Par Pacific Holdings Inc. (PARR), Mid/Small Cap AI Study of the Week

May 9nd, 2024

Weekly AI Pick from the Mid & Small Cap S&P 400 & S&P 600

Company Overview

Par Pacific Holdings, Inc. is an energy company based in Houston, operating in the refining, retail, and logistics sectors. The company owns four refineries located in Hawaii, Wyoming, Washington, and Montana, with a combined crude oil throughput capacity of 219,000 barrels per day. Its retail segment includes fuel retail outlets and convenience stores under brands like "Hele" and "nomnom" in Hawaii, Washington, and Idaho. The logistics segment manages a transportation network comprising pipelines, terminals, marine vessels, and rail facilities, ensuring efficient movement of crude oil and refined products across the Pacific, Northwest, and Rocky Mountain regions.

Par Pacific also holds equity investments in natural gas-focused Laramie Energy, LLC, and key energy infrastructure partnerships. The Wyoming refinery, with a 20 Mbpd capacity, produces various refined products and has received the EPA’s ENERGY STAR certification. The retail segment has been expanding, particularly in Washington, and the logistics segment supports crude oil transport and storage for its refiners and retail locations. Recent acquisitions of logistics assets in Montana and expansions in retail operations are potential drivers for future revenue. Economic growth in Washington State and South Dakota, particularly in the Puget Sound area and the Black Hills Region, respectively, supports the market for Wyoming refined products.

The Montana refinery benefits from economic growth in the Pacific Northwest and the Rockies, processing heavy crude oils to produce a diverse range of products. Par Pacific adheres to stringent federal and state environmental regulations, including greenhouse gas emissions initiatives and fuel standards like the Renewable Fuel Standard (RFS) and low carbon fuel standards. These regulations could increase operational costs and impact demand for petroleum products. The company maintains compliance with various environmental laws, including the Resource Conservation and Recovery Act (RCRA) and the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), with no significant liabilities identified. While air emissions regulations could increase costs, they currently have no material financial impact. Par Pacific emphasizes the value of its workforce and has a diverse customer base, with one customer accounting for 13% to 17% of consolidated revenue in recent years.

By the Numbers

Annual 10-K Report Summary for Fiscal Year 2023:

- Net Income: Increased to $728.6 million from $364.2 million in 2022.

- Adjusted EBITDA: Rose to $696.2 million from $643.4 million in 2022.

- Total Revenues: Grew to $8.23 billion from $7.32 billion in 2022.

- Cost of Revenues: Increased to $6.84 billion from $6.38 billion in 2022.

- Operating Income: Jumped to $680 million from $437.9 million in 2022.

- Refining Segment Operating Income: Increased by $274.3 million to $676.2 million.

- Logistics Segment Operating Income: Improved by $15.7 million to $69.7 million.

- Retail Segment Operating Income: Rose by $7.4 million to $56.6 million.

- Refining Adjusted Gross Margin: Increased to $995.0 million from $812.8 million in 2022.

- Logistics Adjusted Gross Margin: Grew by $31.8 million to $121.2 million.

- Retail Adjusted Gross Margin: Increased by $13.8 million to $155.3 million.

- Operating Expenses (excluding depreciation): Surged by $152.4 million to $485.6 million.

Quarterly 10-Q Report Summary for Q1 2024:

- Net Loss: Reported at $3.8 million compared to a net income of $237.9 million in Q1 2023.

- Revenues: Increased by 18% to approximately $1.98 billion.

- Cost of Revenues: Increased by 36%.

- General and Administrative Expenses: Soared by 117%.

- Adjusted EBITDA: Fell to $94.7 million from $167.6 million in Q1 2023.

- Refining Segment Operating Income: Decreased significantly to $22.6 million from $263.1 million in Q1 2023.

- Logistics Segment Operating Income: Increased to $20.4 million from $12.6 million.

- Retail Operating Income: Decreased by $2.5 million to $11.0 million.

- Refining Adjusted Gross Margin: Fell to $207.1 million, a decrease of $4.5 million year-over-year.

- Washington Refinery Adjusted Gross Margin per Barrel: Decreased by 55% to $6.13.

- Wyoming Refinery Adjusted Gross Margin per Barrel: Dropped by 46% to $14.84.

- Total Revenues for Q1 2024: Increased by $0.3 billion to $2.0 billion.

- Operating Expenses for Q1 2024: Totaled $1,971,320 thousand, a significant increase from $1,423,807 thousand in Q1 2023.

