Bath & Body Works, Inc. (BBWI), Large Cap AI Study of the Week

August 27, 2024

Weekly AI Pick from the S&P 500

Company Overview

Bath & Body Works, Inc. is a prominent global retailer specializing in home fragrance, body care, and soap and sanitizer products, operating under brands like Bath & Body Works and White Barn. Transitioning from an apparel-based retailer, the company now focuses on exclusive fragrances for both body and home, distributing products through 1,850 company-operated stores and e-commerce sites in North America, along with additional international locations via franchise and wholesale arrangements. Their growth strategies revolve around brand innovation, international expansion, customer engagement through loyalty programs and digital optimization, and maintaining operational excellence. The company frequently launches new fragrances and products, driven by strong product development capabilities and strategic vendor partnerships, to adapt to changing customer preferences.

The loyalty program, with around 37 million active members, is a significant revenue driver, contributing to two-thirds of U.S. sales. In 2022, Bath & Body Works completed its first company-operated direct channel fulfillment center to support e-commerce growth. The company boasts a seasoned management team and operates a diversified store portfolio, predominantly off-mall, to mitigate exposure to vulnerable mall locations. As of early 2024, the company had expanded its international presence with 485 stores operated by partners. Bath & Body Works is enhancing its omnichannel capabilities through an IT Transformation Project, supported by a predominantly domestic, vertically integrated supply chain. The company experiences seasonal operations, with the fourth quarter being the most profitable due to the holiday season. Emphasizing a culture of inclusion, the Human Capital & Compensation Committee oversees diversity, equity, and inclusion (DEI) policies and executive compensation. Employing about 57,200 associates, the company promotes DEI through eight associate inclusion resource groups and commits to fair wages, offering comprehensive benefits and maintaining rigorous health and safety standards.

By the Numbers

Annual 10-K Report for 2023:

- Net Sales: $7.429 billion (2% decrease from 2022)

- Store Sales: $5.507 billion (1% increase from 2022)

- Direct Channel Sales: $1.582 billion (9% decrease from 2022)

- Gross Profit: $3.236 billion (slight decrease of $19 million from 2022)

- Gross Profit Rate: Improved by 50 basis points to 43.6%

- Operating Expenses: $1.951 billion ($72 million increase from 2022)

- Cash and Cash Equivalents: $1.084 billion (down from $1.232 billion in 2022)

- Debt Leverage Ratio: Improved from 3.1 to 2.8

- Dividend Payments: $0.80 per share, totaling $182 million for 2023

- Long-term Debt: Decreased from $4.862 billion to $4.388 billion

- Adjusted Net Income from Continuing Operations: $747 million (down from $878 million as per GAAP measures)

Quarterly 10-Q Report for Q1 2024:

- Consolidated Net Sales: $1.384 billion (0.9% decrease from Q1 2023)

- International Sales: Decreased by 29.3%

- Operating Income: $187 million (4% increase from Q1 2023)

- Cost Savings: $40 million achieved in Q1 2024

- Gross Profit: $606 million (increased from Q1 2023)

- Gross Profit Rate: Improved to 43.8% (up from 42.7% in Q1 2023)

- Operating Expenses: $419 million (up from Q1 2023)

- Interest Expense: Decreased to $82 million (from $89 million in Q1 2023)

- Net Cash from Operating Activities: $76 million

- Net Cash used for Investing Activities: $46 million

- Dividend Payment: $0.20 per share for Q1 2024 (consistent with Q1 2023)

- Long-term Debt: Decreased from $4,781 million in April 2023 to $4,282 million in May 2024

