NVIDIA, worth your chips?

NVIDIA's latest quarterly revenue surged to $18.12 billion, marking a 206% year-over-year increase, with significant contributions from its Data Center segment.

NVIDIA CORP (NVDA)

November 22, 2023

(AI generated investment deep dive into a company of interest)

Company Overview

NVIDIA Corporation is a leading technology company specializing in Graphics Processing Units (GPUs) and Systems on Chip (SoCs). It has pioneered accelerated computing and expanded into fields like artificial intelligence (AI), data science, autonomous vehicles, robotics, and 3D internet applications. NVIDIA's GPUs are used in various sectors, including gaming, professional visualization, data centers, and automotive. The company has invested over $37 billion in research and development, leading to significant technological advancements.

NVIDIA's business strategy involves combining hardware, systems, software, algorithms, libraries, and services to create unique value for their markets. New areas of growth for NVIDIA include the Hopper architecture of data center GPUs and AI cloud services. The company expects these new areas to significantly drive profit and revenue growth.

NVIDIA's proposed acquisition of Arm Limited was terminated due to significant regulatory challenges, resulting in a termination cost of $1.35 billion. The company operates in two business segments: Compute & Networking and Graphics. NVIDIA is continuously innovating its architecture, chip design, and software within these sectors to deliver enhanced performance for diverse computing requirements.

In terms of revenue generation, NVIDIA's global sales and marketing strategy relies on the technical expertise and product knowledge of its team. It operates on a fabless manufacturing strategy, employing key suppliers for the manufacturing process. The company competes with several tech giants in an intensely competitive environment driven by rapid technological changes, product performance, and pricing strategies.

NVIDIA is also committed to sustainability and plans to match its global electricity usage 100% with renewable energy purchases or generation by 2025. It is planning to build Earth-2, a digital twin of Earth on NVIDIA's AI and Omniverse platforms, which could represent a new area of business driving revenue and profit growth.

By the Numbers

Annual 10-K Report Summary for Fiscal Year 2023:

- Total Revenue: $26.97 billion

- Data Center Revenue: Increased by 41% YoY

- Gaming Revenue: Decreased by 27%

- Professional Visualization Revenue: Decreased to $1.54 billion

- Automotive Revenue: Increased by 60% YoY to $903 million

- Gross Margin: Declined by 8 percentage points to 56.9%

- Inventory Charges: Approximately $2.17 billion

- Operating Expenses: Increased by 50% YoY

- Compute & Networking Revenue: Increased by 36% YoY

- Graphics Revenue: Decreased by 25% YoY

- Effective Tax Rate: 5%

- Cash and Equivalents: $13.3 billion (down from $21.2 billion in 2022)

- Net Cash from Operating Activities: $5.6 billion

- Net Cash from Investing Activities: $7.4 billion

- Net Use of Cash in Financing Activities: $11.6 billion

- Share Repurchases and Dividends: Returned $10.04 billion and $398 million, respectively

- Long-term Debt: $9.7 billion

Quarterly 10-Q Report Summary for Q3 Fiscal Year 2024:

- Q3 Revenue: $18.12 billion (206% increase YoY)

- Revenue for First Nine Months: $38.82 billion (86% increase YoY)

- Data Center Segment Revenue Increase: 279% YoY

- Compute & Networking Segment Revenue Increase: 369% YoY

- Gross Margin for Q3: 74%

- Gross Margin for First Nine Months: 70.9%

- Operating Income for Q3: $10.42 billion

- Operating Income for First Nine Months: $19.36 billion

- Interest Income: Increased to $234 million

- Income Tax for Q3: $1.28 billion

- Cash, Cash Equivalents, and Marketable Securities: $18.28 billion

- Share Repurchases for Q3: $3.72 billion

- Share Repurchases for First Nine Months: $7.01 billion

- Cash Dividends for Q3: $99 million

- Cash Dividends for First Nine Months: $296 million

- Total Debt as of Q3 End: $9.706 billion

Key Changes and Highlights:

- Significant increase in Data Center revenue across both annual and quarterly reports.

- Decline in Gaming revenue in the annual report, with a turnaround in the quarterly report.

- Gross margin recovery in the quarterly report after a decline in the annual report.

- Substantial increase in operating income in the quarterly report.