- Net Income/Loss for Q1 2024: A loss of $3,751 thousand compared to a net income of $237,890 thousand in Q1 2023.

- Adjusted EBITDA for Q1 2024: Declined to $94,698 thousand from $167,635 thousand in Q1 2023.

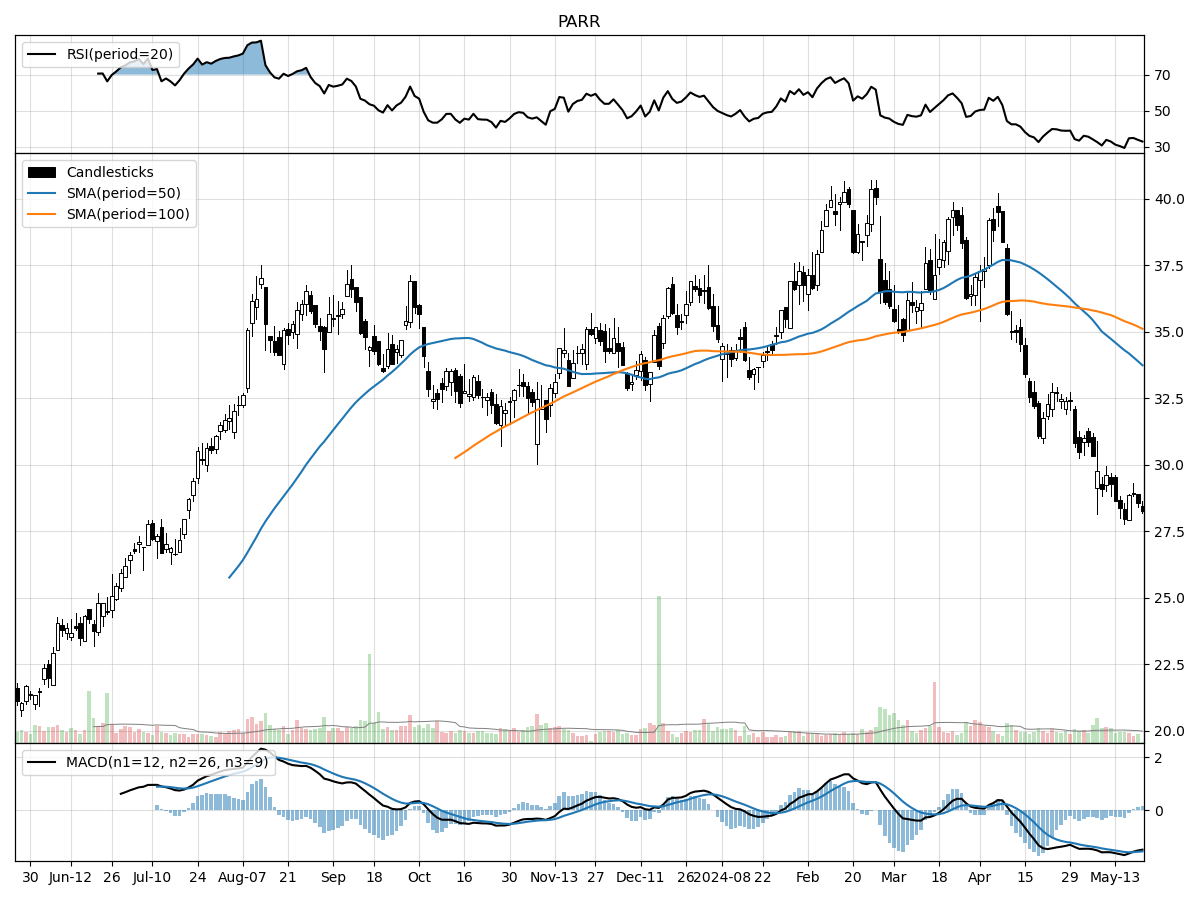

Stock Performance and Technical Analysis

As a stock analyst, when evaluating the investment potential of a company based on its technical analysis, there are several key indicators to consider. The current stock price of $28.26 is 34% above its 52-week low, suggesting the stock has rebounded from its lowest point in the past year. However, it's also 30% below its 52-week high, indicating there has been a significant pullback from its peak. This could be interpreted as the stock currently residing in a middle-range of its yearly volatility, potentially providing a buying opportunity if one believes the stock will trend upwards to retest its 52-week high.

