Pfizer Inc. (PFE), Large Cap AI Study of the Week

December 19, 2023

Weekly AI Pick from the S&P 500

Pfizer Inc. (PFE)

Company Overview

Pfizer Inc., a global biopharmaceutical company, is known for its discovery, development, manufacturing, and distribution of therapies and vaccines. The company made strategic acquisitions in 2022, such as Arena, GBT, and Biohaven, which expanded its treatment options for immuno-inflammatory diseases, sickle cell disease, and migraines. Pfizer operates through two main segments: Biopharma, focusing on innovative biopharmaceuticals, and PC1, which offers contract development and manufacturing services. A significant part of Pfizer's strategy is to drive growth by enhancing its product pipeline and engaging in business development to improve its portfolio.

The company places a strong emphasis on Research and Development (R&D), prioritizing highly differentiated medicines and vaccines and forming collaborations to share innovation, risks, and costs. Internationally, Pfizer is present in over 185 countries, with more than half of its 2022 revenue coming from outside the U.S., largely due to COVID-19 related products. It collaborates with entities like BioNTech and BMS to develop and promote products, sharing costs and profits.

Pfizer markets its products directly to healthcare providers, patients, and various organizations, and employs direct-to-consumer advertising in the U.S. The company has adapted to digital outreach during the COVID-19 pandemic and holds numerous patents, such as those for Inlyta and Eliquis, which are critical for protecting its products and manufacturing processes. However, the expiration of these patents can lead to increased competition and revenue loss.

The pharmaceutical market is highly competitive and regulated, with Pfizer facing competition from generics, biosimilars, and other research-based pharmaceutical companies. Pfizer counters this through innovation, R&D, and business development. Additionally, the company anticipates changes in healthcare payment models and works with payers and the government to improve patient access. Pfizer has not encountered significant raw material shortages and follows strict regulations set by government agencies like the FDA to ensure compliance and market their products effectively.

By the Numbers

- 2022 Total Revenues: $100.3 billion (23% increase from 2021)

- 2022 Net Cash from Operations: $29.3 billion (10% decline from 2021)

- 2022 Adjusted Diluted EPS: $6.58 (62% increase from 2021)

- 2022 Reported Diluted EPS: $5.47 (42% increase from 2021)

- 2022 Operational Revenue Growth (excluding COVID-19 products): 2%

- 2023 Projected Operational Revenues: Between $67 and $71 billion (anticipated decrease)

- 2022 Income from Continuing Operations Before Taxes: $34.7 billion ($10.4 billion surge from 2021)

- 2022 R&D Investments: Substantial, exact figure not specified

- 2022 In-Process Research and Development (IPR&D) Assets: Valued at $11.4 billion

- 2022 Actual Returns on U.S. Pension Plan Assets: (22.4)%

- 2022 Biopharma Segment Revenue Increase: 24%

- 2022 Pfizer CentreOne Revenue Decline: 22%

- 2022 Revenue Deductions (rebates, allowances, etc.): $19.7 billion

- Q3 2023 Revenues: $13.2 billion (42% decrease from Q3 2022)

- First Nine Months of 2023 Revenues: $44.2 billion (42% decrease from the same period in 2022)

- Q3 2023 Loss from Continuing Operations Before Tax: $3.4 billion (compared to income in Q3 2022)

- First Nine Months of 2023 Income from Continuing Operations Before Taxes: $5.2 billion (down from $29.5 billion in the same period of 2022)

- Cost Realignment Program Savings Target by 2024: At least $3.5 billion

- Cost Realignment Program Expected Expenditure: $3.0 billion

- Q3 2023 Costs from Tornado Damage: $209 million

- Q3 2023 Comirnaty Sales: $1.3 billion (70% decrease from Q3 2022)

- Q3 2023 Paxlovid Sales: 97% decrease from Q3 2022

- Q3 2023 Eliquis Sales Growth: 3%

- Q3 2023 Prevnar Family Sales Growth: 15%

- Q3 2023 Cost of Sales: $9.269 billion (53% increase from Q3 2022)

- First Nine Months of 2023 Cost of Sales: 30% decrease from the same period in 2022

- Q3 2023 Selling, Informational, and Administrative Expenses: Slight decrease from Q3 2022

- First Nine Months of 2023 Selling, Informational, and Administrative Expenses: 13% increase from the same period in 2022

