Liberty Energy Inc. (LBRT) , Large Cap AI Study of the Week

October 8, 2024

Weekly AI Pick from the S&P 500

Company Overview

Liberty Energy Inc. is an integrated energy services and technology company that specializes in hydraulic fracturing and related services for onshore oil and gas exploration in North America. The company operates in major North American shale basins, offering services such as wireline services, proppant delivery, and sand mining. Liberty Energy employs advanced technologies to improve operational efficiency and reduce emissions, including the development of digiFrac electric pumps and dual fuel dynamic gas blending fleets. The company has expanded its service offerings through strategic acquisitions such as PropX and Siren, strengthening its proppant delivery solutions. Additionally, it has launched Liberty Power Innovations to focus on alternative fuel solutions, particularly natural gas, to enhance its service portfolio.

The company is committed to environmental sustainability and adheres to ESG principles, integrating them into operations and community engagement. Liberty Energy invests heavily in intellectual property, holding around 500 patents, and prioritizes human capital development through initiatives like the Liberty Frac Academy. This focus on safety and leadership training has contributed to its reputation as one of the safest service providers in the industry. Liberty Energy is subject to various regulatory frameworks, including environmental, health, and safety regulations, and must comply with laws like the Clean Water Act and Clean Air Act. These regulations influence the company's operations and the demand for its services, as clients face pressures from federal and state regulations concerning greenhouse gas emissions and potential climatic impacts. Despite these challenges, Liberty Energy has developed long-term customer relationships and diversified its supply chain through strategic acquisitions, ensuring consistent service delivery and technological innovation. The company's strategic focus on next-generation technological advancements and alternative fuel solutions positions it for future growth in the energy services sector.

By the Numbers

Annual 10-K Report Summary for 2023:

- Revenue: $4.7 billion (14% increase from $4.1 billion in 2022)

- Net Income: $556.3 million (increase of $156.7 million from 2022)

- Operating Income: $760.6 million

- Operating Expenses: Increased by $334 million

- Costs of Services: Rose by 6% to $3.3 billion

- General and Administrative Expenses: Increased by 23% to $221.4 million

- Depreciation Expenses: Rose by 30% to $421.5 million

- Net Income Before Income Taxes: $734.9 million

- Income Tax Expense: $178.5 million (effective tax rate of 24.3%)

- EBITDA and Adjusted EBITDA: Approximately $1.2 billion each

- Cash Balance: Decreased by $6.9 million from the previous year

- Working Capital (excluding cash): Increased by $42.2 million

- Net Operating Cash Flow: $1.0 billion (a $484.2 million rise from 2022)

- Financing Expenditures: Increased by $293.5 million

- Share Repurchase Authorization: Increased to $750 million

- Purchase Obligations: $143.9 million due in the upcoming year

- Finance Lease Obligations: Estimated at $51.1 million

- Net Deferred Tax Liabilities: Reported at $102.3 million

Quarterly 10-Q Report Summary for Q2 2024:

- Revenue: $1.16 billion (decrease of $35.1 million or 2.9% from Q2 2023)

- Operating Income: Decreased by $64.6 million from Q2 2023

- Net Income: Decreased by $44.3 million from Q2 2023

- Service Costs: Increased marginally by $2.3 million to $835.8 million

- Depreciation, Depletion, and Amortization Expenses: Increased by $23.6 million

- Revenue (6-month period): Decreased by $224.1 million or 9.1% from 2023

- Loss on Disposal of Assets: $1.2 million (compared to a $3.7 million gain in 2023)

- Other Expenses, Net: Decreased by $5.6 million year-over-year

- Income Tax Expenses (6-month period): Decreased by $42.8 million from 2023

- EBITDA (Q2): Decreased to $511.0 million from $625.7 million in Q2 2023

- Adjusted EBITDA (Q2): Decreased to $518.0 million from $641.3 million in Q2 2023

- Net Cash Provided by Operating Activities: Decreased to $407.6 million from $444.4 million in 2023

- Cash and Cash Equivalents: Fell by $6.8 million

- Share Repurchases: $59.7 million worth of Class A Common Stock in H1 2024

- Purchase Commitments: $60.4 million payable in 2024, $13.0 million thereafter

- Finance Lease Obligations (3 and 6 months): Increased by $51.4 million and $81.5 million, respectively

- Effective Global Income Tax Rate (6-month period): Declined to 23.7% from 24.4% in 2023

- Income Tax Expenses (3 and 6 months): Decreased to $32.6 million and $59.0 million, respectively, from $47.3 million and $101.8 million in 2023