The recent drop in price of approximately 13.55% in the last month, coupled with a larger 29.47% decline over the past three months, could alarm potential investors. This downward trend might indicate underlying issues within the company or a bearish sentiment in the market regarding this stock.

The volume analysis presents a mixed signal. The recent daily volume is lower than the longer-term average, which could suggest decreased investor interest or a consolidation phase. Lower volume can sometimes precede a breakout, but without other bullish signals, this alone is insufficient to justify an investment.

Looking at the money flow indicators, we see that the stock is under moderate selling pressure and distribution, meaning that more investors are looking to sell their shares than buy. This is typically a bearish sign as it suggests that the market participants are not confident in the stock's future performance.

Lastly, the Moving Average Convergence Divergence (MACD) is bearish at -1.57. The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a stock's price. A bearish MACD indicates that the short-term momentum is declining relative to the long-term momentum, potentially signaling a downward movement in the stock's price.

In summary, the technical analysis suggests caution. The stock's price is currently in a downward trend with bearish indicators like negative MACD and selling pressure. Traders might look for a reversal pattern or wait for more bullish signals before considering entry, while long-term investors might want to delve deeper into the fundamental analysis to determine if the current price offers a good value for the company's future growth prospects.

The ‘Bull’ Perspective

Executive Summary:

- Diversified Business Model: Par Pacific's diverse operations in refining, logistics, and retail offer a hedge against sector-specific downturns, with logistics segment operating income increasing to $20.4 million from $12.6 million year-over-year.

- Strategic Acquisitions: The acquisition of assets, such as the Billings Acquisition, has bolstered revenue streams, contributing to an 18% rise in revenues to approximately $1.98 billion.

- Improving Market Conditions: With inflation rates declining and the stock market rallying, Par Pacific is well-positioned to benefit from the improving economic environment.

- Efficiency and Cost Management: Despite current financial setbacks, Par Pacific's commitment to operational efficiency and cost management is likely to improve margins over time.

- Long-Term Growth Potential: The company's strategic investments, such as in Laramie Energy, and the anticipated rebound in energy demand post-pandemic, provide significant growth potential.

Elaboration on Key Points:

- Diversified Business Model:

Par Pacific Holdings, Inc. has demonstrated the strength of its diversified business model, which has allowed it to weather sector-specific storms. The logistics segment, in particular, has proven to be a silver lining amidst broader challenges, with its operating income increasing by a robust 62% year-over-year to $20.4 million. This diversification acts as a natural hedge, providing stability when other segments, such as refining, face headwinds due to market fluctuations or regulatory pressures. The company's total yield of 94.4% for its refined products and the increase in retail segment sales volumes to 29,431 thousand gallons from 27,123 thousand gallons year-over-year, underscore the resilience of its operations. - Strategic Acquisitions:

Strategic acquisitions have been a cornerstone of Par Pacific's growth strategy. The Billings Acquisition, for instance, has significantly contributed to the company's revenue growth, with an overall increase of $0.3 billion to $2.0 billion. Acquisitions not only expand Par Pacific's asset base and operational capabilities but also bring in new revenue streams that can offset volatility in other areas of the business. The company's ability to integrate and leverage these new assets will be critical in driving future profitability. - Improving Market Conditions:

The broader market conditions are showing signs of improvement, with inflation rates easing and the stock market reaching new highs. Such an environment is beneficial for Par Pacific as it may lead to increased consumer spending and higher demand for energy products. Moreover, as geopolitical tensions stabilize and OPEC production cuts potentially ease, crude oil prices may find a more balanced level, which could help in stabilizing the company's input costs and refining margins. - Efficiency and Cost Management:

Par Pacific is focused on efficiency and cost management, which is essential for weathering the current financial downturn and setting the stage for improved profitability. The company has been navigating increased operating expenses, which totaled $1,971,320 thousand compared to $1,423,807 thousand the previous year. By continuing to streamline operations and manage costs, Par Pacific can improve its adjusted gross margin, which has seen pressure in recent quarters. As the company adjusts to the new market realities, these efforts are expected to pay off in the form of stronger financial performance. - Long-Term Growth Potential:

Looking beyond the immediate financial challenges, Par Pacific holds significant long-term growth potential. The company's investment in Laramie Energy exposes it to the lucrative natural gas and oil exploration sector, which could yield substantial returns as global energy demand rebounds. Additionally, the anticipated increase in energy consumption post-pandemic positions Par Pacific to capitalize on rising demand. Despite the current net loss of $3.8 million, these strategic investments and market dynamics present opportunities for growth and improved shareholder value in the long run.

