Apple Inc. (AAPL), Large Cap AI Study of the Week

June 18, 2024

Weekly AI Pick from the S&P 500

Company Overview

Apple Inc. is a diversified technology company that designs, manufactures, and markets a wide range of products including smartphones (iPhone), personal computers (Mac), tablets (iPad), wearables (Apple Watch, AirPods), and home devices (Apple TV and HomePod). Beyond hardware, Apple offers various services such as advertising, AppleCare support, cloud services, digital content subscriptions (Apple Music, Apple TV+, Apple Arcade), and payment services (Apple Card, Apple Pay). The company operates on a global scale with significant markets in the Americas, Europe, Greater China, Japan, and the Rest of Asia Pacific.

Apple faces fierce competition driven by rapid technological advancements, aggressive pricing, and frequent new product introductions. Future revenue and profit growth are expected from expanding existing markets, launching innovative products and technologies, and increasing emphasis on its services and digital content platforms. The company places great importance on intellectual property protection but relies heavily on its innovative workforce and strong marketing capabilities. Apple experiences seasonal sales fluctuations, with higher sales typically in the first fiscal quarter due to holiday demand and new product launches. Committed to an inclusive, diverse, and safe work environment, Apple offers competitive compensation and comprehensive benefits, promotes open communication, and regularly seeks employee feedback to foster a collaborative culture. The company also prioritizes health and safety through extensive training and measures to ensure employee security and wellbeing.

By the Numbers

Annual 10-K Report Summary for Fiscal Year 2023:

- Total net sales: $383.3 billion

- Net income: $97.0 billion

- Decrease in net sales: 3% ($11.0 billion) from the previous year

- iPhone and Mac sales: Not specified, but noted as reduced

- Share repurchase program: $90 billion

- Dividend increase: Quarterly dividend to $0.24 per share

- Sales by region: Declines in the Americas, Europe, Greater China, and Japan; Rest of Asia Pacific increased by 1%

- Services segment: 9% increase in net sales

- Gross margins: Relatively stable

- Operating expenses: Increase, with R&D costs up by 14%

- Effective tax rate: Lower than the previous year due to reduced rate on foreign earnings and U.S. foreign tax credit regulations

- Cash, cash equivalents, and unrestricted marketable securities: $148.3 billion

- Debt: $106.6 billion

- Lease payments: $15.8 billion

- Manufacturing purchase obligations: $53.1 billion

- Other purchase commitments: $21.9 billion

- Deemed repatriation tax balance: $22.0 billion ($6.5 billion payable within the next year)

Quarterly 10-Q Report Summary for Q2 2024:

- Total net sales for the quarter: $90.8 billion (4% decrease YoY)

- Total net sales for the first six months: $210.3 billion (1% decline)

- iPhone sales: 10% decrease

- iPad sales: 17% decrease

- Wearables, Home, and Accessories: 10% decrease

- Services net sales: 14% increase

- Mac net sales: 4% increase

- Net sales by region for the quarter: Americas down 1%, Europe up 1%, Greater China down 8%, Japan down 13%, Rest of Asia Pacific down 17%

- Gross margin: Improved to 46.6%

- Services gross margin: 74.6%

- Products gross margin: Relatively flat YoY with a slight increase

- Operating expenses: Increased due to higher headcount costs and infrastructure-related costs

