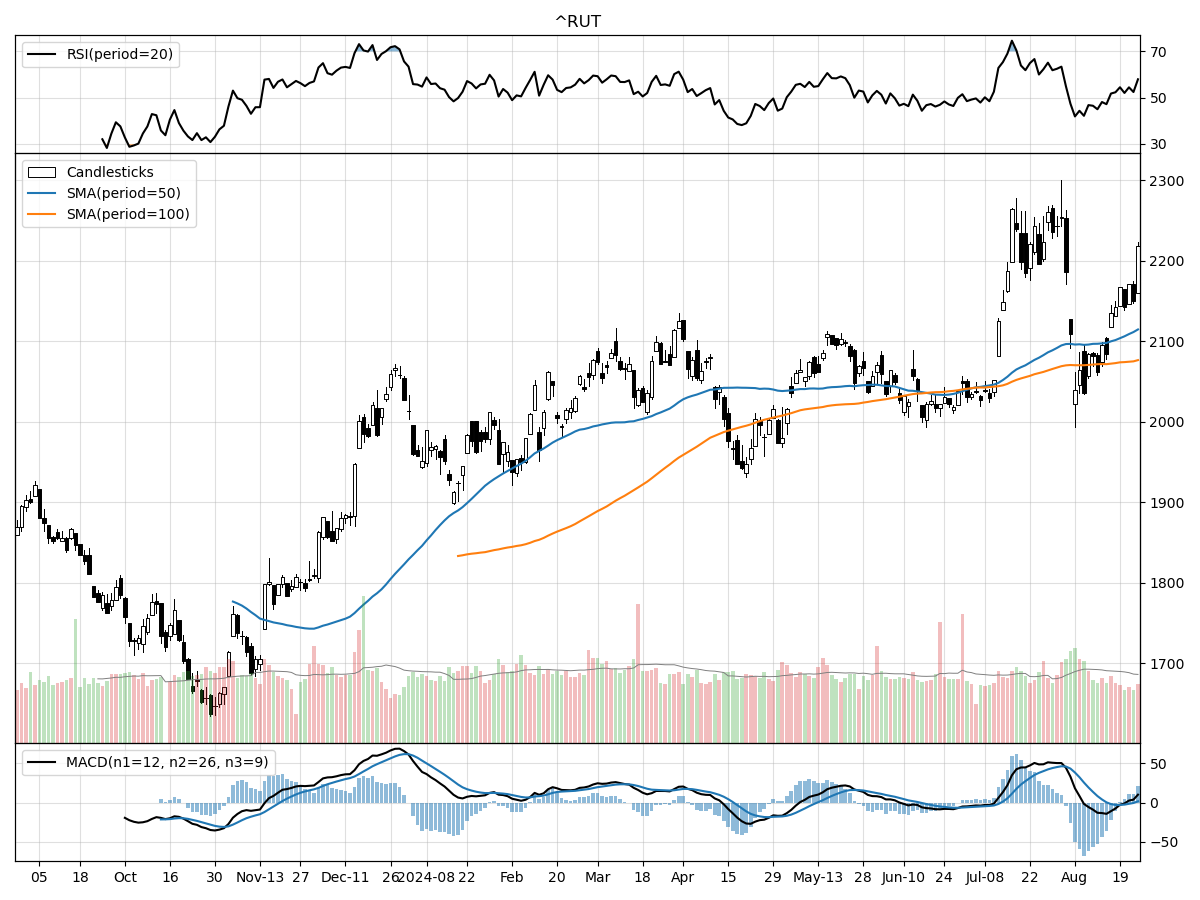

Russell 2000

The technical performance of the S&P 500, Nasdaq, and Russell 2000 indices reveals some intriguing variations and similarities in their recent market behavior. The S&P 500 and Russell 2000 indices both exhibit a stable price trend over the last month and have seen a significant rise over the last three months, with the S&P 500 up by 7.62% and the Russell 2000 up by 7.88%. The Nasdaq has shown a slightly lower increase of 6.82% over the same period. All three indices are trading well above their 52-week lows, with the Nasdaq leading at 41%, followed by the S&P 500 at 36%, and the Russell 2000 at 35%. However, the Nasdaq is currently 4% below its 52-week high, while the S&P 500 and Russell 2000 are almost at their 52-week highs, with the S&P 500 at its peak and the Russell 2000 just 1% below.

In terms of volume and momentum indicators, the Nasdaq stands out with a higher recent daily volume compared to its long-term average, suggesting increased trading activity. The S&P 500 and Russell 2000 show relatively stable volumes. Money flow indicators suggest heavy buying pressure for both the S&P 500 and Nasdaq, while the Russell 2000 experiences moderate buying pressure. Notably, the S&P 500 and Nasdaq are under accumulation, whereas the Russell 2000 is under distribution. From a momentum perspective, the MACD is bullish for both the S&P 500 and Russell 2000, indicating upward momentum, while it is bearish for the Nasdaq, suggesting a potential downward trend. The RSI indicates that the S&P 500 is modestly overbought, whereas the Nasdaq is in a neutral state, indicating neither overbought nor oversold conditions.

