Caesars Entertainment, Inc. (CZR), Large Cap AI Study of the Week

April 2, 2024

Weekly AI Pick from the S&P 500

Company Overview

Caesars Entertainment, Inc. (CZR) is a major player in the gaming and hospitality industry, having grown through acquisitions like Caesars Entertainment Corporation and William Hill PLC. The company's revenue streams are diverse, including gaming, sports betting, and hospitality from its 52 properties across the U.S. and its online platforms. Caesars has embraced the digital trend with sports betting and iGaming apps, and it also offers a range of non-gaming attractions such as The LINQ Promenade and the Colosseum at Caesars Palace. The company's business strategy includes leveraging its Caesars Rewards loyalty program and protecting its intellectual property, including trademarks for its sportsbook and online platforms.

Despite its success, Caesars faces challenges from competition, regulatory changes, and the need to comply with environmental and anti-money laundering laws. The business is sensitive to fluctuations in tourism and events, which can impact revenue. Caesars is also proactive in corporate social responsibility, with initiatives like PEOPLE PLANET PLAY aligning with the UN's Sustainable Development Goals, and it focuses on diversity, safety, and responsible gaming practices. Caesars Digital enforces age restrictions and responsible gaming, and the company is committed to reducing its environmental impact through its CodeGreen strategy. With a workforce of 51,000, nearly half unionized, Caesars aims to provide a diverse and inclusive work environment, competitive benefits, and has made significant progress in leadership diversity. The company also gives back to communities through the Caesars Foundation and has a comprehensive anti-money laundering program in place.

By the Numbers

Annual 10-K Report Summary:

- Net Revenues: $11,528 million (a significant recovery from the previous year).

- Net Income: $828 million (compared to a net loss in 2022).

- Issued New Debt Instruments: Specific figures not provided, but mentioned as part of financial activities.

- Net Revenue Increase: Specific figures not provided, but indicated across most segments.

- Caesars Digital Segment Growth: Significant, due to higher sports betting hold and market expansion.

- Increased Expenses: Notable in food and beverage, hotel, and interest expenses.

- Loss on Extinguishment of Debt: Substantial rise, specific figures not provided.

- Las Vegas Segment Revenue Increase: Moderate, specific figures not provided.

- Regional Segment Revenue Growth: Marginal, with some decreases in casino revenue and table game drop.

- Caesars Digital Segment Revenue Surge: Mainly from casino operations, sports betting handle declined.

- Managed and Branded Segment Revenue Growth: Specific figures not provided, but faced an Adjusted EBITDA decline.

Quarterly 10-Q Report Summary:

- Net Revenues Increase (Quarter): 3.7% year over year.

- Net Revenues Increase (Nine Months): 8.8% year over year.

- Adjusted EBITDA Margin (Quarter): 34.8%.

- Net Income Margin (Quarter): 3.1%.

- Adjusted EBITDA (Quarter): $1.043 billion.

- Adjusted EBITDA (Nine Months): $3.008 billion (up from $1.012 billion and $2.286 billion in the same periods of 2022, respectively).

- Cash Position: $841 million.

- Total Revolver Capacity: $2.934 billion.

- New Debt Issued: $2.5 billion term loan and $2 billion in senior secured notes, both maturing in 2030.

- Budget for Caesars Virginia Facility: $650 million (set to open in late 2024).