- Q3 2023 Research and Development Expenses: Minor increase from Q3 2022

- Q3 2023 Amortization of Intangible Assets: Significant increase due to acquisitions

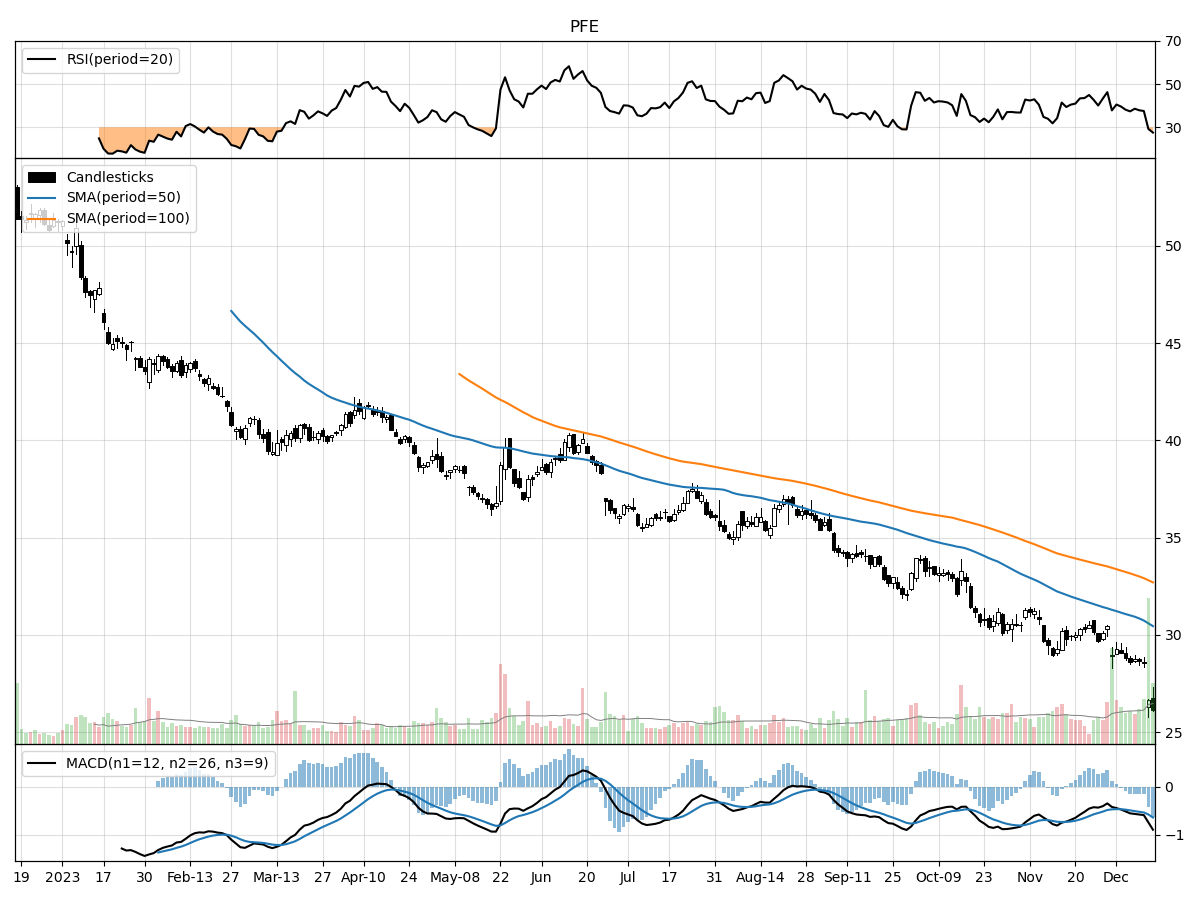

Stock Performance and Technical Analysis

The current stock price is exactly at its 52-week low, which could indicate a potential support level or a sign that the stock is out of favor with investors. The fact that it is 51% below its 52-week high suggests that the stock has experienced significant selling pressure over the past year. The recent price decline of 12% over the last month and 20% over the last quarter further underscores the bearish sentiment that has been dominating the stock. However, reaching a 52-week low could sometimes present a buying opportunity if the fundamentals of the company remain strong and the downward movement is believed to be temporary or overdone.

The daily trading volume is an important aspect to consider. The recent daily volume is significantly higher than the long-term average, indicating that there has been more interest in the stock, potentially due to the sharp decline in price. This heightened volume in the context of a declining price could be a sign of capitulation, where sellers are exiting their positions en masse, sometimes marking the end of a downtrend.