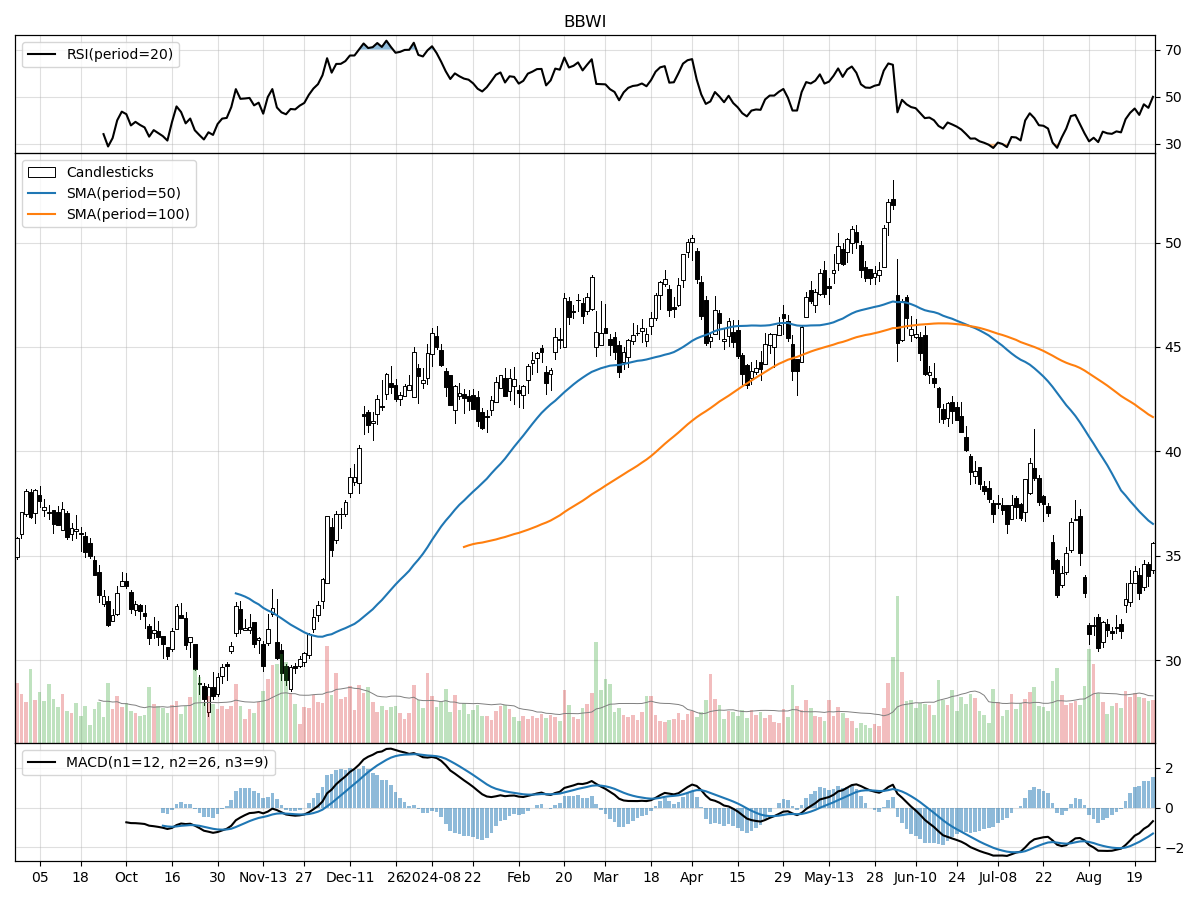

Stock Performance and Technical Analysis

When assessing the technical analysis for a stock currently priced at $35.60, several factors are considered. The stock is trading 26% above its 52-week low, which suggests that the stock has seen some positive momentum from its lowest point in the past year. However, it is also trading 31% below its 52-week high, indicating that the stock has retreated significantly from its peak and may be experiencing some bearish sentiment or undergoing a correction. The relative stability of the stock price over the last month could indicate consolidation, where the stock is trading within a narrow range as investors are deciding on the next move.

The stock's daily trading volume is above its longer-term average, with recent daily volume being 3689030 shares compared to a longer-term average of 3153719.5 shares. This increased volume may suggest heightened investor interest or activity, but it is essential to interpret volume in the context of price movements. The Moving Average Convergence Divergence (MACD) is currently bearish at -1.31, which typically signals downward price momentum and could be a bearish sign for potential investors.