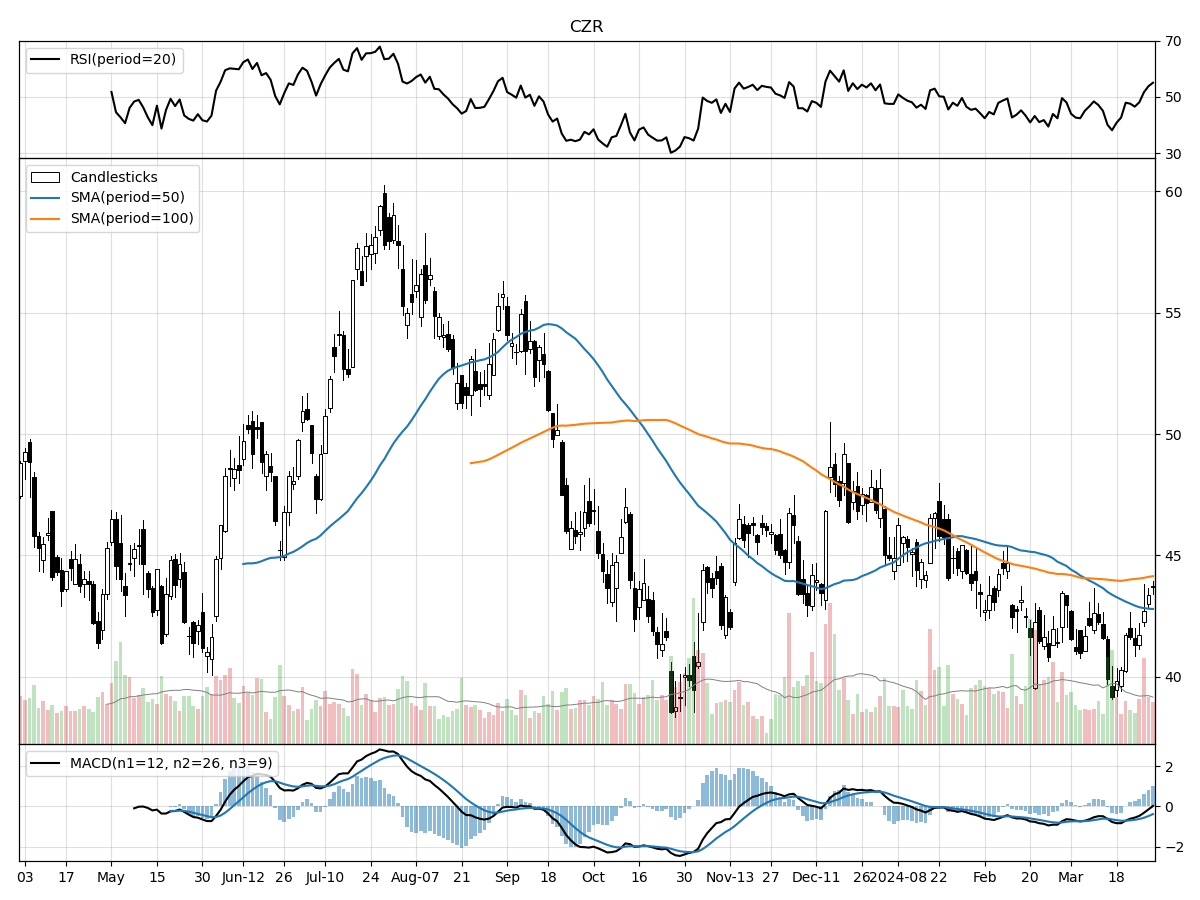

Stock Performance and Technical Analysis

The technical analysis of a stock provides insights into market sentiment and potential price movements based on historical trading data. In evaluating the stock in question, several key indicators present a mixed picture that requires a nuanced interpretation.

Firstly, the stock is trading at $43.74, which is 13% above its 52-week low and 26% below its 52-week high. This suggests that the stock has rebounded from its lows but is still significantly off from its peak, indicating there might be room for recovery if market conditions are favorable. However, this distance from the 52-week high could also signal underlying issues or a change in market sentiment that has led to a devaluation. The stability in price over the last month and three months shows a period of consolidation, which could precede a breakout or breakdown, depending on upcoming catalysts or market shifts.

Volume analysis shows that recent daily trading volume is slightly below the longer-term average, which could imply a waning interest from investors. This is an essential factor to consider, as volume can confirm trends; lower volumes may weaken any potential bullish or bearish signals. The Money Flow indicators provide conflicting information: moderate buying pressure would typically be a positive sign, indicating that investors are accumulating shares. However, indications of distribution suggest that larger investors may be offloading their positions, which could be a bearish sign.

The Moving Average Convergence Divergence (MACD) is currently bearish at -0.37. The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a stock's price. A negative MACD value indicates that the short-term average is below the long-term average, suggesting downward price momentum and reinforcing the bearish sentiment.

