The Monday Charge: April 15, 2024

As the stock market's unwavering ascent finally shows signs of faltering, investors are grappling with a new reality: inflation is not receding as quickly as many had hoped.

This is our Monday article, focusing on the large cap S&P 500 index. Just the information you need to start your investing week. As always, 100% generated by AI and Data Science, informed, objective, unbiased, and data-driven.

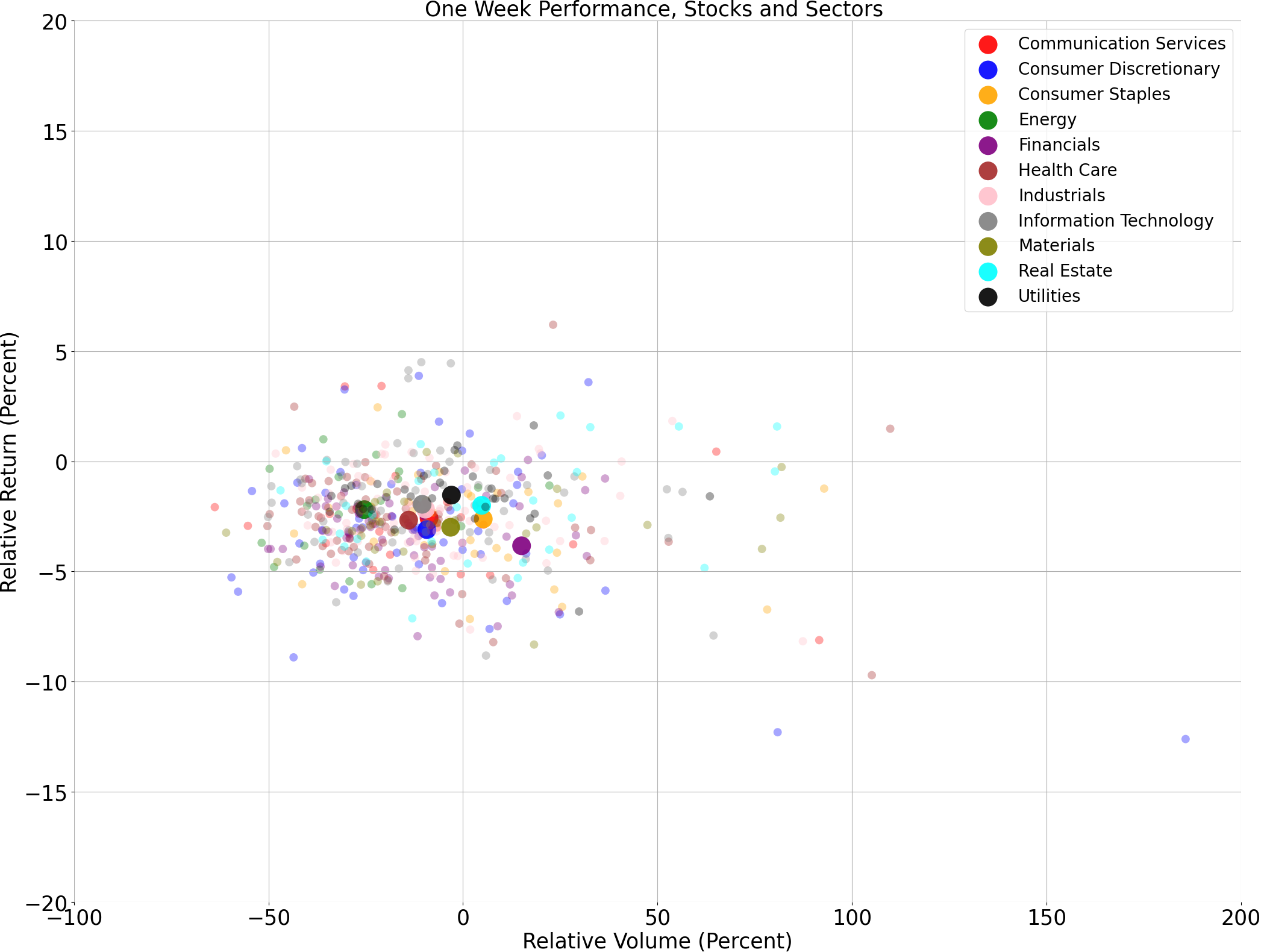

The biggest movers last week on price and volume (Large Cap S&P 500)