- Net Deferred Tax Liabilities: Unchanged at $102.3 million as of June 30, 2024

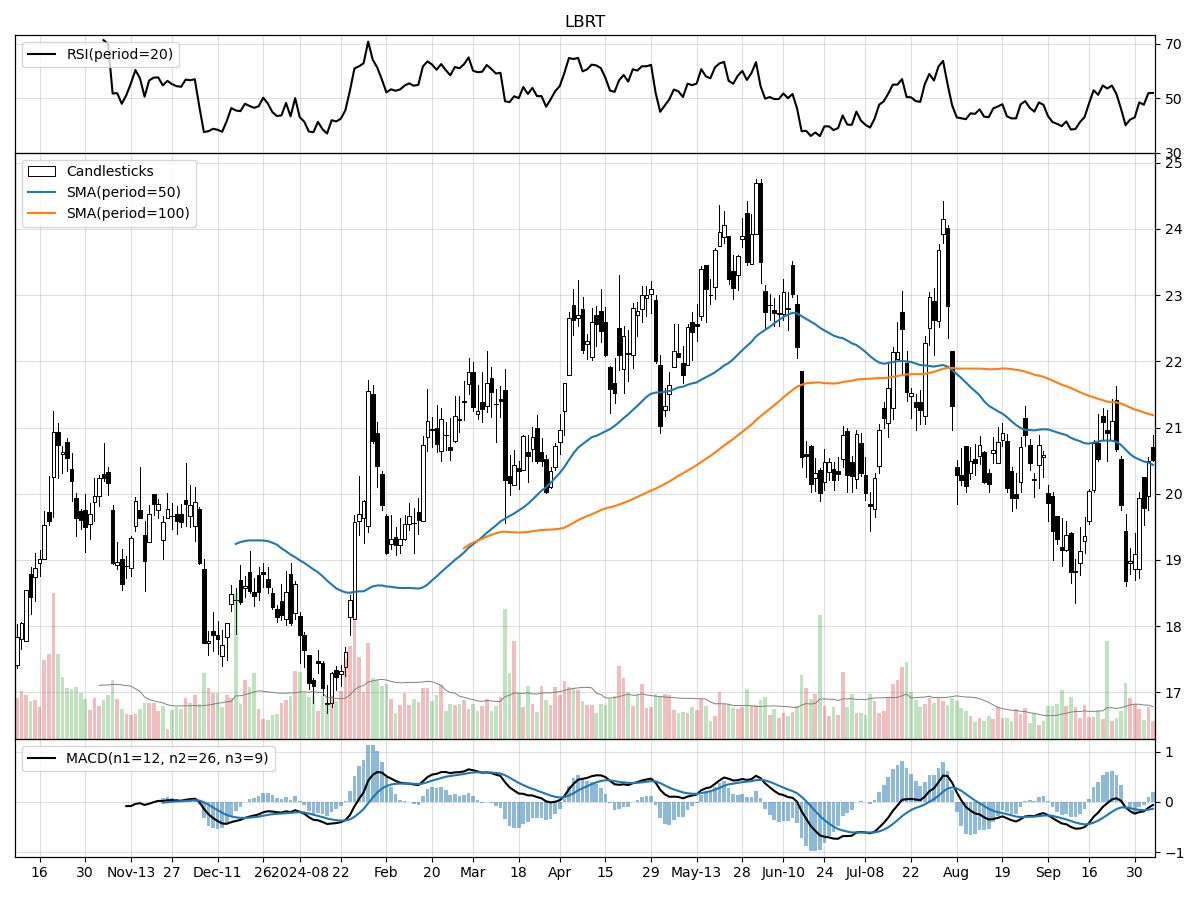

Stock Performance and Technical Analysis

The technical analysis of the stock at hand suggests a mixed outlook with both bullish and bearish signals. The current stock price of $20.51 signifies a moderate upward momentum, as it is 21% above its 52-week low, indicating that the stock has been recovering from its lowest point in the past year. However, it is also 16% below its 52-week high, which could suggest that the stock has faced resistance in reaching and surpassing previous peak levels. The 5.88% price increase over the last month shows short-term bullishness, while the stability over the last three months suggests consolidation, where the stock is neither gaining nor losing much value, indicating a period of indecision among investors.

Volume analysis is essential in confirming price trends. In this case, the recent daily volume is lower than the longer-term average, which may imply a lack of strong conviction in the stock's current price movements. A decrease in trading volume can sometimes precede a reversal or a slowdown in the current trend. Also, the Money Flow indicators are hinting at moderate selling pressure and distribution, which means that more investors are looking to sell their shares than buy, potentially capping the stock's upside in the short term.