The Money Flow indicators suggest that the stock is currently under moderate selling pressure, which aligns with the observed decline in price. Yet, the stock is also under accumulation, which means some investors are starting to buy shares, anticipating a potential reversal or believing the stock to be undervalued at its current price. The Relative Strength Index (RSI), a momentum oscillator, indicates that the stock is oversold. An RSI reading below 30 typically suggests that a security is oversold and could be due for a bounce or reversal. On the other hand, the Moving Average Convergence Divergence (MACD) is bearish at -0.63. The MACD is a trend-following momentum indicator, and a negative value implies that the short-term momentum is weaker than the long-term momentum, possibly indicating a continuation of the downward trend.

In conclusion, the technical analysis presents a mixed picture for the stock. While there are signs of overselling and some level of accumulation, which could point to a potential reversal, the bearish MACD and the significant drop from the 52-week high suggest that caution is warranted. As a stock analyst, it would be essential to balance these technical indicators with an assessment of the company's fundamentals before making an investment decision. It may also be prudent to watch for additional signs of stabilization or reversal, such as a bullish divergence on the RSI or a cross into positive territory on the MACD, before considering entering a position.

The ‘Bull’ Perspective

Title: Pfizer Inc. (PFE): A Resilient Investment Opportunity Amidst Challenges

Upfront Summary:

- Diversified Portfolio and Strong Pipeline: Pfizer's extensive portfolio and robust pipeline, including 90+ clinical-stage programs, ensure long-term growth beyond its COVID-19 products.

- Strategic Acquisitions and Partnerships: Recent strategic moves, like the planned acquisition of Seagen and partnerships, position Pfizer for expansion in lucrative markets.

- Cost Realignment Initiatives: Pfizer's aggressive cost-saving program aims to save $3.5 billion by 2024, which will improve operational efficiency and margins.

- Solid Financial Position: Despite a downturn, Pfizer maintains a strong balance sheet, with significant cash reserves and a low debt-to-equity ratio, indicating financial resilience.

- Attractive Valuation and Dividend: Pfizer's current valuation and consistent dividend payouts present an attractive entry point for long-term investors.

Elaboration on Points:

- Diversified Portfolio and Strong Pipeline:

Pfizer's diverse portfolio, which includes high-performing drugs like Eliquis and the Prevnar family, has demonstrated growth, with Eliquis up by 3% and Prevnar by 15%. The company's pipeline is particularly robust, featuring over 90 clinical-stage programs targeting various indications, which mitigates the risk of over-reliance on any single product. This positions Pfizer to drive future revenue growth as these products mature and reach the market. The downturn in COVID-19 product sales is a temporary setback, and the company's non-COVID portfolio growth of 7% in the recent quarter underscores its underlying strength. - Strategic Acquisitions and Partnerships:

Pfizer's strategic business development activities, such as the planned acquisition of Seagen, a leader in antibody-drug conjugates for cancer therapy, underscore the company's commitment to expanding its oncology footprint. Additionally, the partnership with Flagship Pioneering to develop innovative therapeutics further enhances Pfizer's future prospects. These moves are expected to unlock new revenue streams and drive growth in high-margin areas. The company's proactive approach to M&A and collaboration bodes well for future innovation and market positioning. - Cost Realignment Initiatives:

Pfizer is not resting on its laurels; it has launched a cost realignment program that is anticipated to save at least $3.5 billion by 2024. This program is a strategic step to offset the increased costs and lower revenues experienced in Q3 2023. By optimizing R&D operations and streamlining its organizational structure, Pfizer is poised to emerge leaner and more efficient, which will enhance its competitive edge and profitability in the long run. - Solid Financial Position:

Despite the recent financial downturn, Pfizer's financial health remains robust. The company boasts a solid balance sheet, with substantial cash reserves and a low debt-to-equity ratio compared to industry peers. This financial stability provides Pfizer with the flexibility to navigate market uncertainties, invest in growth opportunities, and weather the impacts of external challenges such as the Inflation Reduction Act and industry consolidation. - Attractive Valuation and Dividend:

Pfizer's stock is currently trading at an attractive valuation, with a forward P/E ratio that is compelling when compared to the broader market and its pharmaceutical peers. Moreover, the company has a history of delivering consistent dividend payouts, which have become even more attractive in the current market environment. For investors seeking a blend of value and income, Pfizer's stock presents a prime opportunity, especially when considering the potential upside from its growth initiatives and pipeline maturation.