- Provision for income taxes and effective tax rate: Increased compared to 2023

- Liquidity: Not specified in the summary

- Manufacturing obligations: $34.2 billion

- Stock repurchases: $23.5 billion

- Dividend: Increased from $0.24 to $0.25 per share

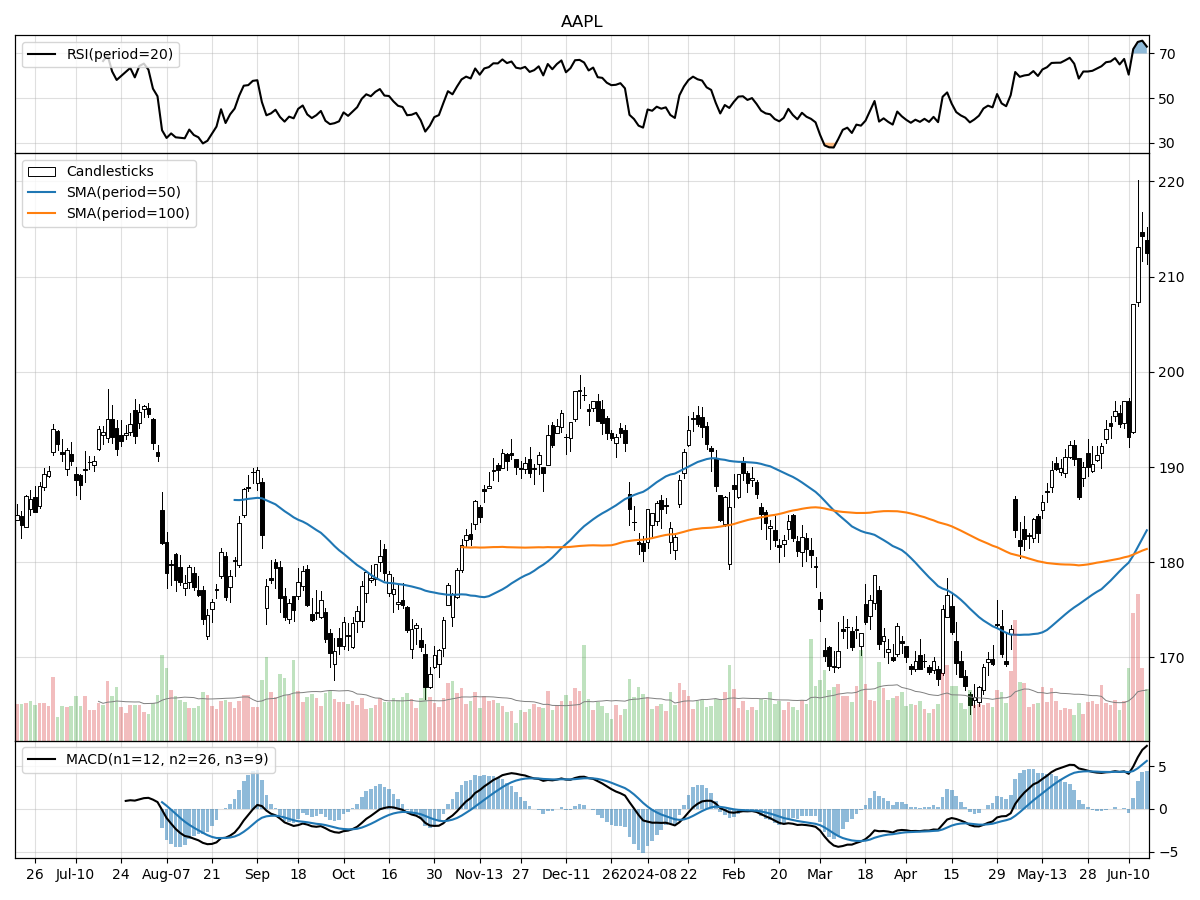

Stock Performance and Technical Analysis

The current stock price of $212.49 is demonstrating strong upward momentum, as it is just a hair below its 52-week high and a substantial 28% above its 52-week low. This suggests that the stock is experiencing a robust bullish trend. A stock trading close to its 52-week high can indicate a strong market belief in the company's prospects, although it can also signal caution for investors as it may imply limited upside potential unless the company's fundamentals support further growth.

The recent trading volume is higher than the longer-term average, with daily volume at around 68 million shares compared to the average of approximately 59 million shares. This elevated volume, in tandem with the stock's price increase, may indicate strong investor interest and could be seen as a confirmation of the current uptrend. However, as the Relative Strength Index (RSI) suggests the stock is overbought, there's a potential risk that the stock may be due for a pullback or consolidation in the near term as traders may take profits, causing the price to stabilize or decline temporarily.

Further reinforcing the bullish sentiment, the Moving Average Convergence Divergence (MACD) is currently bullish at 5.599, which typically suggests that the stock has positive momentum and could continue to rise. Additionally, the money flow indicators pointing to heavy buying pressure and accumulation indicate that investors are actively purchasing the stock, which could drive the price higher as demand outstrips supply. However, investors should remain cautious due to the overbought condition signaled by the RSI. It is often advisable to look for a potential entry point after a corrective phase when the RSI has retreated from overbought levels, assuming the underlying fundamentals of the company remain solid. Overall, while the technical indicators are mainly positive, they also signal the need for caution and a thorough assessment of the company's fundamental strength before making an investment decision.

The ‘Bull’ Perspective

Summary:

- Resilient Services Growth: Apple's Services segment has seen a robust 14% increase in net sales, highlighting a growing and more stable revenue stream that diversifies beyond hardware reliance.

- Improved Margins: Gross margin improvement to 46.6% demonstrates Apple's ability to manage costs effectively and optimize its product mix, even in a challenging economic environment.

- Strategic Capital Returns: Apple's commitment to shareholder returns remains strong, with $23.5 billion in stock repurchases and a dividend increase, signaling confidence in its financial health.

- Innovation and Market Position: Despite a competitive landscape, Apple's continuous innovation and strong brand position it well to capture consumer interest with new product releases.

- Macroeconomic Tailwinds: Lower-than-expected inflation rates and potential Fed rate cuts could lead to increased consumer spending power and a more favorable borrowing environment for Apple.

Elaboration:

- The Services sector of Apple has become a pillar of strength, contributing significantly to the company's bottom line with a 14% increase in net sales compared to the previous year. This uptick is not just impressive in isolation but also when considering the broader economic context where other segments have faced headwinds. The Services growth underscores the success of Apple's strategic pivot towards recurring revenue streams such as iCloud, Apple Music, and the App Store, which provide a buffer against the cyclical nature of hardware sales. With over 1.5 billion active devices globally, Apple's ecosystem is vast, and each user represents a potential subscriber, indicating a substantial runway for further growth in this segment.