Money flow indicators present a mixed signal. On one hand, the stock is showing moderate buying pressure, which could be indicative of investors accumulating shares and could precede an upward price move. On the other hand, the stock is also under distribution, implying that some investors are selling their shares which might reflect a bearish outlook or profit-taking activities. In conclusion, the technical indicators suggest a stock that is experiencing conflicting signals, with both positive buying pressure and negative distribution patterns, alongside a bearish MACD. This mixed analysis would often lead to a cautious investment stance, as the conflicting signals do not provide a clear directional bias. Investors should consider other fundamental factors, the company's recent earnings, industry performance, and broader market conditions before making an investment decision.

The ‘Bull’ Perspective

Summary:

- Robust Financial Performance: BBWI demonstrates strong financial health with a 4% increase in operating income and an improved gross profit rate from 42.7% to 43.8%.

- Strategic Cost Optimization: The company's ongoing plan has already realized $40 million in savings, with a target of $250 million annually by the end of fiscal 2024.

- Dividend Consistency: BBWI has maintained a steady dividend, reinforcing its commitment to shareholder returns.

- Debt Reduction: Long-term debt has been reduced from $4,781 million to $4,282 million, indicating a robust balance sheet.

- Market Position and Growth Prospects: Despite macroeconomic headwinds, BBWI's focus on core categories and digital expansion positions it for growth.

Elaboration:

- Robust Financial Performance:

Despite a slight decrease in net sales, Bath & Body Works, Inc. has shown a commendable increase in operating income by 4%, reaching $187 million. This is a testament to the company's ability to improve merchandise margins and manage costs effectively, even in a challenging retail environment. The gross profit rate has also seen a significant improvement, jumping to 43.8% from 42.7% in the previous year. This improvement is particularly noteworthy given the backdrop of rising inflation and supply chain disruptions, which have squeezed margins across the retail sector. BBWI's financial resilience, highlighted by these numbers, suggests a strong underlying business capable of weathering economic uncertainties. - Strategic Cost Optimization:

Bath & Body Works, Inc.'s commitment to cost optimization is evident in the $40 million savings already achieved. The aggressive target of $250 million in annual savings by the end of fiscal 2024 is not only ambitious but also indicative of the company's proactive approach to maintaining profitability. This strategic initiative will likely enhance BBWI's operational efficiency and competitiveness, particularly as the retail landscape continues to evolve rapidly with increased e-commerce adoption and shifting consumer preferences. - Dividend Consistency:

In a market where many companies have cut or suspended dividends due to economic pressures, BBWI's consistency in dividend payments is a strong signal of financial stability and shareholder value. The company has maintained its dividend payout at $0.20 per share, showcasing a reliable income stream for investors. This consistency is a crucial factor for income-focused shareholders and reinforces BBWI's reputation as a resilient investment in the consumer discretionary sector. - Debt Reduction:

BBWI's ability to reduce its long-term debt load from $4,781 million to $4,282 million is a significant move towards strengthening its balance sheet. This reduction in senior debt across various fixed interest rate notes due between 2025 and 2037 demonstrates prudent financial management and a commitment to reducing leverage. In an environment where many retailers are burdened by heavy debt loads, BBWI's deleveraging efforts set it apart and may provide a cushion against future economic shocks. - Market Position and Growth Prospects:

While facing a decrease in international sales and the normalization of product demand post-pandemic, BBWI is actively driving growth through its core categories, new product lines, and enhanced customer loyalty and digital experiences. The company's strategic focus on these areas is particularly important as the retail sector continues to experience rapid transformation. With a gross profit increase and a clear plan for digital expansion, BBWI is positioning itself to capture market share and meet the evolving needs of consumers. The commitment to innovation and customer engagement, coupled with a strong financial foundation, suggests that BBWI is well-equipped to navigate the macroeconomic challenges ahead and capitalize on growth opportunities.