In summary, the stock presents a complicated technical setup. With the price consolidating, volumes slightly down, mixed money flow signals, and a bearish MACD, an investor would need to weigh these indicators carefully. It's important to consider the broader market context, any sector-specific news, and upcoming company events that could influence the stock's direction before making an investment decision. As always with technical analysis, these indicators are tools to gauge potential price action, and it's crucial to complement them with fundamental analysis and current market conditions.

The ‘Bull’ Perspective

Title: Caesars Entertainment, Inc. (CZR): A Strong Bet for Long-Term Growth

Upfront Summary:

- Revenue Growth and Diversification: CZR's net revenues have increased by 3.7% and 8.8% for the quarter and nine months ending September 30, 2023, respectively, showcasing the company's ability to grow and diversify its income streams.

- Strategic Expansion and Investment: With the opening of the Caesars Virginia facility and other projects, CZR's strategic investment of $650 million exemplifies its commitment to expanding its footprint and enhancing its market share.

- Robust Adjusted EBITDA: The company's Adjusted EBITDA rose to $1.043 billion for the quarter and $3.008 billion for the nine months ending September 30, 2023, reflecting strong operational performance.

- Strong Liquidity Position: CZR maintains a solid liquidity position with $841 million in cash and a total revolver capacity of $2.934 billion, providing financial flexibility and the ability to navigate market uncertainties.

- Digital Transformation and Market Positioning: The company's online gaming and sports wagering segments are showing improved revenues and reduced net losses, positioning CZR favorably in the rapidly growing digital gaming market.

Elaboration on Key Points:

- Revenue Growth and Diversification:

Caesars Entertainment's ability to grow its revenue by 3.7% and 8.8% during challenging economic times is a testament to its operational resilience and strategic business model. The company's revenue diversification, stemming from its gaming, hospitality, sports betting, and online gaming sectors, not only mitigates risks associated with market volatility but also positions it to capitalize on various market trends. Despite the competitive landscape, CZR's growth in its Las Vegas and Regional segments indicates a robust consumer demand for its offerings, reflecting the company's strong brand and customer loyalty. - Strategic Expansion and Investment:

CZR's investment in new projects, such as the $650 million Caesars Virginia facility, is a clear indicator of the company's forward-thinking approach and commitment to growth. These strategic expansions are expected to contribute significantly to future revenue streams and operational efficiencies. The company's ability to continuously invest in new ventures, despite divesting certain assets, demonstrates its strategic focus on long-term value creation and market expansion, which will likely provide a competitive edge in the ever-evolving gaming industry. - Robust Adjusted EBITDA:

The impressive increase in Adjusted EBITDA to over $1 billion for the quarter and $3 billion for the nine-month period is a strong indication of CZR's operational excellence and cost management capabilities. This financial metric, which reflects the company's earnings before interest, taxes, depreciation, and amortization, adjusted for certain items, provides investors with a clear picture of the company's underlying profitability and cash flow generation potential. The growth in Adjusted EBITDA also underscores CZR's ability to navigate the risks associated with rising operating expenses and interest rates. - Strong Liquidity Position:

With a robust liquidity position, including substantial cash reserves and revolver capacity, CZR is well-equipped to handle the potential impacts of economic downturns, rising costs, and other identified risks. The company's proactive approach to refinancing, including the issuance of new debt with favorable terms, strengthens its balance sheet and provides the necessary capital to pursue growth opportunities and weather any market headwinds. This financial stability is crucial for investor confidence, especially in light of the ever-present threats of public health crises and geopolitical tensions. - Digital Transformation and Market Positioning:

The growth of CZR's Caesars Digital segment is particularly noteworthy in an era where online gaming and sports wagering are becoming increasingly popular. By showing improved revenues and reduced net losses in these areas, CZR is effectively capturing the shift in consumer behavior towards digital platforms. The company's strategic focus on digital transformation not only aligns with current market trends but also provides a scalable business model that can adapt to future technological advancements. This strategic positioning is likely to contribute significantly to CZR's long-term growth and profitability.