- Increase in cash reserves in the quarterly report compared to the end of the previous fiscal year.

- Ongoing share repurchases and dividend payments, indicating a return of capital to shareholders.

- Long-term debt remains substantial but stable across the periods reported.

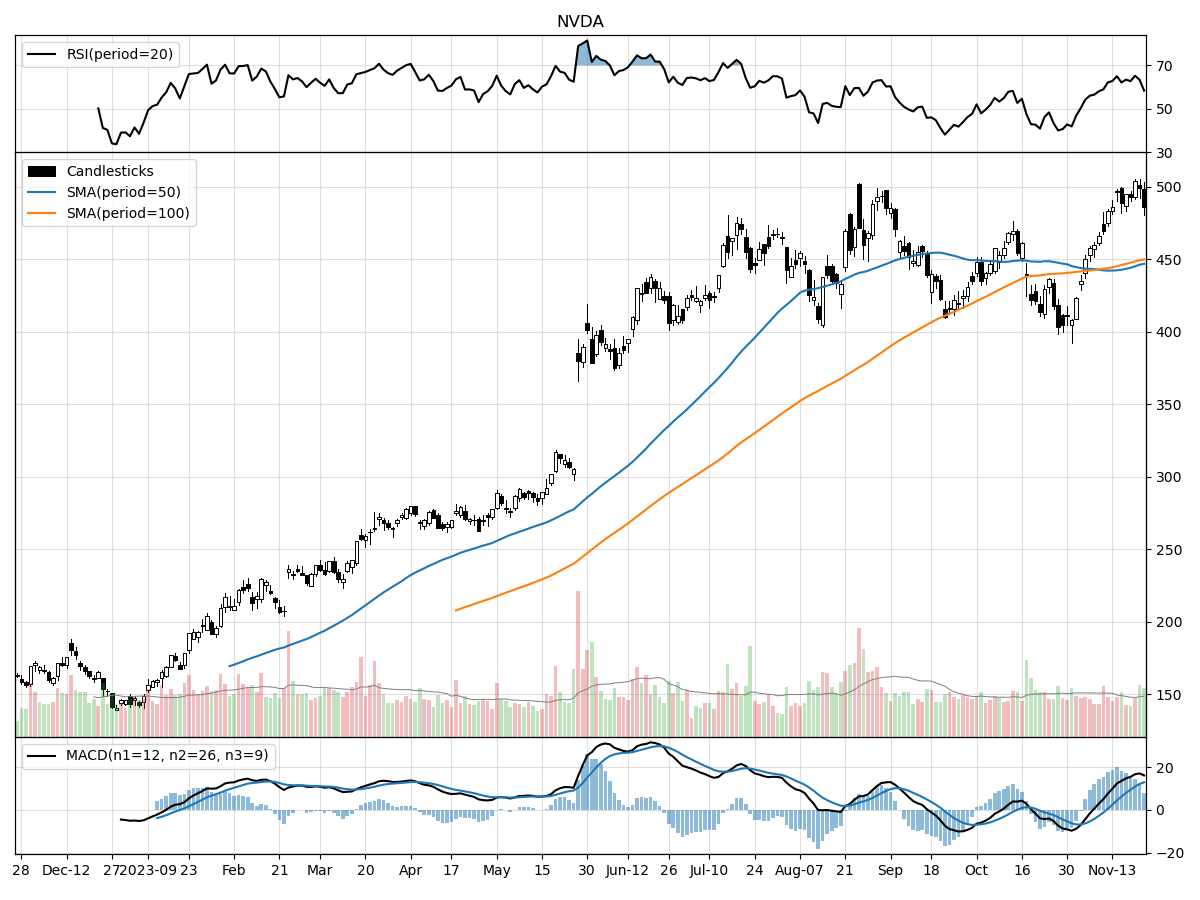

Stock Performance and Technical Analysis

Based on the technical indicators provided, the stock presents a bullish picture with The current stock price of $486.31, which is 246% above its 52-week low, indicates a strong bullish trend over the past year.

The increase of 20.59% in the stock price over the last month is a positive short-term signal, especially as it contrasts with a slight decline of 1.28% over the last three months, hinting at a possible reversal or momentum building in the more immediate term. This is further supported by the Money Flow and the Moving Average Convergence Divergence (MACD) indicators. The MACD value of 12.87, being in positive territory, is typically considered bullish and may suggest that the current trend has upward momentum. This bullishness is also indicated by the stock being under moderate buying pressure and showing signs of accumulation according to Money Flow indicators.

