EOG Resources (EOG), Large Cap AI Study of the Week

February 6 , 2024

Weekly AI Pick from the S&P 500

Company Overview

EOG Resources, Inc., a U.S.-based company founded in 1985, is heavily involved in the exploration, development, production, and marketing of crude oil, natural gas liquids (NGLs), and natural gas. Its operations are primarily focused in the United States, with 99% of its estimated net proved reserves located domestically as of the end of 2022, and it has a smaller presence in Trinidad. EOG's business strategy emphasizes cost control, technological advancements in drilling, and improving reserve recovery rates. The company's major U.S. activities are in the Delaware Basin, South Texas, and the Rocky Mountains, and it has international interests offshore Trinidad and in Australia, with recent exits from Oman and Canada due to insufficient returns.

In Trinidad, EOG's production includes 180 MMcfd of natural gas and 0.6 MBbld of crude oil, and the company is expanding its infrastructure and drilling operations. It has also acquired full interest in an Australian offshore block, WA-488-P, and is preparing for exploratory drilling pending regulatory approval. EOG's marketing strategy for its U.S. production involves pipeline sales and exports, while in Trinidad, it has renegotiated its gas sales contract for better terms.

Financially, EOG relies on its U.S. operations, especially the Eagle Ford Play and Delaware Basin. The company employs around 2,850 people and is recognized for its workplace environment, offering competitive compensation, benefits, and a focus on employee development and diversity. In a competitive oil and gas industry, EOG contends with larger integrated companies and alternative energy sources.

EOG operates under strict regulations that impact drilling, lease management, and royalty payments and faces oversight from federal agencies. New policies, such as the Inflation Reduction Act of 2022, could affect royalty rates and operations. The company is also subject to environmental regulations, including those addressing climate change and methane emissions, which have not yet significantly impacted its financials or operations but could lead to future compliance costs. Hydraulic fracturing, a key part of EOG's operations, is under increasing regulatory scrutiny, and further regulations could increase operational costs. Internationally, EOG navigates various environmental regulations that could materially affect its operations and compliance costs. Lastly, EOG's revenue is sensitive to fluctuating energy prices, which can significantly impact its financial performance.

By the Numbers

Annual 10-K Report Summary (2022):

- Net income: $7,759 million (up from $4,664 million in 2021)

- Average crude oil price: $94.23 per barrel (39% increase)

- Average natural gas price: $6.64 per MMBtu (72% increase)

- Total estimated net proved reserves: 4,238 MMBoe (up 491 MMBoe)

- Debt-to-capitalization ratio: 17% (down from 19% in 2021)

- Wellhead revenues: $22.796 billion (48% increase)

- Operating revenues: $25.702 billion

- Dividends paid in 2022: $5.1 billion

- Wellhead crude oil and condensate revenues: $16,367 million (47% increase)

- NGLs revenues: $2,648 million (46% increase)

- Wellhead natural gas revenues: $3,781 million (55% increase)

- Net losses on financial commodity derivative contracts: $3,982 million (up from $1,152 million in 2021)

- Operating expenses: $15,736 million (up $3,196 million from previous year)

- Net cash from operating activities: $11,093 million

- Exploration and development expenditures: $4,931 million

Quarterly 10-Q Report Summary (First Nine Months of 2023):

- Crude oil price decrease: 21%

- Natural gas price decrease: 60%

- Operating revenues (Q3 2023): $6,212 million (down 18% from $7,593 million in Q3 2022)

- Wellhead revenues (Q3 2023): $4,635 million (23% decrease)

