Gilead Sciences Inc. (GILD), Large Cap AI Study of the Week

April 23, 2024

Weekly AI Pick from the S&P 500

Company Overview

Gilead Sciences, Inc. is a global biopharmaceutical company that specializes in the development and distribution of innovative treatments for life-threatening diseases such as HIV, hepatitis, COVID-19, and cancer. It has a strong portfolio of HIV treatments, including Biktarvy and the newly launched Sunlenca for resistant HIV-1 infections. Gilead also markets Veklury for COVID-19 and has a presence in the oncology sector with therapies like Yescarta, Tecartus, and Trodelvy. The company's products are sold worldwide, with a significant portion of U.S. sales through large wholesalers.

The company is actively engaged in research and development, focusing on viral diseases, oncology, and inflammatory diseases. It has made strategic transactions to enhance its portfolio, such as collaborations with Assembly Biosciences and Tentarix Biotherapeutics, and a co-development deal with Arcellx. Gilead also holds numerous patents and continues to seek protection for its innovations, although it faces risks related to patent enforceability and litigation.

Manufacturing is carried out both in-house and through third-party contractors, with a focus on maintaining high-quality standards and securing reliable raw material sources. Gilead is committed to diversity and inclusion, with a workforce that is over half female and ethnically diverse in the U.S. The company offers competitive benefits, focuses on professional development, and is dedicated to corporate social responsibility, though it acknowledges that its ESG goals are subject to change.

By the Numbers

Annual 10-K Report Summary:

- Total revenues: $27.1 billion (1% decrease from $27.3 billion in 2022)

- Veklury sales: 44% decrease

- HIV product sales: 6% increase

- Biktarvy sales: 14% increase

- Oncology sales: 37% increase

- Cell Therapy sales: 28% increase

- Liver Disease product sales: 1% decrease

- Net income: $5.7 billion (23% increase)

- Diluted earnings per share: $4.50 (24% increase)

- Gross-to-net deductions: 38% of gross product sales

- Foreign exchange impact: $224 million negative impact

- Cost of goods sold: 15% increase

- Research and development expenses: 15% increase ($741 million increase)

- Acquired IPR&D expenses: $1.2 billion

- Selling, general, and administrative expenses: $417 million increase

- Cash, cash equivalents, and marketable debt securities: $8.4 billion

- Net cash from operating activities: $1.1 billion decrease from 2022

- Debt repayments: $1.5 billion

- Dividends: $3.7 billion

- Stock repurchases: $1.4 billion

- Impairment charge recognized in 2022: $2.7 billion

Quarterly 10-Q Report Summary:

- Total revenues: $20 billion (1% increase)

- Net income: $4.2 billion (44% increase)

- Diluted earnings per share: $3.37 (44% increase)

- Foreign exchange impact: $191 million negative impact over nine months

- Product gross margin: Decline due to Trodelvy costs

- Research and development expenses: 27% increase for the quarter, 26% increase for nine months

- Acquired IPR&D expenses: $56 million payment for August 2023 collaboration

- Selling, general, and administrative expenses: 8% increase for the quarter, 23% increase for nine months

- Effective tax rate: Decrease due to agreement with tax authority and prior acquisition tax impact

- Cash, cash equivalents, and marketable debt securities: $8.0 billion

- Net cash provided by operating activities: $5.8 billion (decrease)

- Cash used in investing activities: $1.5 billion (decrease)

- Cash used in financing activities: $4.0 billion (decrease)