Conclusion:

Bath & Body Works, Inc. presents a compelling investment case, underpinned by its robust financial performance, strategic cost optimization initiatives, consistent dividend payments, debt reduction, and strong market positioning with clear growth prospects. While the broader economic environment and specific risks such as inflation and supply chain disruptions pose challenges, BBWI's resilience and strategic actions demonstrate its potential to thrive. Investors looking for a stable yet growth-oriented retail stock may find BBWI to be an aromatic blend of opportunity in a volatile market.

The ‘Bear’ Perspective

Summary:

- Declining International Sales: BBWI's international sales plummeted by 29.3%, significantly contributing to the overall sales dip of 0.9%.

- Rising Operating Expenses: Despite an increase in operating income, BBWI is experiencing higher general, administrative, and store operating expenses, now at 30.3% of net sales.

- Vulnerable to Economic Headwinds: Macroeconomic challenges and normalization of demand post-pandemic pose a risk to BBWI's growth trajectory.

- Labor Market and Supply Chain Concerns: Labor challenges and supply chain disruptions can lead to increased costs and operational inefficiencies.

- Dependence on Seasonal Sales and Physical Stores: Heavy reliance on the holiday season and physical store traffic could lead to volatility in earnings.

Elaboration:

- Declining International Sales:

BBWI's recent 29.3% dive in international sales is a red flag for investors. This downturn is a considerable part of the overall 0.9% decrease in net sales to $1.384 billion. When a company faces such a steep decline in an entire segment, it's indicative of underlying issues that could range from poor market penetration to increased competition or even geopolitical tensions affecting consumer behavior. For a retail company, international markets often present an opportunity for growth outside of saturated domestic markets. BBWI's failure to capitalize on this could limit its long-term potential, making the stock less attractive. - Rising Operating Expenses:

The increase in operating expenses, now accounting for 30.3% of net sales, is another concern. Higher associate wages, BOPIS (Buy Online, Pick Up In-Store) fees, and marketing expenses are driving these costs. While investing in employees and marketing can be beneficial, there is a delicate balance to maintain profitability. If these costs continue to outpace sales growth, BBWI's margins could be squeezed further, ultimately impacting the bottom line and making the stock a less desirable investment. - Vulnerable to Economic Headwinds:

BBWI's acknowledgment of macroeconomic challenges and the expected normalization of demand post-pandemic suggests a potentially rocky road ahead. With the Federal Reserve's anticipated interest rate cuts, there may be a broader economic slowdown on the horizon. A slowdown could exacerbate the already declining sales and put additional pressure on the company's financial performance. Investors should be wary of stocks like BBWI that are sensitive to economic cycles and consumer discretionary spending. - Labor Market and Supply Chain Concerns:

Labor-related challenges and supply chain disruptions are critical risks for BBWI. The retail sector is labor-intensive, and with the current environment of rising wages, BBWI could face increased operational costs. Furthermore, supply chain issues can lead to inventory problems and delayed product availability, which in turn can harm sales and customer satisfaction. These factors could negatively impact the company's efficiency and profitability, making the stock less appealing to investors. - Dependence on Seasonal Sales and Physical Stores:

BBWI's significant reliance on the fourth-quarter holiday season for a substantial portion of its annual revenue is a considerable risk. Any disruption during this period, such as a weaker-than-expected retail environment or shifts in consumer spending habits, could have a disproportionate impact on the company's financial results. Additionally, the company's dependence on foot traffic in physical stores in an increasingly digital world poses a long-term risk. As online shopping continues to grow in popularity, BBWI may struggle to maintain its brick-and-mortar sales, potentially leading to a decline in overall revenue and profitability.

In conclusion, while Bath & Body Works, Inc. may have a strong brand and a loyal customer base, the combination of declining international sales, rising expenses, vulnerability to economic downturns, labor and supply chain issues, and dependence on seasonal and in-store sales present significant challenges. These factors, coupled with the broader market and economic risks, suggest that investors should exercise caution when considering BBWI stock. It may be prudent to avoid buying, selling, or shorting the stock until the company demonstrates it can effectively navigate these challenges and capitalize on growth opportunities.

Comments ()