These technical insights suggest that the S&P 500 is currently experiencing strong upward momentum but might be approaching overbought conditions, while the Nasdaq shows high trading activity but potential bearish momentum. The Russell 2000, with its moderate buying pressure and bullish MACD, indicates a balanced yet positive outlook, although the distribution trend could be a concern. Investors should consider these technical factors in conjunction with broader market conditions and individual investment goals.

Last week vs. history (Large Cap S&P 500)

Market Commentary

In the world of finance, last week's Federal Reserve symposium in Jackson Hole, Wyoming, served as a critical juncture for monetary policy observers. The annual event, often likened to a monetary-policy red carpet, provided no formal policy decisions but offered valuable insights into the Fed's future direction. Fed Chair Jerome Powell's much-anticipated speech did not deliver any surprises, but it did set the stage for what investors might expect in the coming months. The symposium's discussions have left markets eagerly awaiting the Fed's next official meetings, where significant actions are anticipated.

One of the key takeaways from Powell's speech is the likely timeline for interest rate cuts, which are expected to commence in September. The Fed has maintained a steady policy rate for over a year, primarily due to its dual mandate of stable inflation and maximum employment not being fully met. However, recent commentary suggests that the Fed now sees sufficient progress on both fronts to begin adjusting rates. This shift indicates that the long wait for rate cuts is almost over, but the goalposts have moved, with the Fed's focus now more balanced between inflation and employment data.

The central bank's fight against inflation has shown signs of success, with core CPI at 3.2%, marking its lowest level since April 2021. This decline in inflation, coupled with a softening labor market, suggests that the Fed may soon ease its restrictive monetary policy. Recent data, including July's underwhelming jobs report, have sparked recession worries, but these concerns appear to be overblown. While the labor market has shown some signs of weakness, it remains robust enough to avoid an immediate economic downturn.

Interestingly, this upcoming rate-cutting cycle is not driven by a collapsing economy or a financial crisis, as has often been the case in the past. Instead, the Fed aims to gradually reduce rates to bring monetary policy closer to a neutral setting. This approach is more about letting off the brake rather than pressing on the gas pedal. Powell emphasized that the Fed will be highly data-dependent in making policy changes, suggesting that the path for rate cuts may be inconsistent, with cuts and pauses interspersed over the next year.

Historically, interest rate cuts have been favorable for financial markets, and this time is expected to be no different. The stock market has already rallied in anticipation of these cuts, with the S&P 500 index returning nearly 40% since interest rates peaked last October. However, the benefits of lower rates may not be fully exhausted, as a soft landing for the economy could provide a boost to corporate profits and extend the current bull market into 2025. Lower rates can also support stock-market valuations and bond-market returns.

Despite the positive outlook, investors should brace for some volatility. Initial Fed rate cuts often accompany shifts in economic and financial conditions, leading to choppy market performance in the short term. Additionally, uncertainties surrounding the U.S. presidential election and geopolitical issues could contribute to market anxiety. While the Fed's shift to less restrictive policy is broadly seen as a tailwind, it won't eliminate periodic swings or volatility for the remainder of 2024.

Looking back over the past 40 years, stock-market performance following initial Fed rate cuts has generally been positive, although not without short-term turbulence. The broader performance of equities in the one and two years following the commencement of rate cuts has often been strong, especially in periods where rate cuts were not followed by a recession. This historical context supports a positive view for financial markets ahead, even if a recession cannot be entirely ruled out.

In summary, the Fed's recent commentary from Jackson Hole indicates a likely shift towards rate cuts starting in September, driven by progress on inflation and a softening labor market. This upcoming rate-cutting cycle is unique in its approach, focusing on easing restrictive policy rather than stimulating a collapsing economy. While the outlook for financial markets appears favorable, investors should remain cautious of potential volatility and economic uncertainties. The historical performance of equities following rate cuts offers a positive precedent, suggesting that the current bull market could extend into the coming years.

Stock study for Tuesday

Bath & Body Works, Inc. is a prominent global retailer specializing in home fragrance, body care, and soap and sanitizer products, operating under brands like Bath & Body Works and White Barn. Transitioning from an apparel-based retailer, the company now focuses on exclusive fragrances for both body and home, distributing products through 1,850 company-operated stores and e-commerce sites in North America, along with additional international locations via franchise and wholesale arrangements. Their growth strategies revolve around brand innovation, international expansion, customer engagement through loyalty programs and digital optimization, and maintaining operational excellence. The company frequently launches new fragrances and products, driven by strong product development capabilities and strategic vendor partnerships, to adapt to changing customer preferences.

Comments ()