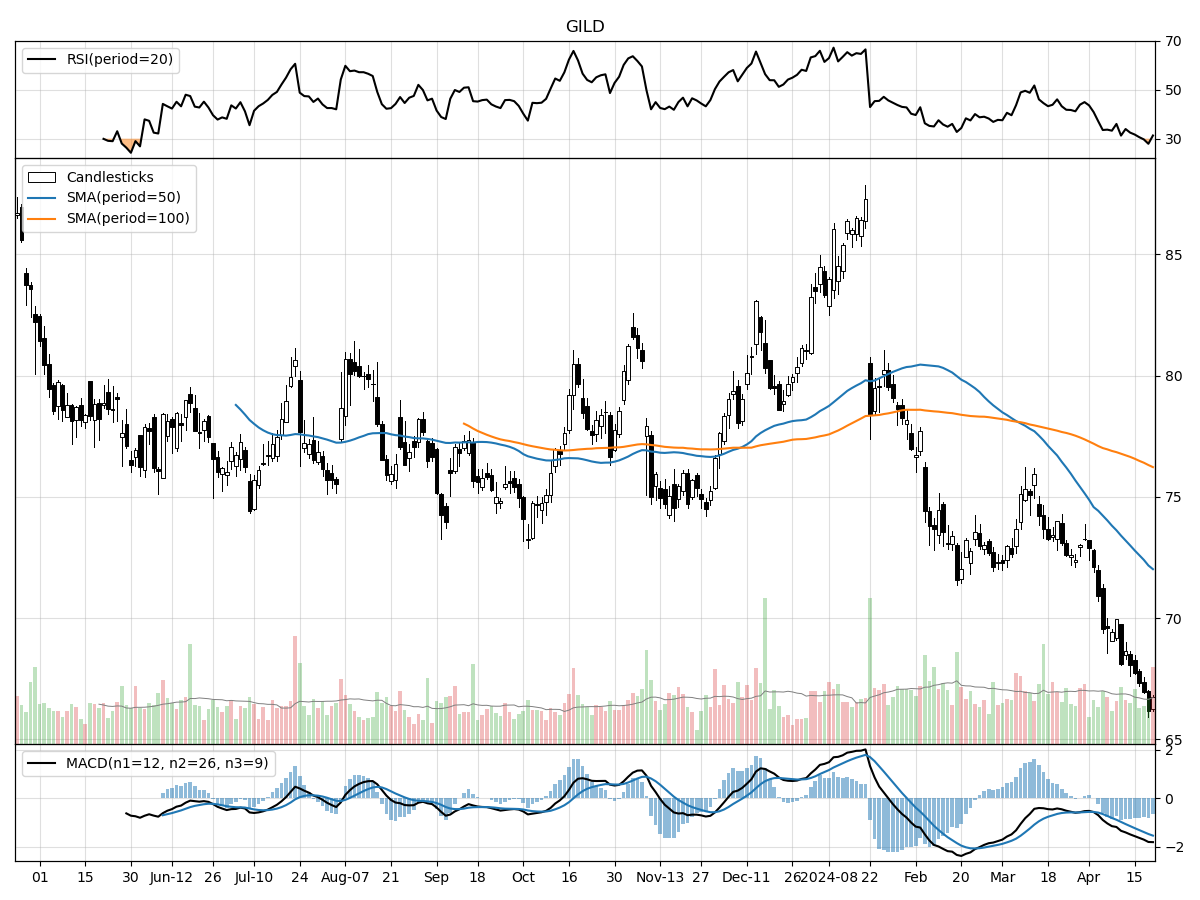

Stock Performance and Technical Analysis

The current technical analysis of the stock suggests a bearish sentiment in the market. The stock price is currently unchanged from its 52-week low, indicating that the market has not found a reason to increase the valuation from its lowest point in the past year. Furthermore, at 23% below its 52-week high, it seems that the stock has lost a significant portion of the gains it might have accrued, pointing towards a shift in investor confidence or underlying company performance issues.

The trading volume provides mixed signals. The recent daily volume is slightly higher than the longer-term average, which can indicate increased interest in the stock. However, this interest doesn't necessarily translate into buying pressure, as indicated by the price declines of 8.06% over the last month and 16.79% over the last three months. This suggests that the increased volume could be associated with selling activity rather than buying.

The Money Flow indicators support this view, showing that the stock is under heavy selling pressure and is experiencing distribution, meaning that the stock is being sold off more than it is being accumulated. The Moving Average Convergence Divergence (MACD) indicator reinforces the negative outlook, as a bearish MACD at -1.54 suggests that the short-term momentum is lower than the long-term momentum, indicating a downward price trend.

Given these indicators, caution is advised for investors considering this stock. The current momentum and selling pressure suggest that the stock may continue to face downward pressure in the near term. Potential investors may want to wait for signs of a reversal, such as bullish MACD crossover or improvements in Money Flow indicators, before considering entry. As always, it's important to consider these technical indicators alongside fundamental analysis, which includes evaluating the company's financial health, management, industry conditions, and growth prospects.

