Microsoft, all that AI and Cloud

Microsoft's Q1 FY 2024 report shows a noteworthy performance, with a 13% increase in revenue, reaching $56.517 billion...

Microsoft Corp. (MSFT),

November 8, 2023

(An occasional AI generated investment deep dive into a company of interest)

Company Overview

Microsoft Corp is a technology giant with a diverse range of products and services. They operate in sectors like operating systems, productivity applications, server applications, video games, and hardware such as PCs, tablets, and gaming consoles. They also offer cloud-based solutions, consulting services, and online advertising. Microsoft has been focusing on AI, as seen in products like Microsoft Cloud and Microsoft Teams.

The company operates in several significant business sectors such as AI technology, gaming, cloud-based services, and first-party devices. They are planning to acquire Activision Blizzard, which would strengthen their position in the gaming industry. Microsoft is also investing in workplace transformation, AI, security solutions, and utilizing Windows to enhance their cloud business.

New areas of business that could drive revenue and profit growth include their AI-powered platforms, gaming industry investments, and sustainability initiatives. Their acquisition of Activision Blizzard and their AI Skills Initiative are expected to provide significant growth. Microsoft's commitment to reducing their carbon footprint and becoming more sustainable could open up potential revenue streams via green energy and carbon offset initiatives.

Microsoft also provides various productivity and business process products, including Office Consumer and Office Commercial, and LinkedIn. Their Intelligent Cloud services, including Azure and Nuance, offer both public and private server products and cloud services. Potential revenue drivers could be the shift from on-premises solutions to Office 365 and Dynamics 365, expanded product offerings, subscriptions for LinkedIn's monetized solutions, and growing demand for Azure's AI infrastructure and services.

In the AI sector, Microsoft faces competition from Amazon and Google. In server and systems management, they compete with Hewlett-Packard, IBM, and Oracle. In personal computing, they face competition in areas of database, business intelligence, software development, and enterprise services. However, Microsoft's advantage lies in its ability to provide integrated and comprehensive solutions across various business needs. Future revenue and profit growth could be driven by their investment in gaming studios, patent licensing, exclusive game content, and growth in devices.

By the Numbers

- Revenue: Increased by 7% to $211.9 billion in FY 2023 and by 13% to $56.517 billion in Q1 FY 2024.

- Gross Margin: Increased by 8% to $146.05 billion in FY 2023.

- Operating Expenses: Rose by 10% in FY 2023.

- Net Income: Decreased slightly by 1% to $72.36 billion in FY 2023.

- Productivity and Business Processes Revenue: Increased by 9% to $69.27 billion in FY 2023 and by 13% to $18.6 billion in Q1 FY 2024.

- Intelligent Cloud Revenue: Increased by 17% to $87.9 billion in FY 2023 and by 19% to $24.26 billion in Q1 FY 2024.

- More Personal Computing Revenue: Decreased by 9% to $54.73 billion in FY 2023 and increased by 3% to $13.67 billion in Q1 FY 2024.

- Operating Income: Rose by 6% to $88.52 billion in FY 2023 and by 25% to $26.895 billion in Q1 FY 2024.

- Effective Tax Rate: Increased from 13% in FY 2022 to 19% in FY 2023.

- Cash, Cash Equivalents, and Short-Term Investments: Increased from $104.8 billion in FY 2022 to $111.3 billion in FY 2023 and to $144.0 billion in Q1 FY 2024.

- Cash from Operations: Decreased by $1.5 billion to $87.6 billion in FY 2023 and increased by $7.4 billion to $30.6 billion in Q1 FY 2024.

- Dividends: Increased from $18.6 billion in FY 2022 to $20.2 billion in FY 2023.

- Share Repurchase: The company repurchased 69 million shares for $18.4 billion in FY 2023 and 11 million shares for $3.6 billion in Q1 FY 2024.

- Acquisition of Activision Blizzard: Completed for a total cash payment of $61.8 billion in Q1 FY 2024.

- Pending IRS Audit: Proposed additional tax payment of $28.9 billion plus penalties and interest.

- Pending Transition Tax Liability: $7.7 billion as of September 30, 2023.