Price and volume moves last week for every stock and sector (Large Cap S&P 500)

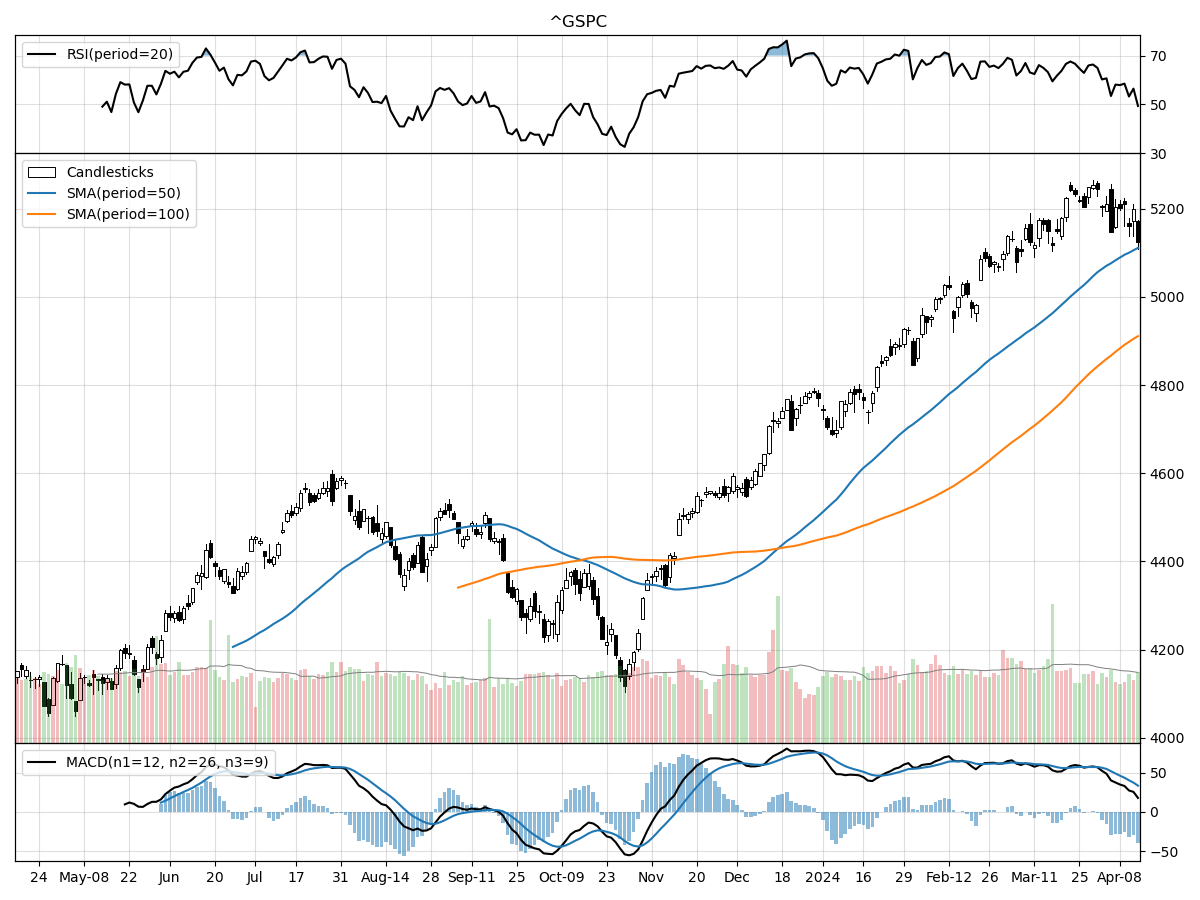

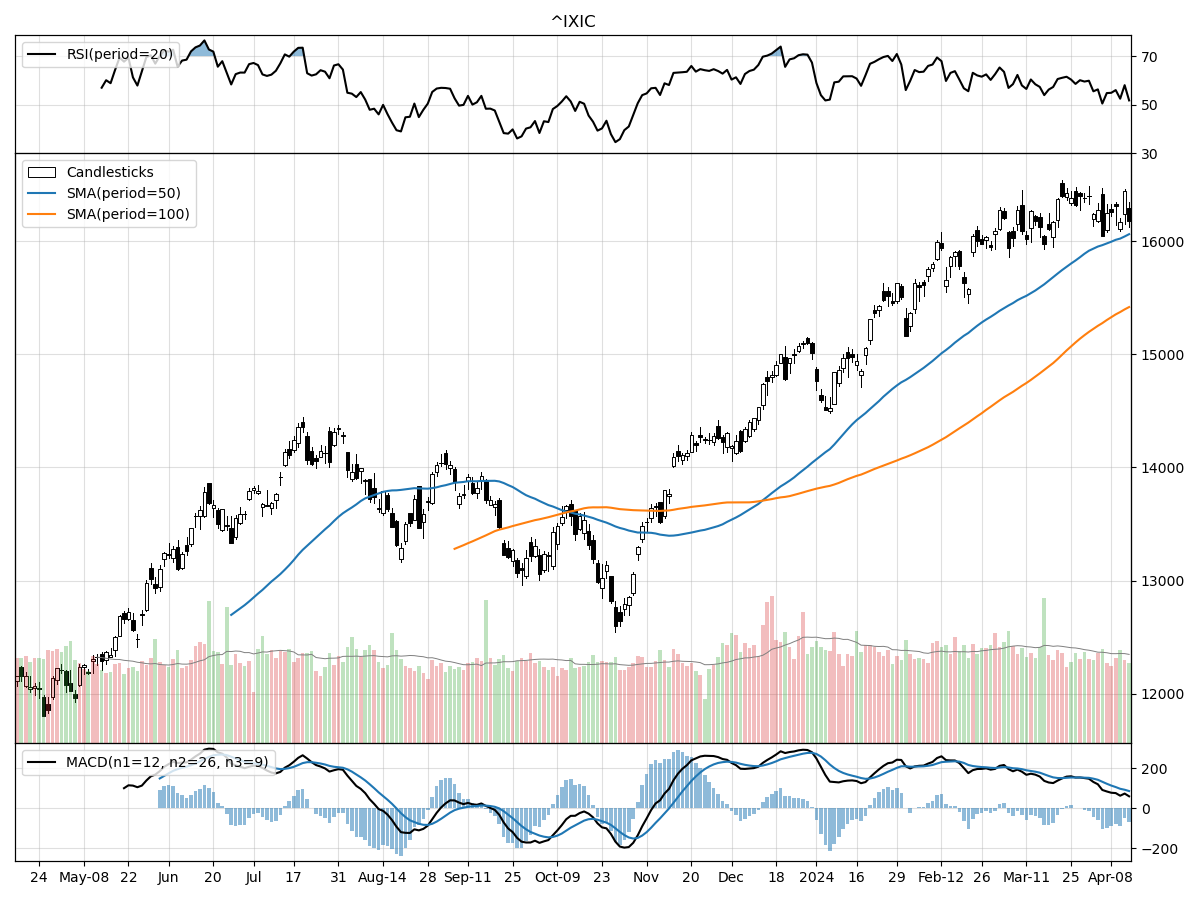

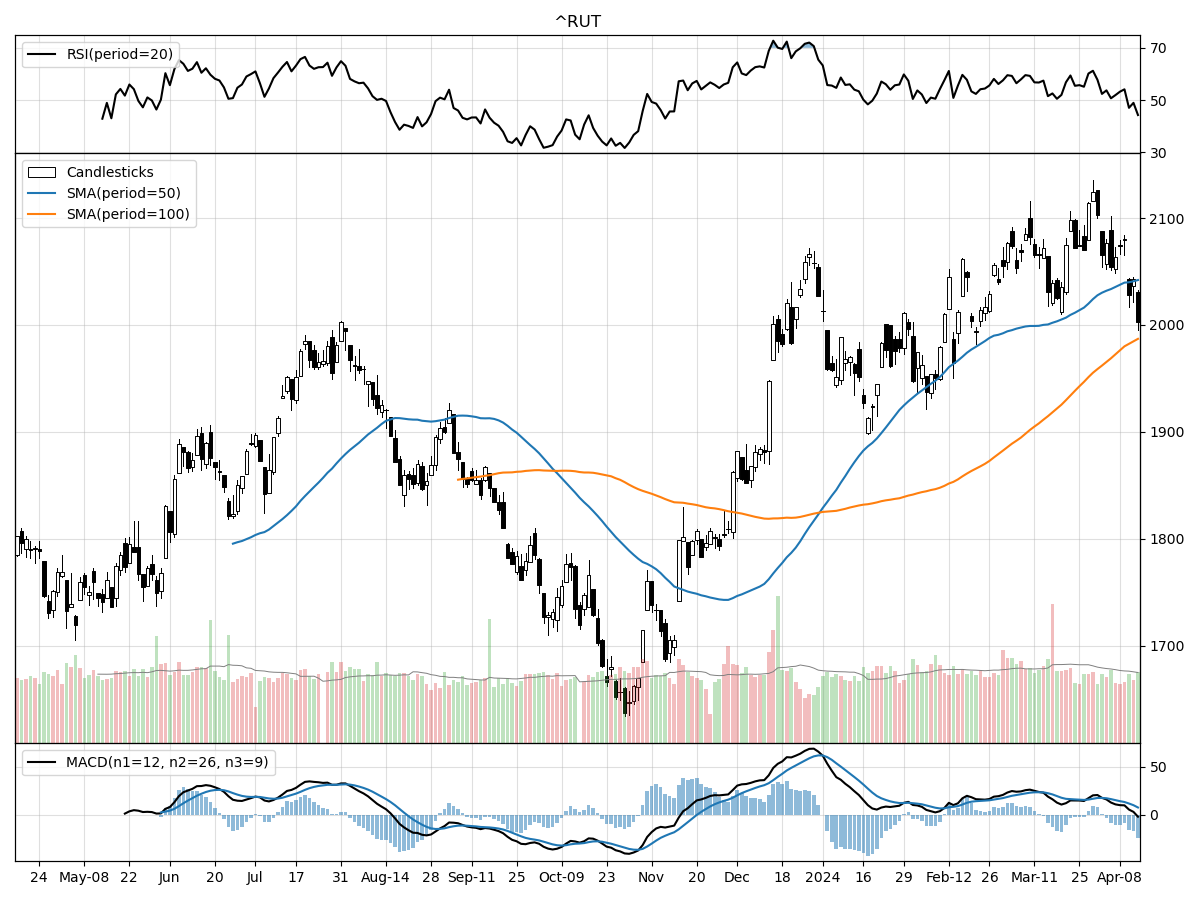

A technical analysis across indices

S&P500

Nasdaq

Russell 2000

Across the S&P 500, Nasdaq, and Russell 2000 Small Cap indices, there are both converging and diverging technical performance indicators that can help guide investment decisions. All three indices are currently experiencing bullish momentum as indicated by their positive MACD (Moving Average Convergence Divergence) values, which suggests that in the short to intermediate term, the trend for each index has been upward. The S&P 500 and Nasdaq have both seen price increases over the last three months, with gains of 7.16% and 7.44% respectively, while the Russell 2000 has remained relatively stable in the same period, indicating a divergence in performance where larger-cap stocks (S&P 500 and Nasdaq) have outperformed small-cap stocks (Russell 2000).