However, it's important to note that the current daily volume is slightly below the longer-term average. While this could simply reflect a normal fluctuation, if the trend of decreasing volume continues, it could be a signal that the bullish momentum is not backed by strong conviction. Lastly, the Relative Strength Index (RSI), which measures the speed and change of price movements, indicates that the stock is neither overbought nor oversold, providing no strong signal to sell or buy based solely on this indicator.

In summary, the technical indicators suggest that the stock has been performing strongly in the short term and is experiencing bullish momentum, as evidenced by the positive MACD and Money Flow indicators. Prospective investors should consider additional fundamental analysis and market context to validate these technical signals before making an investment decision.

The ‘Bull’ Perspective

Title: NVIDIA: A High-Performance Stock for the Future of Computing

Summary:

- Stellar Revenue Growth: NVIDIA's latest quarterly revenue surged to $18.12 billion, marking a 206% year-over-year increase, with significant contributions from its Data Center segment.

- Robust Financial Health: The company's gross margin expanded to 74% in Q3, and operating income skyrocketed, signaling strong operational efficiency and profitability.

- Strategic Capital Allocation: NVIDIA's aggressive share repurchase program and consistent dividend payments demonstrate a shareholder-friendly policy and confidence in long-term growth.

- Navigating Geopolitical Challenges: Despite concerns over new U.S. export restrictions, NVIDIA's diversified global presence and growth in other regions mitigate potential sales declines.

- Future-Proofing Through Innovation: NVIDIA's continuous investment in R&D and advancements in AI and gaming position it well to capitalize on future technology trends despite external risks.

Elaboration:

- Stellar Revenue Growth:

NVIDIA's revenue leap to $18.12 billion in the third quarter is nothing short of impressive. This 206% increase from the previous year is a testament to the company's dominance, particularly in the Data Center segment, which saw a 279% annual revenue rise. This growth is fueled by the robust demand for NVIDIA's HGX platform and AI applications. The Compute & Networking segment's 369% yearly increase further underscores the company's pivotal role in driving the future of high-performance computing. These numbers clearly illustrate NVIDIA's market leadership and the increasing reliance on its technology across various industries. - Robust Financial Health:

The company's gross margin expansion to 74% is a clear indicator of operational excellence and cost management. Coupled with an operating income surge to $10.42 billion for the quarter, up by a staggering 1633% year over year, NVIDIA's financial health is rock-solid. These figures reflect the company's ability to not only generate revenue but also to translate it efficiently into profits. Furthermore, the increase in interest income to $234 million due to higher yields adds to the financial robustness, providing NVIDIA with ample resources to navigate any market uncertainties. - Strategic Capital Allocation:

NVIDIA's return of $3.72 billion in share repurchases and payment of $99 million in cash dividends during Q3 FY2024 signal a strong commitment to enhancing shareholder value. This strategic capital allocation is a vote of confidence in the company's future prospects. By reducing the number of shares outstanding, NVIDIA is boosting earnings per share and, consequently, investor returns. Such financial stewardship is crucial, especially when considering the potential headwinds from geopolitical tensions and industry-wide challenges. - Navigating Geopolitical Challenges:

Despite the headwinds from the new U.S. export restrictions, NVIDIA's global reach and its strategic focus on other growing regions provide a cushion against the potential sales impact in China and Russia. The company's proactive approach to managing supply chain complexities and its ability to adapt to changing trade environments underscore its resilience. While the geopolitical landscape presents challenges, NVIDIA's diversified market penetration and innovative product pipeline ensure it remains on a growth trajectory. - Future-Proofing Through Innovation:

NVIDIA's commitment to research and development, evidenced by its trailblazing work in AI and the gaming sector, positions it at the forefront of future technological revolutions. Despite external risks such as economic downturns and regulatory changes, NVIDIA's innovation engine keeps it ahead of the curve. The company's forward-looking approach is crucial for long-term success, especially in an industry driven by rapid technological advancements. By staying at the cutting edge, NVIDIA ensures its products and services remain in high demand, future-proofing its business against any transient market shifts.