The Moving Average Convergence Divergence (MACD) is a trend-following momentum indicator that shows the relationship between two moving averages of a stock's price. A bearish MACD of -0.13 indicates that the short-term momentum is less than the long-term momentum, suggesting that the stock could be entering a downtrend or losing strength in its current uptrend. This bearish signal should be considered in the context of the other indicators and overall market conditions.

In summary, while the stock has shown some positive price action relative to its 52-week period, the lower trading volume, selling pressure indicated by Money Flow, and a bearish MACD signal caution against outright bullishness. The mixed technical signals suggest that investors should closely monitor the stock for more definitive signs of direction before making a decision to invest. It might be prudent to look for additional fundamental analysis or wait for technical indicators to align more clearly with either a bullish or bearish trajectory before taking a position.

The ‘Bull’ Perspective

Upfront Summary:

- Strong Cash Position and Debt Management: Liberty Energy maintains a robust balance sheet with $241.2 million in available credit and a disciplined approach to debt management, ensuring financial flexibility in a volatile market.

- Strategic Share Repurchase Program: The company's commitment to shareholder returns is evident through its share repurchase program, with $59.7 million worth of Class A Common Stock bought back in the first half of 2024.

- Adaptive Business Model in Regulatory Landscape: Despite regulatory challenges, Liberty Energy has demonstrated adaptability, positioning itself to navigate the evolving environmental regulations while maintaining operational efficiency.

- Investment in Technological Advancements: Continuous investment in fleet capabilities and technological advancements keeps Liberty at the forefront of the hydraulic fracturing industry, providing a competitive edge.

- Resilience Amidst Geopolitical and Economic Uncertainties: The company's operational resilience and strategic positioning allow it to withstand the pressures of geopolitical tensions, labor market fluctuations, and potential federal rate cuts.

Elaboration on Key Points:

- Financial Stability and Credit Availability:

Liberty Energy's financial prudence is evident in its strong cash position and credit availability. With $241.2 million in remaining availability under its ABL Facility, the company demonstrates a strong liquidity profile that is crucial in an industry known for its cyclical nature and capital-intensive operations. This financial flexibility allows Liberty to weather downturns, invest in growth opportunities, and manage its debt effectively, with no material off-balance-sheet arrangements that could unduly strain its finances. The company's strategic financial management is particularly important given the recent decline in net income and the potential impact of rate cuts on the broader economy. - Shareholder Value Through Stock Repurchases:

Liberty Energy's strategic share repurchase program underscores its commitment to enhancing shareholder value. By repurchasing $59.7 million of its Class A Common Stock in the first half of 2024, the company is signaling confidence in its intrinsic value and future prospects. This move not only supports the stock price by reducing the number of shares outstanding but also reflects the company's disciplined capital allocation strategy. Share buybacks can be particularly attractive to investors, especially in a market environment where other forms of yield, such as dividends, might be under pressure due to economic headwinds. - Navigating the Regulatory Environment:

The oil and gas sector is highly sensitive to regulatory changes, especially those related to environmental protection and hydraulic fracturing. Liberty Energy's ability to adapt to these changes is crucial for its continued success. Despite the risk of new restrictions and increased costs due to regulatory pressures, Liberty has maintained operational efficiency and compliance. The company's proactive approach to managing environmental concerns, such as water usage and emissions, positions it well to handle potential future regulations, ensuring its services remain in demand. - Technological Edge in a Competitive Market:

Investing in technology is key to staying competitive in the hydraulic fracturing industry. Liberty Energy's increase in depreciation, depletion, and amortization expenses by $23.6 million reflects its commitment to enhancing fleet capabilities and adopting innovative technologies. These investments not only improve operational efficiency but also reduce environmental impact, aligning with the industry's shift towards more sustainable practices. By leveraging advanced technologies, Liberty can offer superior services to its clients, differentiating itself from competitors and capturing a larger market share. - Withstanding External Pressures:

Liberty Energy's operational resilience is tested against a backdrop of geopolitical tensions, labor market changes, and shifts in monetary policy. The recent strong labor-market data, with 254,000 jobs added versus the forecasted 150,000, and the subsequent impact on Federal Reserve rate cuts, could signal a tightening financial environment. However, Liberty's sound financial structure and strategic foresight equip it to navigate these uncertainties. The company's ability to maintain a stable operational footing, even amidst potential disruptions from events like the East Coast port strike and Middle Eastern geopolitical tensions, speaks to its robust risk management and contingency planning.