In terms of money flow indicators, which measure the buying and selling pressure, there's a mixed signal among the indices. The S&P 500 is under moderate selling pressure and distribution, which could indicate a potential shift in investor sentiment or profit-taking activities. Conversely, the Nasdaq and Russell 2000 are under accumulation, suggesting that investors are buying into these stocks, which could be seen as a positive sign for continued upward movement. The current stock prices of all three indices are well above their respective 52-week lows, showing a strong recovery from any lows within the past year. However, the proximity of the S&P 500 and Nasdaq to their 52-week highs (2% and 1% below, respectively) may imply limited upside potential in the near term, while the Russell 2000 has a slightly larger buffer of 5%, which could suggest more room for growth.

The daily trading volume has been relatively consistent with the longer-term average for all three indices, indicating a stable level of investor participation. The Relative Strength Index (RSI) readings for the Nasdaq and Russell 2000 show that neither is currently overbought or oversold, which typically suggests that there is no immediate momentum exhaustion and that the current trend could persist. However, without the RSI data for the S&P 500, the analysis is incomplete for that index. Overall, while the indices share some similarities in technical performance, there are distinct differences in money flow and proximity to their respective 52-week highs that could influence an investor's decision depending on their strategy and risk tolerance.

Last week vs. history (Large Cap S&P 500)

Market Commentary

Markets Navigate a Turbulent Path as Inflation Shadows Fed's Next Move

As the stock market's unwavering ascent finally shows signs of faltering, investors are grappling with a new reality: inflation is not receding as quickly as many had hoped. Last week, the financial world's gaze shifted from the spectacle of a solar eclipse to the less celestial, but equally riveting, Consumer Price Index (CPI) report. The numbers came in hot, challenging the market's rosy expectations of imminent Federal Reserve rate cuts and potentially charting a new trajectory for equity prices.

The CPI, a barometer for inflation, indicated a year-over-year increase of 3.5% in March, slightly up from the previous month. Core CPI, which excludes the volatile food and energy sectors, remained unchanged at 3.8%, slightly above forecasts. This stubbornness in core inflation, particularly driven by service sectors like medical care and insurance, suggests that the economy's robust demand is contributing to persistent price pressures, despite improvements in goods prices as supply chains have normalized.

Investors had previously been buoyed by the prospect of a dovish pivot from the Fed, with markets at one point pricing in as many as six rate cuts for 2024. However, the recent inflation data have poured cold water on these expectations, prompting a reassessment of the timeline and extent of monetary easing. The anticipation of rate cuts had been a key driver of the stock market's rally since October 2023, with the S&P 500 reaching new heights amid a streak of weekly gains.

Despite the latest inflation report's implications, it is not all doom and gloom for the markets. There is still room for shelter costs to moderate, which would help ease overall inflation. Moreover, the economy's underlying strength, reflected in areas like manufacturing and business investment, provides a solid foundation for corporate earnings growth. This resilience suggests that while the path to the Fed's 2% inflation target may be more gradual and challenging, the backdrop for the financial markets remains fundamentally sound.

The recalibration of rate cut expectations has led to a dip in the market, but it is worth noting that the reaction has been relatively subdued compared to previous periods of monetary tightening. This measured response may indicate that investors are confident in the economy's ability to withstand a slower pace of policy easing. It also underscores the importance of the Fed's careful approach to ensure that inflation is on a sustainable downward trajectory before loosening its grip on rates.

Looking ahead, the "sell in May and go away" adage seems less relevant in the current context. Historical data suggest that market performance during the summer months does not justify a seasonal overhaul of investment strategies. As the market navigates the complex interplay between inflation data and Fed policy, investors would do well to focus on the long-term trends and the economy's enduring strengths rather than react to short-term fluctuations.

In summary, while inflation continues to cast a shadow over the market's future, the underlying economic indicators point to a resilient backdrop that should support continued growth. The journey towards a more accommodative monetary policy may have hit a bump, but the road ahead still holds promise for patient and strategic investors.

AI stock picks for the week (Large Cap S&P 500)