Conclusion:

In conclusion, while Pfizer Inc. has faced headwinds with the decline in COVID-19 product sales and external risks, the company's diversified portfolio, strategic business developments, cost-saving initiatives, solid financial standing, and attractive valuation make it a resilient investment opportunity. For long-term investors, the current challenges may represent a strategic entry point to capitalize on Pfizer's growth trajectory and enduring commitment to innovation and shareholder value.

The ‘Bear’ Perspective

Why Investors Should Steer Clear of Pfizer Inc. Stock

- Significant Revenue Decline: Pfizer's revenue plummeted by 42% to $13.2 billion in Q3 2023, with a similar decrease over the first nine months.

- Overreliance on COVID-19 Products: The company's COVID-19 products, which previously drove revenue, are now facing a 70% and 95% forecasted revenue decrease for Paxlovid and Comirnaty, respectively.

- Operational Challenges: Pfizer is grappling with operational challenges including a costly tornado impact, restructuring expenses, and potential supply chain disruptions.

- Regulatory and Pricing Pressures: Governmental pressures on drug pricing, such as the Inflation Reduction Act, are expected to impact Pfizer's profitability.

- Legal and Compliance Risks: Ongoing legal proceedings and the need for stringent regulatory compliance present significant risks to Pfizer's financial health.

Elaboration on Key Points

- Significant Revenue Decline

Pfizer Inc.'s financial downturn in Q3 2023 is a red flag for investors, with revenues taking a nosedive of 42% to $13.2 billion. Over the first three quarters, the revenue decrease mirrored this trend, signaling a distressing pattern rather than a one-off event. Such a drastic reduction in revenue is a clear indicator of the company's waning sales, particularly as it tries to pivot away from its COVID-19 product reliance. With Pfizer's income from continuing operations before taxes crashing from $29.5 billion to $5.2 billion in the first nine months year-over-year, investors should question the company's ability to bounce back in the near term. - Overreliance on COVID-19 Products

The sharp decline in sales of Pfizer's COVID-19 products is a cause for concern. Paxlovid and Comirnaty have seen forecasted revenue decreases of 70% and 95%, respectively, for the year 2023. This is particularly troubling considering these products previously accounted for a significant portion of Pfizer's revenue stream. As the pandemic wanes and the world adapts to living with the virus, the demand for these products is naturally diminishing. This overreliance on a now-dwindling revenue source could spell trouble for Pfizer's future growth prospects. - Operational Challenges

Pfizer is currently facing several operational headwinds. The tornado that struck its Rocky Mount, NC manufacturing facility in July 2023 has already resulted in $209 million in costs for Q3, and while production is expected to recover by year-end, the incident underscores the vulnerability of Pfizer's supply chain. Additionally, the company is in the midst of a costly restructuring process and has launched a cost realignment program to save $3.5 billion by 2024, with $3.0 billion in expected expenditures to achieve these savings. These operational challenges could strain the company's resources and detract from its focus on growth. - Regulatory and Pricing Pressures

The pharmaceutical industry is under increasing pressure from governments worldwide to lower drug prices, and Pfizer is not immune. The U.S. Inflation Reduction Act is set to impact Medicare prices starting in 2026, which could squeeze Pfizer's profit margins. Furthermore, as the industry faces more scrutiny over pricing practices, Pfizer may be forced to reduce prices or face reimbursement hurdles, both of which could adversely affect its bottom line. - Legal and Compliance Risks

Pfizer is embroiled in various legal proceedings that could prove costly. Patent litigation and government investigations are ongoing concerns that not only risk financial penalties but also damage the company's reputation. Additionally, the pharmaceutical sector is highly regulated, and any missteps in compliance could lead to significant fines and sanctions. Pfizer's need to maintain stringent regulatory compliance across multiple jurisdictions adds to its operational complexity and risk profile.

In conclusion, while Pfizer Inc. has been a pharmaceutical powerhouse, particularly during the height of the COVID-19 pandemic, the current landscape presents a multitude of challenges that suggest caution is warranted for investors considering the stock. The combination of declining revenues, overreliance on COVID-19 products, operational hurdles, regulatory and pricing pressures, and legal and compliance risks paint a picture of a company at a precarious inflection point. Investors would be wise to consider these factors carefully before making any decisions regarding Pfizer stock.

Comments ()