In conclusion, Caesars Entertainment, Inc. (CZR) presents a compelling investment case for those looking to capitalize on the company's strategic growth initiatives, strong financial performance, and robust market positioning. While risks such as economic uncertainties, competition, and regulatory changes remain, CZR's proactive management and diversified business model provide a solid foundation for long-term success. Investors would be wise to consider CZR as a key player in their portfolio, poised to deliver sustainable returns in the dynamic gaming and entertainment sector.

The ‘Bear’ Perspective

Title: A Cautious Stance on Caesars Entertainment: Why Investors Should Hold Off

Upfront Summary:

- Revenue Growth vs. Operating Costs: While Caesars Entertainment, Inc. (CZR) reported a 3.7% and 8.8% increase in net revenues for the quarter and nine months ending September 30, 2023, respectively, operating expenses also rose, potentially squeezing profit margins.

- Interest Expense Concerns: CZR's interest expenses have increased due to higher financing obligations and interest rates, which could strain the company's financial flexibility and profitability.

- Competition and Market Saturation: The gaming and hospitality industry is highly competitive, and market saturation could limit CZR's growth potential, especially with the legalization and expansion of gaming in key markets.

- Regulatory and Operational Risks: Regulatory changes, public health crises, and cybersecurity threats present significant risks to CZR's operations and financial stability.

- Valuation and Market Dynamics: Current valuation metrics suggest that CZR's stock may be trading at a premium, and any adverse news or economic shifts could lead to a re-evaluation of the stock price.

Elaborating on the Points:

- Revenue Growth vs. Operating Costs:

Caesars Entertainment has shown resilience with its revenue growth, posting a 3.7% increase for the quarter and an 8.8% increase for the nine-month period ending September 30, 2023. However, these numbers do not exist in a vacuum. Operating expenses have concurrently risen, driven by higher general, administrative, food, and beverage costs. This uptick in expenses, if not managed, could erode the net income margin, which currently stands at 3.1%. Investors should be wary of this delicate balance, as any further increase in costs without a proportional rise in revenue could negatively affect the bottom line. - Interest Expense Concerns:

CZR's financials reveal a concerning increase in interest expenses, reflective of the company's higher financing obligations amidst a rising interest rate environment. This uptick in interest payments, from the issuance of a $2.5 billion term loan and $2 billion in senior secured notes, both due in 2030, could potentially limit the company's financial maneuverability. With a net income margin already at a modest 3.1%, the increased cost of debt servicing could put additional pressure on profitability. - Competition and Market Saturation:

The gaming sector is fiercely competitive, with numerous players vying for market share. Caesars' growth trajectory is at risk due to potential market saturation and the expansion of gaming operations, including online gaming, in key markets. For instance, the Regional segment's growth has been tempered by competition and adverse weather conditions. This saturation could cap the company's growth prospects and lead to a plateau in revenue, which does not bode well for a stock that commands a premium valuation. - Regulatory and Operational Risks:

Regulatory shifts, health epidemics like COVID-19, and cybersecurity threats pose significant operational risks to Caesars Entertainment. The company has already experienced the impact of such events, with property closures and operational restrictions during the pandemic. Additionally, a recent data breach involving their loyalty program underscores the potential financial and reputational damage from cybersecurity incidents. These risks could lead to unexpected costs, litigation, and a loss of customer trust, all of which could materially affect the company's financial health. - Valuation and Market Dynamics:

Despite the positive trends in some financial metrics, CZR's valuation may be cause for concern. Elevated valuations, particularly in a volatile market, expose the stock to sharp corrections if investor sentiment shifts or if the company fails to meet growth expectations. Given the current economic climate and the potential for further interest rate hikes, there's a credible risk that CZR's stock could be re-evaluated by the market, leading to a possible decline in its share price.

Conclusion:

In light of the above points, a bearish stance on Caesars Entertainment is justified. The company's increasing operating costs, higher interest expenses, fierce competition, regulatory and operational risks, and lofty valuation present a confluence of factors that could negatively impact its stock performance. Prudent investors should consider these risks and maintain a cautious approach when it comes to CZR, potentially looking for more favorable investment opportunities with a better risk-reward profile in the current economic landscape.

Comments ()