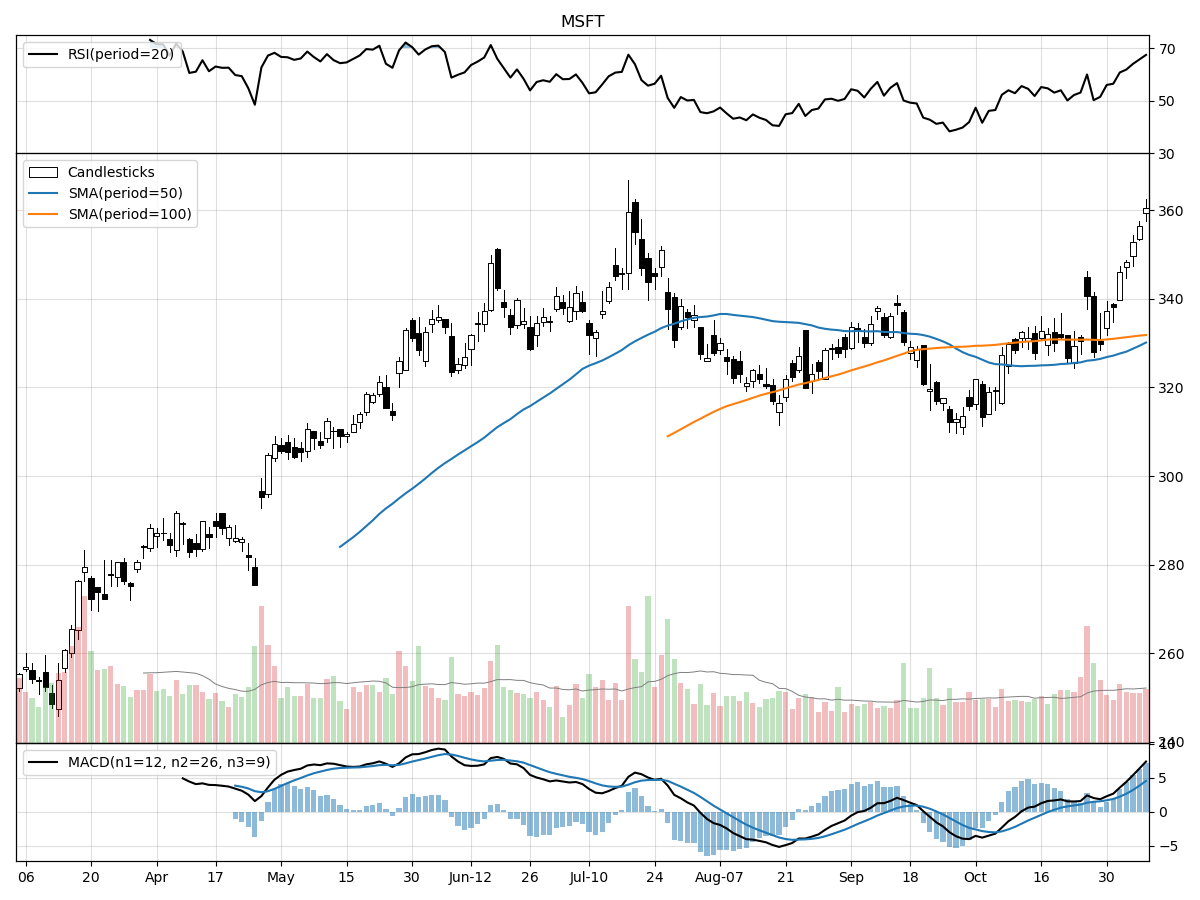

Stock Performance and Technical Analysis

Analyzing the current state of the stock, it's clear that the stock is showing a positive trend overall. The current price of the stock is $360.53, which is a significant 45% above its 52-week low, indicating a strong recovery and bullish trend. Additionally, the stock has seen a steady increase over the past few months, with a rise of 8.46% in the last month and a 12.01% increase in the last quarter. This consistent upward trajectory suggests that the stock has strong momentum, which is a key indicator for potential growth.

In terms of volume, the recent daily volume stands at 26,064,515 shares/day, which is slightly below the longer-term average of 26,732,541 shares/day. While there's a slight dip, it's not significant enough to indicate a substantial change in investor interest or trading activity. The Moving Average Convergence Divergence (MACD) is bullish at 4.558, which is a signal that the stock's short-term momentum is outpacing its long-term momentum, another positive sign for investors.

However, it's important to note that the stock is currently under heavy buying pressure according to money flow indicators. At the same time, the stock is under distribution, which means that despite the buying pressure, shareholders are selling their shares. This could be a cause for concern as it might indicate that the stock is nearing its peak and may soon start to decline. While the stock's current performance is strong, investors should keep an eye on these indicators to avoid potential pitfalls.

Overall, the stock demonstrates a bullish trend but the distribution pressure suggests caution. As always, investors should conduct thorough research and consider their individual risk tolerance before making investment decisions.

The ‘Bull’ Perspective

Summary:

- Strong Q1 FY 2024 performance: Microsoft's Q1 FY 2024 report shows a robust 13% increase in revenue, reaching $56.517 billion, and a 25% increase in operating income at $26.895 billion.

- Significant growth in cloud revenue: Microsoft's cloud revenue saw a substantial increase of 24% to $31.8 billion.

- Investments and cash inflow: Microsoft's cash, cash equivalents, and short-term investment totals rose from $111.3 billion in June 2023 to $144.0 billion in September 2023.

- Share repurchase program: Microsoft's $60 billion share repurchase program had $18.7 billion remaining as of September 2023.

- Pending risks: The company is currently under audit by the IRS, facing a proposed additional tax payment of $28.9 billion plus penalties and interest.

Strong Q1 FY 2024 performance:

Microsoft's Q1 FY 2024 report shows a noteworthy performance, with a 13% increase in revenue, reaching $56.517 billion. This growth is further augmented by a 25% increase in operating income, which reached $26.895 billion. The Productivity and Business Processes and Intelligent Cloud divisions saw increases of 13% ($18.6 billion) and 19% ($24.26 billion) respectively. The More Personal Computing division also saw a modest increase of 3% ($13.67 billion). These figures indicate a strong financial performance and a promising future for Microsoft.