- Debt-to-total capitalization ratio: 12%

- Cash and cash equivalents: $5.3 billion

- Available credit facility: $1.9 billion

- Planned cash returns to stockholders for FY 2024: 70%

- Quarterly dividend increase: $0.91 per share

- Special dividend: $1.50 per share

- Share repurchases (Q3 2023): 6.2 million shares for $671.1 million

- Wellhead crude oil and condensate revenues (Q3 2023): Decrease of 10%

- NGL revenues (Q3 2023): Decrease of 28%

- Natural gas revenues (Q3 2023): Decrease of 66%

- Net gain on financial commodity derivative contracts (Q3 2023): $43 million

- Operating expenses reduction (Q3 2023): $274 million

- Operating revenues decrease (First Nine Months of 2023): 6% or $1,154 million

- Lease and well expenses increase: $99 million

- DD&A expenses decrease: $102 million

- G&A and exploration costs increase: $34 million and $25 million, respectively

- Cash balance decrease: $646 million

- Net cash from operating activities increase: $587 million

- Net cash used in investing activities increase: $1,182 million

- Total expenditures (First Nine Months of 2023): $5,184 million

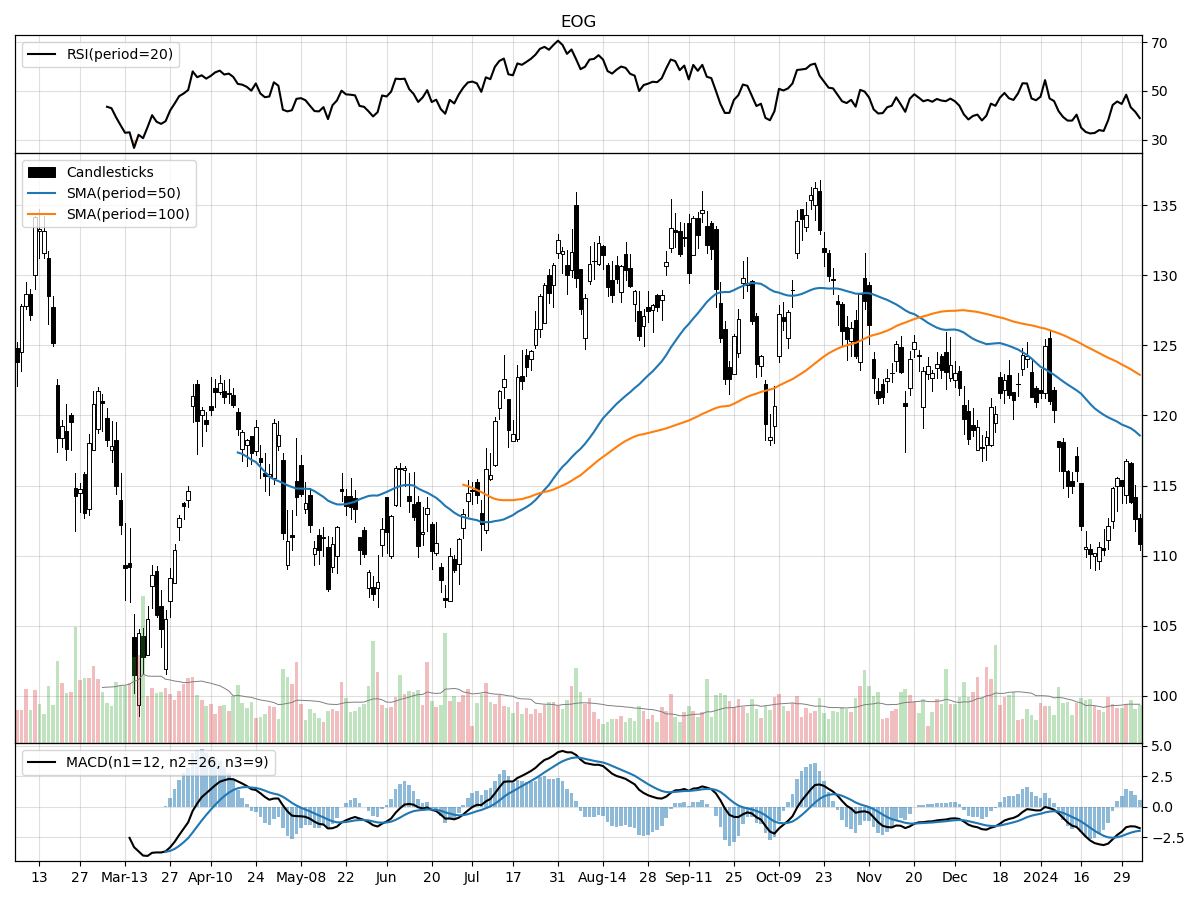

Stock Performance and Technical Analysis

When conducting a technical analysis of a stock, traders and analysts use various indicators to assess the stock's momentum, trend, and potential reversal points. Here's an analysis based on the provided technical data:

The current stock price of $110.85 is 9% above the 52-week low and 18% below the 52-week high, which suggests the stock has retreated from its peak levels and may be trading in the middle of its 52-week range. A price decline of about 7.92% in the last month and 9.61% over the last three months indicates that the stock has been under some selling pressure recently. This is further supported by the Money Flow indicators that suggest moderate selling pressure. However, the Money Flow indicators also hint at accumulation, which can be a signal of increased buying interest at lower prices. This could be a sign that some investors are seeing value at these levels and could potentially support a price stabilization or an upward move if this trend continues.