Conclusion:

In conclusion, NVIDIA's remarkable financial performance, strategic financial management, and innovative prowess make it a compelling investment opportunity. While no investment is without risk, NVIDIA's ability to navigate geopolitical tensions and its foresight in technology development are convincing arguments for its potential to continue thriving. As the company boldly addresses the challenges ahead, its strong foundation and visionary approach position it well to capitalize on the next wave of computing advancements, making NVIDIA a stock to watch in the ever-evolving tech landscape.

The ‘Bear’ Perspective

- Regulatory Risks and Geopolitical Tensions: Recent regulatory changes, especially in China, pose significant threats to NVIDIA's revenue streams, which could be severely impacted if sales continue to decline in this key market.

- Overreliance on Data Center Growth: NVIDIA's stellar performance is heavily reliant on its data center business, which experienced a 279% year-over-year increase, but this overreliance could be detrimental if market dynamics shift.

- Vulnerability to Supply Chain Disruptions: NVIDIA's complex supply chain and dependence on third-party suppliers for manufacturing components expose it to risks of disruption and shortages, which could lead to increased costs or inability to meet demand.

- Operational and Cybersecurity Risks: The company's operations are susceptible to cybersecurity threats and data breaches, which could result in significant financial and reputational damage.

- High Valuation Amid Market Volatility: NVIDIA’s current market valuation is steep, and with rising U.S. debt and calls for a special fiscal commission, market volatility could lead to a potential overcorrection in the stock's price.

Detailed Analysis:

- Regulatory Risks and Geopolitical Tensions:

The U.S. government's new licensing requirements that affect exports to several countries, including China and Russia, have introduced a significant level of uncertainty to NVIDIA's business outlook. China has been a substantial market for NVIDIA, contributing heavily to its revenue, and any reduction in sales here could have a profound impact on the company's financial performance. The recent news headline "Nvidia shares drop as China worries overshadow stellar forecast" underscores the market's concern over these regulatory challenges. Additionally, the company's 3,400 employees in Israel could be affected by ongoing geopolitical conflicts, which further adds to the operational risks faced by NVIDIA. - Overreliance on Data Center Growth:

While NVIDIA's Compute & Networking segment saw a massive 369% annual increase, such high growth rates may not be sustainable in the long term. The data center market is subject to rapid technological changes and intense competition. If NVIDIA fails to keep up with industry innovations or if competitors introduce more compelling offerings, it could result in a significant loss of market share and revenue. The company's future success is closely tied to its ability to maintain this momentum, which is by no means guaranteed. - Vulnerability to Supply Chain Disruptions:

NVIDIA's reliance on a complex supply chain and third-party suppliers makes it vulnerable to disruptions, which have been exacerbated by the global pandemic and ongoing trade disputes. The company's recent move to increase purchase obligations and add new suppliers indicates a reactive approach to supply chain management, which may not be sufficient to mitigate future risks. Supply chain issues can lead to product shortages, excess inventory, and increased costs, all of which can negatively impact NVIDIA's bottom line. - Operational and Cybersecurity Risks:

In an era where cyber threats are becoming more sophisticated, NVIDIA's exposure to potential cybersecurity incidents is a significant concern. A major data breach or cyber-attack could lead to substantial financial costs, erode customer trust, and damage the company's reputation. Given the increasing prevalence of such incidents across the tech industry, investors should be wary of the potential risks that NVIDIA faces in this domain. - High Valuation Amid Market Volatility:

NVIDIA's stock price has seen considerable growth, reflecting its strong financial performance. However, in a market environment where rising U.S. debt levels and the potential for a new fiscal commission are stoking concerns about economic stability, high valuations could be particularly vulnerable to corrections. This is compounded by the recent headlines such as "Big investors say US markets rally could prove short-lived," indicating a lack of confidence in the sustainability of current market valuations. NVIDIA's high valuation, therefore, may not be supported in the event of a market downturn, leading to significant potential losses for investors.

In conclusion, while NVIDIA Corporation has shown impressive financial growth, the risks associated with regulatory changes, geopolitical tensions, supply chain vulnerabilities, operational and cybersecurity threats, and market volatility cannot be ignored. Prudent investors should consider these factors carefully before making any investment decisions regarding NVIDIA's stock.

Comments ()