Significant growth in cloud revenue:

Microsoft's cloud revenue saw a significant increase of 24% to $31.8 billion. The company's investment in cloud services is paying off, with Dynamics products and cloud services revenue increasing by 22%, and Dynamics 365 growing by 28%. This growth in cloud revenue is a clear indication of Microsoft's successful transition to a cloud-first business model and the increasing demand for cloud services.

Investments and cash inflow:

Microsoft's cash, cash equivalents, and short-term investment totals rose from $111.3 billion in June 2023 to $144.0 billion in September 2023. Over the same period, equity investments increased from $9.9 billion to $11.4 billion. Cash inflow from operations rose considerably by $7.4 billion to $30.6 billion. This strong cash position and positive cash flow provide Microsoft with the financial flexibility to invest in growth opportunities, return capital to shareholders, and weather any potential economic downturns.

Share repurchase program:

Microsoft's $60 billion share repurchase program had $18.7 billion remaining as of September 2023. For Q3 2023, Microsoft repurchased 11 million shares for $3.6 billion, while in Q3 2022, it repurchased 17 million shares for $4.6 billion. Share repurchases signal the company's confidence in its future prospects and commitment to returning capital to shareholders, which is a positive sign for investors.

Pending risks:

The company is currently under audit by the IRS, facing a proposed additional tax payment of $28.9 billion plus penalties and interest. This could potentially impact future financial performance. However, given Microsoft's strong cash position and robust financial performance, the company is well-equipped to manage this potential liability.

In conclusion, Microsoft's strong financial performance, significant growth in cloud revenue, robust cash position, and commitment to returning capital to shareholders through its share repurchase program make it a compelling investment opportunity. While the company faces potential risks, including the ongoing IRS audit, these risks are mitigated by the company's strong financial position and strategic investments in high-growth areas like cloud services.

The ‘Bear’ Perspective

- Microsoft's dependence on Windows licensing for significant revenue is under threat from emerging device platforms, which could lead to reduced revenue and operating margins.

- The company's heavy investments in cloud-based services and AI could backfire if they fail to attract enough users or generate sufficient revenue, potentially impacting gross margins and operating income.

- Microsoft's operational and cybersecurity risks, including data breaches and disruptions of online services, could lead to increased costs, loss of revenue, and reputational damage.

- Supply chain disruptions could negatively affect the production and distribution of products like Xbox consoles and Surface devices, impacting the company's revenue and operating margins.

- Legal and regulatory risks, including anti-corruption laws and data privacy regulations, could result in penalties, increased costs, and a tarnished reputation.

Windows Licensing Under Threat

Microsoft's significant reliance on Windows licensing for revenue is increasingly under threat from emerging device platforms like smartphones and tablets. As the technology landscape evolves rapidly, the traditional PC market, where Windows dominates, is shrinking. In 2020, global PC shipments amounted to approximately 275 million units, a decrease from the 365 million units shipped in 2011. This shift in consumer preferences could potentially lead to a decline in Microsoft's revenue and operating margins.

Investments in Cloud and AI

Microsoft has heavily invested in cloud-based services and AI, with operating expenses for the Intelligent Cloud segment amounting to $5.3 billion in Q1 FY 2024. However, these investments carry significant risks. If Microsoft fails to attract sufficient users or generate enough revenue to meet these costs, it could negatively impact their gross margins and operating income. In FY 2023, Microsoft's Intelligent Cloud segment's gross margin was 67%, down from 68% in FY 2022, indicating a potential squeeze on profitability.

Operational and Cybersecurity Risks

Microsoft faces significant operational risks, including data losses and disruptions of online services. In 2021, the company experienced a significant data breach affecting its Exchange Server software, which led to increased cybersecurity costs and reputational damage. Additionally, the company's reliance on third-party products could increase costs and liability claims, which could harm its competitive position.

Supply Chain Disruptions

The ongoing global supply chain crisis could negatively affect the production and distribution of Microsoft's hardware products like Xbox consoles and Surface devices. In Q1 FY 2024, the company's More Personal Computing division, which includes these products, saw only a modest increase of 3% in revenue, likely impacted by these disruptions. Such issues could continue to affect the company's revenue and operating margins.

Legal and Regulatory Risks

Microsoft is subject to numerous legal and regulatory risks. The company is currently under audit by the IRS, facing a proposed additional tax payment of $28.9 billion plus penalties and interest. Furthermore, scrutiny from competition laws in countries like the U.S., EU, and China might limit Microsoft's ability to optimize its portfolio and result in anti-competitive conduct claims. Breaches of Anti-Corruption laws might result in penalties or damage to Microsoft's reputation. Additionally, laws regarding the handling of personal data could result in increased costs and impede the adoption of Microsoft services, hurting its revenue and negatively affecting its reputation.

In conclusion, while Microsoft has shown strong performance in recent quarters, the company faces significant risks that could potentially impact its future financial performance. Investors should consider these factors carefully before making investment decisions.

Comments ()