- Gross margin is a critical indicator of operational efficiency and pricing power, and Apple has reported an impressive increase to 46.6%. This improvement is a testament to Apple's ability to navigate supply chain complexities and currency fluctuations while still delivering cost savings and a favorable mix of high-margin services. With the Products gross margin remaining relatively stable, it's clear that Apple's strategic pricing and product mix are helping to maintain profitability even as the company faces declining sales in certain hardware categories.

- Apple's capital return program reflects its financial strength and commitment to delivering shareholder value. The company's $23.5 billion in stock repurchases underscores its belief in the intrinsic value of AAPL shares. Furthermore, the dividend increase from $0.24 to $0.25 per share might appear modest, but it represents a steady income stream for investors and a signal that Apple is confident in its ability to generate ample free cash flow, despite market volatility.

- Innovation is at the core of Apple's DNA, and its market position remains solid. While iPhone sales have recently dipped by 10%, Apple has a track record of reinvigorating its product lines with cutting-edge features that resonate with consumers. The upcoming iOS updates, potential new hardware releases, and advancements in AR/VR technology are all areas where Apple could redefine the market once again. Moreover, with a dedicated and affluent customer base, Apple's product ecosystem encourages brand loyalty and repeat purchases, which is crucial in a competitive tech landscape.

- The macroeconomic environment presents a silver lining for Apple. With the CPI and PPI inflation readings coming in lower than expected, there is potential for a more favorable economic landscape ahead. Should the Fed decide to cut rates in response to sustained lower inflation, this could lead to increased consumer spending power, benefiting discretionary purchases such as electronics. Additionally, a more favorable borrowing environment could enable Apple to finance its operations and strategic initiatives more cheaply, further bolstering its financial position.

In conclusion, while the tech giant faces challenges like any other company, the combination of a diversified revenue base, strong operational efficiency, strategic shareholder returns, continuous innovation, and potential macroeconomic tailwinds make Apple Inc. a compelling buy for investors looking for long-term growth and stability in their portfolios.

The ‘Bear’ Perspective

In the current market landscape, Apple Inc. (AAPL) presents a precarious investment opportunity that warrants caution. Here are the key reasons to avoid buying, selling, or shorting Apple stock:

- Declining Sales Figures: Apple's most recent quarterly report shows a concerning 4% year-over-year decrease in net sales, with significant drops in iPhone, iPad, and Wearables sales.

- Geopolitical and Economic Headwinds: Macroeconomic factors, including a 10% drop in sales in Greater China and a 13% decline in Japan, reflect the impact of geopolitical tensions and economic slowdowns on Apple's performance.

- Rising Operating Expenses: Apple's operating expenses have increased due to higher R&D costs and infrastructure spending, which could squeeze future margins.

- Market Saturation and Competition: Apple operates in a highly competitive market with rapid technological changes, and there's a real risk of market saturation, especially in mature markets where growth is slowing.

- Regulatory and Legal Challenges: The company faces ongoing regulatory scrutiny, especially regarding its App Store practices, which could lead to enforced changes and financial penalties.

Elaboration on Key Points

- Declining Sales Figures: Apple's 4% decline in total net sales to $90.8 billion for the quarter is a red flag for investors. Even more concerning is the 10% decrease in iPhone sales, which are a cornerstone of Apple's revenue. The iPad and Wearables segments are also suffering, with sales down 17% and 10%, respectively. While Services net sales have increased by 14%, this may not be enough to offset the declines in hardware, which have traditionally been Apple's bread and butter.

- Geopolitical and Economic Headwinds: The sales drops in Greater China (8%), Japan (13%), and the Rest of Asia Pacific (17%) are indicative of broader issues. These regions have been hit by a combination of factors, including U.S.-China trade tensions, a strong U.S. dollar, and the ripple effects of economic slowdowns. Apple's reliance on international sales, which accounted for 61% of Q2 2024's revenue, makes it vulnerable to geopolitical risks and currency fluctuations.

- Rising Operating Expenses: Research and development costs, along with increased spending on selling, general, and administrative expenses, have driven up operating expenses. While investment in innovation is necessary, there is no guarantee of a proportional return on these investments. Higher expenses without a corresponding increase in sales put pressure on margins and, ultimately, on profitability.

- Market Saturation and Competition: Apple's market is showing signs of saturation, particularly in developed countries where most consumers who want and can afford an iPhone already have one. Moreover, the competition is not just from other high-end manufacturers but also from lower-cost producers who are increasingly offering high-quality alternatives. This competition could lead to a further erosion of Apple's market share and pricing power.

- Regulatory and Legal Challenges: Regulatory scrutiny is intensifying, particularly around the App Store, which has been a significant revenue driver for Apple. Changes to commission structures or business practices mandated by antitrust actions could have a substantial negative impact on Apple's services revenue. Additionally, Apple's extensive international operations expose it to a complex web of laws and regulations, which could lead to increased compliance costs or fines.

In conclusion, while Apple Inc. remains a tech behemoth with a strong brand and a loyal customer base, the combination of declining sales in key product categories, geopolitical and economic uncertainties, rising operating expenses, market saturation, and looming regulatory challenges present significant risks. These factors suggest that a cautious approach is warranted, and investors should consider these risks carefully before making any decisions regarding Apple stock.

Comments ()