The Relative Strength Index (RSI) indicates that the stock is modestly oversold. An RSI below 30 typically suggests that a stock may be oversold and thus could be due for a rebound as sellers exhaust themselves, but the term "modestly" indicates it may not have reached an extreme level that often precedes a strong reversal. On the other hand, the Moving Average Convergence Divergence (MACD) is bearish with a reading of -1.95, which points to downward momentum and might imply that the stock could continue to decline in the short term if this trend persists.

Overall, the mixed signals from these technical indicators require careful consideration. Accumulation signs and an oversold condition could be bullish signals, but the bearish MACD and the recent price decline suggest caution. Investors and traders should weigh these indicators against the stock's overall trend, market conditions, and any potential catalysts for price movement. It may also be prudent to look for confirmation from other technical patterns or signals before making an investment decision. As with any investment, it's crucial to align technical analysis with risk management strategies and personal investment goals.

The ‘Bull’ Perspective

EOG Resources: A Resilient Energy Powerhouse in a Volatile Market

Upfront Summary:

- Impressive Financial Health: EOG Resources boasts a low debt-to-total capitalization ratio of 12%, with $5.3 billion in cash and $1.9 billion available from its credit facility, signaling strong financial resilience.

- Commitment to Shareholder Returns: Despite market challenges, EOG is increasing cash returns to stockholders from 60% to 70% in fiscal 2024, including a consistent dividend policy with a recent hike to $0.91 per share and a special dividend of $1.50 per share.

- Strategic Operational Advantages: EOG's focus on horizontal drilling and efficiency initiatives has led to a 4% increase in production, mainly from the Permian Basin, showcasing its operational prowess.

- Robust Liquidity Position: With significant liquidity and a proactive approach to capital management, EOG has repurchased 6.2 million shares for $671.1 million, underpinning its confidence in long-term value.

- Proactive Adaptation to Market Conditions: EOG has demonstrated agility in adjusting to the tumultuous energy market, mitigating the impacts of commodity price volatility and inflationary pressures through cost reduction and efficiency improvements.

Elaboration on Key Points:

- Impressive Financial Health:

EOG Resources stands out as a bastion of financial stability in the often-tumultuous oil and gas sector. With a debt-to-total capitalization ratio at a mere 12%, the company has managed to maintain a level of indebtedness that is the envy of its peers. This conservative financial posture is further bolstered by its significant cash reserves amounting to $5.3 billion and an additional $1.9 billion of untapped credit. This positions EOG to weather the volatility of oil and gas markets, where recent headlines have seen crude oil prices drop by 21% and natural gas by 60% compared to last year, without compromising on its growth trajectory or shareholder commitments. - Commitment to Shareholder Returns:

In a period where many companies are tightening their belts, EOG is doubling down on its promise to enrich its investors. The company's plan to increase cash returns to stockholders to 70% in the coming fiscal year is a bold statement of confidence. This is not mere rhetoric; it is backed by tangible increases in dividends to $0.91 per share and the issuance of a substantial $1.50 per share special dividend. These shareholder-friendly moves are particularly compelling given the backdrop of a challenging market environment, demonstrating EOG's ability to not just survive but thrive and share the spoils of its success. - Strategic Operational Advantages:

EOG's strategic operational initiatives have borne fruit, with a 4% uptick in production volumes, primarily from the prolific Permian Basin. This increase comes despite the broader industry grappling with price drops and cost pressures. EOG's emphasis on horizontal drilling and self-sourcing sand for hydraulic fracturing are just a couple of examples of how the company has honed its operational efficiency. These advancements are critical for maintaining profitability and competitive advantage, especially when market conditions are not favorable. - Robust Liquidity Position:

The company's robust liquidity position is a testament to its shrewd financial management. EOG's share repurchase program, which saw the buyback of 6.2 million shares for $671.1 million, is not only a sign of self-assurance but also a catalyst for enhancing shareholder value. With $4.3 billion remaining for future repurchases, EOG is poised to continue this trend, which could be a boon for stock prices, especially when considering the current underperformance relative to historical highs. - Proactive Adaptation to Market Conditions:

EOG's ability to adapt proactively to fluctuating market conditions is commendable. The company has successfully implemented cost reduction measures, decreasing operating expenses by $274 million in the third quarter of 2023. This agility is crucial in a landscape where recent Federal Reserve decisions to hold interest rates steady could create both opportunities and challenges for the energy sector. EOG's strategic initiatives, such as its downhole motor and self-sourced sand programs, have helped mitigate the adverse effects of inflation and supply chain disruptions, ensuring the company remains on solid footing.