In conclusion, Liberty Energy Inc. presents a compelling investment case as it demonstrates financial strength, shareholder-centric policies, adaptability to regulatory shifts, technological innovation, and resilience in the face of economic and geopolitical challenges. The company's strategic maneuvers and operational agility position it well to capitalize on future growth opportunities within the evolving energy landscape.

The ‘Bear’ Perspective

- Regulatory Risks and Compliance Costs: Liberty Energy Inc. faces significant regulatory risks that could lead to increased compliance costs and operational restrictions, particularly concerning hydraulic fracturing.

- Dependence on Volatile Commodity Prices: The company's financial performance is highly sensitive to volatile oil and gas prices, which can lead to unpredictable capital spending by customers and affect the company's liquidity.

- Operational Challenges and Environmental Scrutiny: Operational challenges, such as obtaining permits and adapting to environmental regulations, could disrupt Liberty Energy's services and lead to revenue loss.

- ESG Pressures and Market Shifts: As the market increasingly focuses on Environmental, Social, and Governance (ESG) issues, Liberty Energy may face reduced demand for its services and increased costs due to a shift towards lower-carbon energy sources.

- Technological Advancements and Competition: Keeping up with rapid technological advancements in hydraulic fracturing is essential for Liberty Energy to maintain its market share, requiring continuous investment and innovation.

In-Depth Analysis:

- Regulatory Risks and Compliance Costs

Liberty Energy Inc. operates in an industry that is currently under intense regulatory scrutiny, particularly in the area of hydraulic fracturing. The potential for new federal, state, and local regulations poses a significant risk to the company's operations. For instance, the Biden administration's suspension of new oil and gas leases on federal lands and the potential increase in royalty rates could lead to a decline in demand for Liberty's services. If the EPA imposes stricter emission and water management standards, the company could face increased compliance costs, which in 2024 may already be in the tens of millions, squeezing profit margins and reducing the capital available for other operational needs. Legal battles over environmental reviews and lease sales could further complicate operations and lead to additional expenses and delays. - Dependence on Volatile Commodity Prices

Liberty Energy's financial health is closely tied to the fluctuating prices of oil and natural gas. These commodity prices are subject to global economic forces, geopolitical events, and shifts in supply and demand. A downturn in commodity prices, as seen in previous years, can lead to rapid declines in customer capital spending, directly impacting Liberty's bottom line. For example, a 10% drop in oil prices could precipitate a commensurate or greater percentage decline in Liberty's revenue, given the company's revenue decrease of $224.1 million, or 9.1%, from the previous year, as noted in their financial statements. - Operational Challenges and Environmental Scrutiny

Liberty Energy must navigate complex permitting processes and adapt to an evolving regulatory landscape, which could hinder its ability to operate efficiently. The company's operations and its customers' activities could be significantly impacted by restrictions on water usage for hydraulic fracturing, which is a critical input for the company's services. Moreover, any accidents or environmental hazards could lead to costly disruptions and damage the company's reputation. For example, a single operational mishap resulting in environmental damage could result in millions in cleanup costs and fines, not to mention the potential for long-term revenue loss due to damaged customer relationships. - ESG Pressures and Market Shifts

The growing emphasis on ESG issues presents a dual challenge for Liberty Energy. On one hand, the company may incur additional costs to meet rising ESG standards and investor expectations, which may not be fully quantifiable at present but are likely to be substantial. On the other hand, the global shift towards renewable energy sources could reduce long-term demand for oil and gas services. For instance, a 1% shift in energy market share from fossil fuels to renewables could represent millions in lost revenue for companies like Liberty Energy. - Technological Advancements and Competition

The oil and gas services industry is highly competitive, and technological innovation is a key differentiator. Liberty Energy must continually invest in new technologies to improve efficiency and reduce costs. Failure to keep up with competitors' technological advancements could result in a loss of market share. For example, if a competitor develops a technology that reduces fracking costs by 20%, Liberty Energy would need to match this to stay competitive, potentially costing the company millions in research and development.

In conclusion, while Liberty Energy Inc. has been a player in the oil and gas services industry, the combination of regulatory risks, commodity price volatility, operational challenges, ESG pressures, and the need for continuous technological innovation presents a compelling case for investors to exercise caution. The potential for increased costs, revenue instability, and market shifts make Liberty Energy a less attractive investment option in the current economic and regulatory climate.

Comments ()