The ‘Bull’ Perspective

Investing in Gilead Sciences (GILD): A Strategic Opportunity Amidst Market Volatility

Executive Summary:

- Robust Financial Performance: Gilead has demonstrated a 44% increase in net income to $4.2 billion, with a corresponding EPS growth, showcasing strong profitability.

- Expanding Therapeutic Portfolio: The company's commitment to expanding its treatment offerings, particularly in oncology and antiviral therapies, positions it for future growth.

- Strategic Management of Debt: Gilead's strategic issuance and repayment of debt enhance its financial stability and creditworthiness.

- Innovative Research and Development: A 27% increase in R&D spending underscores Gilead's dedication to innovation, which is critical for long-term success in the biopharmaceutical industry.

- Diversification and Resilience: Despite reliance on HIV product sales, Gilead's diversification into other therapeutic areas mitigates risk and ensures resilience against market fluctuations.

Elaboration on Key Points:

- Robust Financial Performance

Gilead's financials are a beacon of profitability in an industry that demands constant innovation and adaptation. The company's net income leap to $4.2 billion, a 44% surge, is not just a number – it's a testament to its operational efficiency and market acumen. The diluted earnings per share (EPS) growth mirrors this trend, indicating a solid return on investment for shareholders. This financial prowess is particularly impressive given the broader market's recent softening, demonstrating Gilead's ability to thrive even when others falter. Despite a modest 1% increase in total revenues, the significant jump in net income reflects Gilead's effective cost management and strategic financial planning. - Expanding Therapeutic Portfolio

Gilead's aggressive pursuit of new therapeutic avenues, especially in the lucrative fields of oncology and antiviral research, is setting the stage for future revenue streams. The company's investment in research partnerships and the expansion of indications for existing treatments, such as Trodelvy, are forward-thinking moves that could pay dividends as these markets grow. While the recent decline in Veklury sales due to a drop in COVID-19 hospitalizations presents a challenge, Gilead's broadening portfolio provides a hedge against such fluctuations. This diversification is crucial for sustaining growth, particularly when considering the 67% revenue dependence on HIV treatments and the associated risks of market competition and treatment protocol changes. - Strategic Management of Debt

Gilead's savvy financial maneuvers, including the issuance of $2.0 billion in senior unsecured notes and the repayment of $2.25 billion, reflect a strategic approach to debt management. This not only optimizes the company's capital structure but also signals to investors a commitment to maintaining fiscal responsibility. In an environment where interest rates are on the rise, as indicated by the increase in 2- and 10-year U.S. Treasury yields, Gilead's conservative approach to debt is reassuring and may protect the company from potential interest rate shocks. - Innovative Research and Development

The company's 27% increase in R&D expenditure is a bold statement of its intent to remain at the forefront of biopharmaceutical innovation. This commitment is critical in an industry where the next breakthrough can redefine market leadership. Gilead's focus on advancing clinical trials and nurturing its pipeline ensures it stays competitive and ready to capitalize on new opportunities. The potential risks associated with clinical trials, such as delays and safety issues, are inherent in the industry, but Gilead's substantial investment in R&D indicates a proactive stance in mitigating these risks through thorough research and development processes. - Diversification and Resilience

Gilead's strategic diversification into areas beyond its traditional HIV stronghold demonstrates a keen awareness of the need for resilience in a volatile market. This approach not only spreads risk but also positions the company to tap into new revenue sources as they emerge. The recent softening of markets and the pullback in growth and interest-rate-sensitive sectors underscore the importance of a well-rounded portfolio. Gilead's foray into other therapeutic areas, such as oncology and cell therapy, provides a buffer against the HIV market's uncertainties and competitive pressures, ensuring the company's stability and continued relevance in the healthcare sector.

Conclusion:

In conclusion, Gilead Sciences presents a compelling investment case. Its robust financial performance, strategic debt management, and aggressive investment in R&D are indicative of a company that is not only weathering current market storms but also positioning itself for future success. Gilead's diversification strategy further mitigates risks, making it a resilient player in the biopharmaceutical space. For investors seeking a blend of stability, innovation, and growth potential, GILD stands out as a prudent choice amidst market volatility.