In conclusion, the combination of EOG Resources' strong financial health, unwavering commitment to shareholder returns, strategic operational efficiencies, robust liquidity, and proactive market adaptation make it a compelling investment opportunity. Even as the company navigates the risks inherent in the energy sector, including commodity price volatility, regulatory changes, and environmental concerns, EOG's strategic positioning and financial prudence suggest it is well-equipped to continue delivering value to its shareholders. The company's resilience in the face of adversity is not just a testament to its current strength but also an indicator of its potential for sustained success in the years to come.

The ‘Bear’ Perspective

Bearish Outlook on EOG Resources Inc.: Why Investors Should Exercise Caution

Upfront Summary:

- Decline in Commodity Prices: Recent drops in crude oil by 21% and natural gas by 60% compared to 2022 significantly impact EOG's revenue streams.

- Operational and Market Risks: Inflation and supply chain disruptions increase operating costs, while market volatility poses risks to financial stability.

- Regulatory and Environmental Pressures: Stricter environmental regulations and the transition to sustainable energy sources could lead to higher compliance costs and reduced demand for EOG's products.

- Technological and Execution Risks: EOG's ambitious net-zero GHG emissions target by 2040 hinges on unproven technologies and could lead to increased expenses if not executed properly.

- Geopolitical Tensions and Economic Indicators: Global geopolitical instability and mixed economic signals from the Fed and labor market create an uncertain environment for oil and gas investments.

Elaboration on Points:

- Decline in Commodity Prices:

EOG Resources has faced a challenging market with crude oil and natural gas prices experiencing significant declines. The 21% drop in crude oil and a staggering 60% in natural gas prices from the previous year have led to an 18% decrease in operating revenues, down to $6,212 million in Q3 of 2023. EOG's wellhead revenues also took a hit, with a 23% reduction to $4,635 million. These numbers reflect the volatility and unpredictability of commodity markets, which directly affect the company's bottom line. Investors should be wary of the potential for continued price instability, which could further strain EOG's financial performance. - Operational and Market Risks:

The oil and gas industry is not immune to broader market trends, and EOG is facing increased operational costs due to inflation and supply chain challenges. Despite efficiency initiatives, the company reported a decrease in cash balance by $646 million over nine months in 2023. Moreover, with a volatile market and the potential for decreased investor interest in fossil fuels, EOG could encounter difficulties in securing capital at reasonable costs. The company's low debt-to-total capitalization ratio of 12% is a positive sign, but market conditions could quickly change the capital access landscape, affecting EOG's ability to maintain or expand operations. - Regulatory and Environmental Pressures:

EOG's operations are increasingly coming under scrutiny due to environmental concerns. The shift towards sustainable energy and the imposition of stricter regulations could result in reduced product demand and higher operational costs. For instance, the company's commitment to achieving net-zero Scope 1 and Scope 2 GHG emissions by 2040 will require substantial investment and expose it to risks associated with regulatory changes. Investors must consider the potential financial impact of these environmental commitments and the possibility of unforeseen expenses stemming from new regulations. - Technological and Execution Risks:

The company's net-zero GHG emissions target is ambitious and relies on the development and implementation of technologies that are currently experimental, such as carbon capture and storage (CCS). The success of these initiatives is uncertain, and failure to progress as planned could lead to increased costs that have not been accounted for. Moreover, EOG's reliance on third-party operators for some properties introduces execution risks that could affect project outcomes and financial results. These factors suggest that EOG's future profitability may be more precarious than it appears. - Geopolitical Tensions and Economic Indicators:

Global geopolitical tensions, such as conflicts that disrupt oil supply lines, can lead to sudden spikes or drops in oil prices, affecting EOG's revenue unpredictably. Additionally, the recent news headlines regarding the Federal Reserve's stance on interest rates and the strong labor market performance present a mixed economic outlook. While the Fed's decision to potentially hold rates steady could signal economic stability, the complexity of balancing inflation with economic growth suggests that the economic environment remains uncertain. This uncertainty, combined with the inherent risks in the oil and gas sector, makes EOG's stock a potentially volatile investment.

Comments ()