Conclusion:

While Par Pacific Holdings, Inc. faces headwinds, as evidenced by its Q1 2024 performance, the company's diversified business model, strategic acquisitions, improving market conditions, focus on efficiency, and long-term growth potential make it an attractive investment for the forward-looking investor. As the energy sector continues to evolve, Par Pacific's adaptability and strategic positioning are likely to drive its recovery and success in the coming years.

The ‘Bear’ Perspective

Bearish Outlook on Par Pacific Holdings, Inc. (PARR): A Case for Caution

Executive Summary:

- Substantial Net Loss: PARR reported a net loss of $3.8 million in Q1 2024, a stark contrast from a net income of $237.9 million in Q1 2023.

- Declining Refining Margins: The company's refining segment saw a significant drop in adjusted gross margin per barrel, with the Washington and Wyoming refineries experiencing a 55% and 46% decrease, respectively.

- Operational Risks and Geopolitical Concerns: Operational hazards, geopolitical events, and OPEC production cuts present substantial risks that could further destabilize the company's financials.

- Environmental and Regulatory Pressures: Compliance with evolving environmental regulations and the Renewable Fuel Standard (RFS) program could lead to increased operational costs and investment risks.

- High Debt and Interest Burden: With a substantial debt load and high-interest payments, PARR faces liquidity constraints that may limit future growth and necessitate unfavorable financing.

Detailed Analysis:

- Significant Financial Deterioration

Par Pacific Holdings, Inc.'s first quarter of 2024 has been disappointing, with a reported net loss of $3.8 million. This is a drastic shift from the $237.9 million net income in Q1 2023. Such a decline is alarming and signals underlying issues that could persist. The absence of a $94.7 million gain on RINs settlements that boosted the previous year's figures exacerbates the concern. With operating expenses and cost of revenues surging by 36% and 117% respectively, the company's profitability is being squeezed. Investors should be wary of the company's ability to manage costs and maintain profitability in a challenging economic environment. - Refining Segment Underperforming

The refining segment, traditionally a strong performer for PARR, has shown worrying signs of decline. The Washington refinery's adjusted gross margin per barrel plummeted by 55% to $6.13, while the Wyoming refinery's margin fell by 46% to $14.84 per barrel. These numbers suggest that PARR is struggling to maintain its refining profitability amid market volatility and operational challenges. This decline is particularly concerning given that refining is a core component of PARR's business model, and continued margin compression could significantly impact the company's bottom line. - Operational Risks and Geopolitical Concerns

PARR's operations are fraught with risks, including the potential for fires, explosions, and natural disasters that could disrupt operations. Geopolitical tensions, such as the ongoing Russia-Ukraine conflict, pose additional threats to the stability of crude oil prices and supply chains. The company also faces risks from OPEC production cuts, which could further exacerbate the volatility in energy prices. These factors combined create a precarious situation for PARR, where any adverse event could have outsized impacts on its financial health. - Environmental and Regulatory Pressures

Environmental and regulatory challenges are mounting for PARR. The company must navigate the complex Renewable Fuel Standard (RFS) program, which requires purchasing Renewable Identification Numbers (RINs), adding to the operational costs. The volatility in RINs prices is an unpredictable factor that could negatively impact cash flows. Moreover, initiatives to reduce carbon intensity and promote renewable energy sources are likely to decrease demand for PARR's petroleum products, while climate change legislation and potential carbon taxes could impose additional financial burdens. These factors make PARR's future profitability uncertain and potentially costly to maintain. - High Debt and Interest Burden

PARR's financial stability is further compromised by its substantial debt load and the associated high-interest payments. This debt burden limits the company's financial flexibility and could restrict its ability to invest in growth opportunities or respond to market changes. As of Q1 2024, the constraints placed on the company's liquidity raise concerns about its capacity to sustain operations without seeking additional, potentially unfavorable financing. In a rising interest rate environment, the cost of servicing this debt could escalate, further squeezing the company's financial resources.

In conclusion, while Par Pacific Holdings, Inc. may have had a strong past performance, the current financial downturn, coupled with operational, geopolitical, environmental, and financial risks, paints a bearish picture. Investors should approach PARR with caution, as the company faces a multitude of challenges that could hinder its ability to recover and grow in the near term.

Comments ()