The ‘Bear’ Perspective

Why Investors Should Exercise Caution with Gilead Sciences (GILD) Stock

Summary:

- Overreliance on HIV Drug Sales: GILD's revenue is heavily dependent on its HIV treatments, which contribute approximately 67% to its total revenue, making it vulnerable to market changes and competitive pressures.

- Uncertain Future of Veklury (Remdesivir): The sales trajectory of Gilead's COVID-19 treatment is unpredictable due to variable infection rates and the emergence of competing treatments, posing inventory risks.

- Regulatory and Pricing Pressures: Legislative actions and pricing pressures, particularly from the Inflation Reduction Act of 2022, could constrain Gilead's pricing power and profitability.

- Manufacturing and Supply Chain Risks: Manufacturing complexities and supply chain disruptions can lead to product shortages, recalls, or regulatory setbacks, impacting Gilead's ability to deliver products and generate revenue.

- Intellectual Property and Legal Risks: Patent expirations, litigation, and challenges to intellectual property rights threaten Gilead's market exclusivity and may result in substantial financial obligations.

Elaboration on Points:

- Overreliance on HIV Drug Sales:

Gilead Sciences' financial health is heavily tied to its HIV drug portfolio, which is responsible for two-thirds of its revenue stream. While this has historically been a strong suit for Gilead, with 67% reliance, it also poses a significant risk. Changes in treatment protocols, competition from generic drug manufacturers, or breakthroughs by competitors could drastically reduce Gilead's market share. Moreover, the recent modest 1% increase in total revenues to $20 billion for the first nine months of 2023 indicates a potential plateauing of growth in this segment, which should be a cause for concern among investors considering the company's limited diversification. - Uncertain Future of Veklury (Remdesivir):

The sales of Veklury, Gilead’s antiviral drug for COVID-19, have been a substantial contributor to the company's revenue during the pandemic. However, with the decline in COVID-19 hospitalizations and the availability of vaccines and other treatments, the future demand for Veklury is highly uncertain. This unpredictability could lead to either excess inventory, which was a concern in past quarters, or shortages if there is an unexpected surge in cases, both of which can adversely affect the company's financials. The decline in sales of Veklury and Liver Disease treatments adds to the uncertainty surrounding Gilead's revenue stability. - Regulatory and Pricing Pressures:

The pharmaceutical industry is facing increasing pricing scrutiny from the government and the public. The Inflation Reduction Act of 2022 and other regulatory measures could further restrict Gilead's ability to set prices, potentially diminishing profit margins. Rebates and discounts, particularly to government programs such as Medicaid and the 340B program, have already impacted Gilead's financial outcomes. These pressures, combined with the risk of increased rebates and legislative changes, could significantly affect the company's bottom line. - Manufacturing and Supply Chain Risks:

Gilead's reliance on third-party manufacturers and the complexity of its cell therapy products, such as Yescarta and Tecartus, introduce substantial risks. Manufacturing issues could lead to shipment delays, product recalls, or clinical and regulatory delays, as evidenced by the product gross margin suffering from costs associated with the newly approved Trodelvy indication. Furthermore, global supply chain disruptions could impact the company's ability to maintain consistent revenue streams, a concern that has been exacerbated by recent global events. - Intellectual Property and Legal Risks:

Intellectual property rights are the lifeblood of biopharmaceutical companies like Gilead. With patent litigation and the potential for early loss of exclusivity, Gilead faces the risk of reduced market protection for its key products. The company has already had to navigate complex patent landscapes, and any adverse outcomes in ongoing or future litigation could lead to significant financial obligations or the need to find costly licensing agreements or alternative technologies. This risk is compounded by the fact that Gilead's product sales have seen mixed results, with some segments growing while others, such as Veklury, are declining.

Conclusion:

Considering these factors, investors should proceed with caution regarding Gilead Sciences stock. The company's overreliance on its HIV portfolio, the volatile future of Veklury sales, regulatory and pricing headwinds, manufacturing and supply chain vulnerabilities, and intellectual property challenges all present significant risks that could impede Gilead's financial performance and stock value. While the company has shown resilience and an ability to navigate a complex healthcare landscape, these risks are substantial enough to warrant a conservative approach to investment in GILD stock at this time.

Comments ()